Broadcom (AVGO +2.21%) is turning out to be one of the biggest beneficiaries of the artificial intelligence (AI) chip boom after Nvidia. That's because the application-specific integrated circuits (ASICs) that Broadcom designs have been a huge hit among cloud service providers looking for cheaper alternatives to the expensive graphics cards that Nvidia sells.

Not surprisingly, there are rumors that Nvidia has established a new department to focus on ASICs. The custom nature of these chips means that they can be programmed to perform specific tasks, which is why they are now gaining traction for AI inference applications.

The overwhelming performance per watt advantage that ASICs are capable of delivering over graphics processing units (GPUs) while performing the tasks they are designed for explains why they are now in great demand -- and other industry players are also benefiting.

Image source: Getty Images.

A smaller Broadcom rival is cutting its teeth in the lucrative custom AI processor market

Broadcom estimates that its serviceable addressable market (SAM) from just three hyperscale customers that are using its custom AI processors could be worth $60 billion to $90 billion in the next couple of years. That figure could head higher considering that Broadcom has brought new customers on board lately.

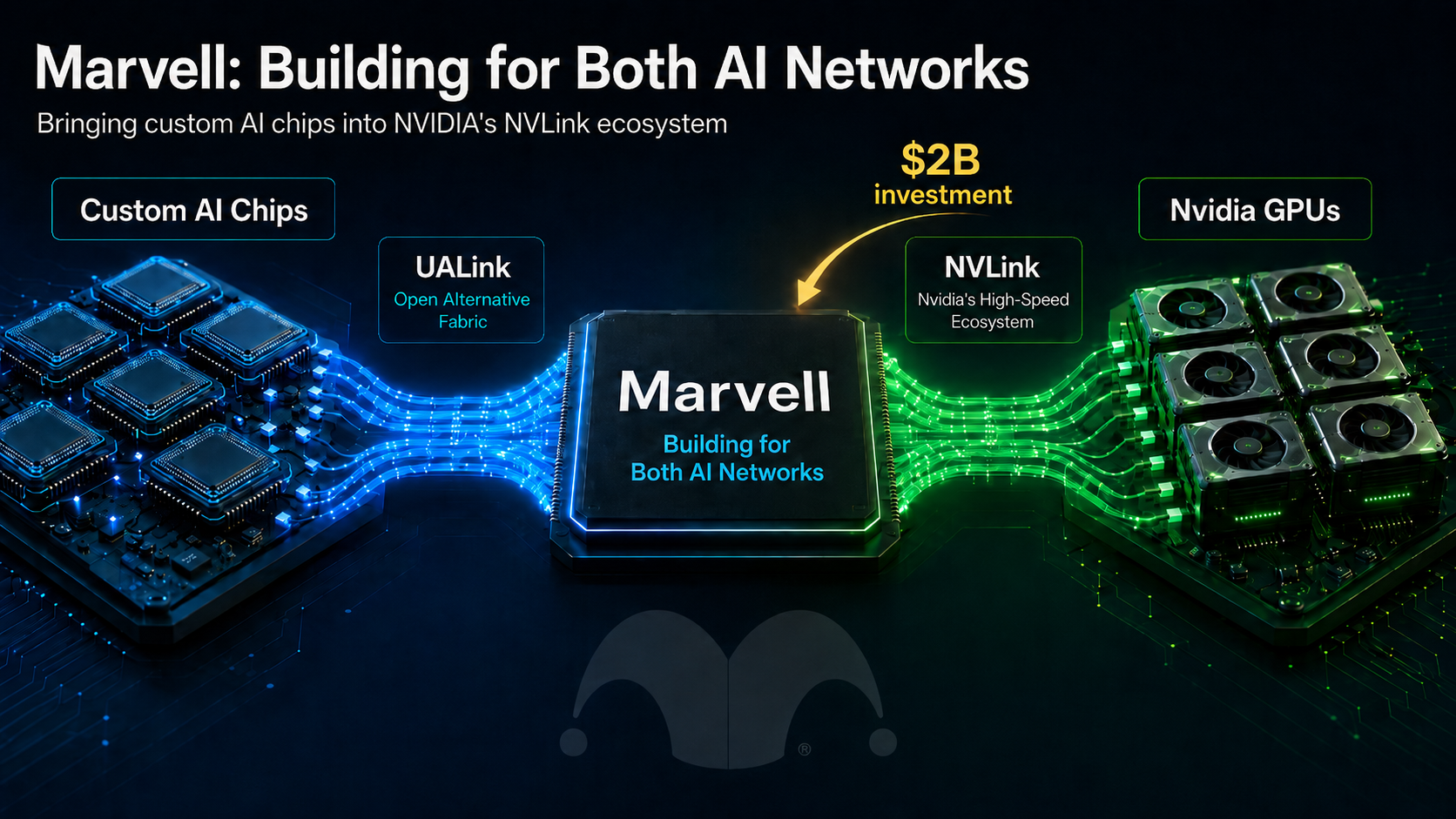

However, Broadcom isn't the only company that's looking to make the most of this market. We have seen that Nvidia may have already set its sights on this space. But it is worth noting that Broadcom has a smaller competitor that's rapidly gaining traction in the custom AI processor market and could challenge its dominance.

That company is Marvell Technology (MRVL +6.85%). While Broadcom is reportedly controlling an impressive 70% share of the custom AI processor space, Marvell is quickly gaining ground. It is targeting a 20% market share of custom AI processors by 2028, up from less than 5% in 2023. Earlier, Marvell was projecting an addressable revenue opportunity of $55 billion in this market by 2028, so a 20% share of this space by then would have brought its custom AI chip revenue to $11 billion.

NASDAQ: MRVL

Key Data Points

That would have been a substantial increase over the $4 billion AI revenue that Marvell is expected to generate in the ongoing fiscal year. However, don't be surprised to see the company's AI revenue turning out to be higher than $11 billion after three years as it has the ability to take share away from Broadcom, along with an expansion in its addressable opportunity.

Marvell management pointed out on its latest earnings conference call that it expects to corner 20% of an updated $94 billion total addressable market (TAM) by 2028. The company has generated $7.2 billion in total revenue in the past four quarters, which means the custom AI chip market alone has the ability to significantly supercharge its growth.

What's more, Marvell could take away more share from Broadcom in this market in the next three years than it is currently projecting. That's because it now sees more than 50 custom AI chip opportunities across more than 10 customers, which could help it generate a whopping $75 billion in lifetime revenue. Marvell has already been designing chips for three major cloud computing providers, and its updated pipeline suggests that it could witness a significant expansion in its customer base.

Marvell's valuation and healthier growth prospects make it a better bet than Broadcom

Marvell is growing at a faster pace than Broadcom. The former's revenue shot up by 58% year over year in the previous quarter to $2 billion, far exceeding the 22% spike in Broadcom's top line to $16 billion. Additionally, Marvell's earnings more than doubled year over year, while Broadcom reported a 36% increase in its non-GAAP earnings per share.

Of course, Marvell is the smaller company of the two. But that's precisely why it has the ability to keep growing at a faster pace by challenging Broadcom's dominance. Even better, Marvell is way cheaper than Broadcom with a forward earnings multiple of just 27 as compared to Broadcom's reading of 37. All this makes Marvell a top AI stock to buy right now, as it has the ability to deliver impressive long-term gains to investors by making a bigger dent in the lucrative custom AI chip market.