Broadcom (AVGO -1.25%) has been a big winner of the booming demand for artificial intelligence (AI) chips in the past year. Shares of the chip designer shot up 89% during this period, and that solid rally seems justified in light of the company's improving growth profile owing to its dominant position in the market for custom AI chips.

The company is set to release its fiscal 2025 third-quarter results on Sept. 4, and it won't be surprising to see the stock get a nice shot in the arm once it releases its report. Let's look at the reasons why it may be a good idea to buy Broadcom stock before its upcoming results.

Image source: Getty Images.

Broadcom can beat Wall Street's expectations once again

Broadcom's earnings per share exceeded consensus estimates in each of the past four quarters. Investors can expect the company to deliver a market-beating performance once again, thanks to a couple of reasons.

NASDAQ: AVGO

Key Data Points

First, tech giants are expected to spend more money on AI infrastructure than previously estimated. As pointed out by Yahoo! Finance, AI spending by big tech companies -- Amazon, Microsoft, Alphabet, and Meta Platforms -- is expected to hit $364 billion in 2025, up by $39 billion from the original estimate.

The new estimate points toward an increase of 63% in AI spending this year by the big tech giants, up from the 59% increase witnessed last year. This stronger spending bodes well for Broadcom, especially considering that big tech companies are focusing on developing more in-house chips for their data centers.

This brings us to the second reason why Broadcom could deliver another quarter of better-than-expected results. Big tech companies are increasingly investing in custom AI processors for their data centers to reduce operational costs. This was the reason why investment bank UBS recently suggested that Broadcom is on track to exceed expectations when it releases its results and also raised its price target to $345 from $290.

According to UBS, Broadcom could get a boost from the stronger-than-expected production ramp of Google's custom AI processors. The investment bank is expecting the demand for Google's latest TPU (tensor processing unit) to jump by over 50% in 2025, and that could fuel a 60% increase in Broadcom's AI revenue this year.

Broadcom is already designing custom AI processors for Google, Meta, and ByteDance. Even better, the company is engaged with another four hyperscale customers for designing their custom AI processors. Reports indicate that these four customers could be xAI, OpenAI, Arm Holdings, and Apple.

So, the chances of Broadcom delivering better-than-expected results once again are quite solid thanks to stronger demand from current customers, as well as the potential ramp from new customers.

Another big reason to buy the stock

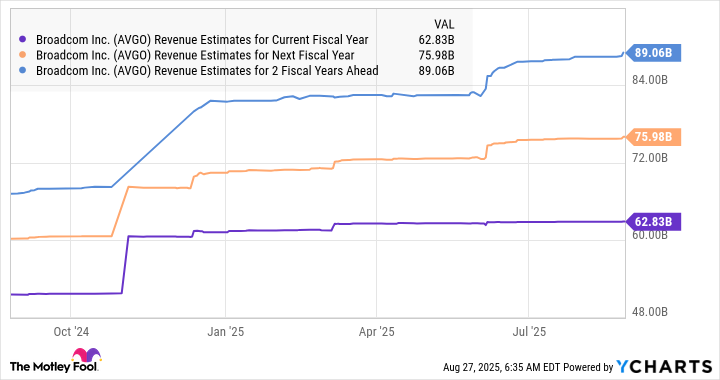

Analysts expect Broadcom to end the current fiscal year with almost $63 billion in revenue, which would be a 22% increase from the year-ago period. The company is on track to record AI-specific revenue of $13.6 billion in the first three quarters of the fiscal year, which translates into an annual run rate of just over $18 billion.

Looking ahead, Broadcom estimates its potential revenue opportunity from its first three custom AI chip customers to land between $60 billion and $90 billion in fiscal 2027. That opportunity could be much bigger when we take into account the new customers that the company is expected to bring on board.

As such, Broadcom seems to be on track to continue outperforming the market's expectations over the next three years since its AI business alone could be enough for it to crush Wall Street's revenue estimates in fiscal 2027.

AVGO Revenue Estimates for Current Fiscal Year data by YCharts

Importantly, Broadcom's 70% share of the custom chip market means that it is in a terrific position to capitalize on the huge end-market opportunity. All this makes Broadcom a top AI stock to buy and hold for the long run and doing that before its upcoming earnings report could be a smart move, since it could soar higher after Sept. 4.