Here's a great way to earn strong market returns over the long term: Identify companies that have been ignored or underestimated by most investors but have attractive prospects; buy their shares at a deep discount; and hold on to them for a long time. Picking out such corporations isn't easy, though.

Let's consider two potential candidates: Iovance Biotherapeutics (IOVA +1.83%) and Teladoc Health (TDOC +4.17%). These two healthcare specialists have faced significant challenges in recent years but are trying to mount a comeback. Which one of the two is the more attractive contrarian buy? Let's find out.

Image source: Getty Images.

The case for Iovance Biotherapeutics

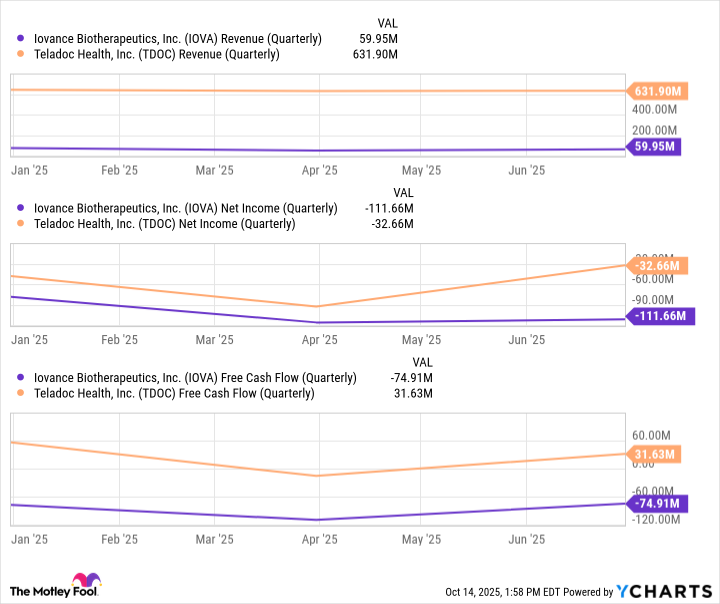

Iovance Biotherapeutics is a small-cap biotech company that developed Amtagvi, a medicine for advanced melanoma. This therapy was a bit of a breakthrough, becoming the first of its kind to be approved in this indication. Amtagvi's sales have been slowly ramping up since the drug's approval in February 2024. In the first half of 2025, Iovance's revenue -- almost all of which comes from Amtagvi -- totaled $109.3 million, more than tripling compared to the year-ago period.

The biotech expects revenue of $250 million to $300 million for the fiscal year, which isn't too bad for a company with a market cap of just $773 million. Further, Iovance recently received approval for Amtagvi in Canada and expects to launch the medicine in several other countries eventually. It estimates that every year, 8,000 patients in the U.S. die from melanoma. Though not all of them are eligible for Amtagvi, many more than it has treated so far are.

So, between the potential in the U.S. and other regions abroad, there is an attractive market that could allow Amtagvi to eventually become a blockbuster.

NASDAQ: IOVA

Key Data Points

Lastly, Amtagvi is being investigated as a treatment for several other forms of cancer. If Iovance can make solid clinical and regulatory progress, sales of its crown jewel will grow consistently and perhaps help the company turn profitable. There are some risks. Amtagvi is a complex medicine to manufacture and administer. It is made from patients' own cells and requires 34 days (on average) to make before being inserted via intravenous infusion after they have received chemotherapy.

That's why Amtagvi can only be administered in specialized centers. These are factors that somewhat limit the medicine's availability and increase commercialization expenses. But despite these challenges, if Iovance Biotherapeutics' master plan comes to fruition, the stock could soar.

The case for Teladoc Health

Teladoc Health, a notable player in the telemedicine market, has lost significant traction over the past few years. However, the company's ecosystem remains deep. As of the second quarter, it had 102.4 million members in its integrated care segment, a number that grew 11% compared to the same period last year.

The company's BetterHelp virtual therapy segment is bleeding paying subcribers, but the company is taking steps to address the problem. Teladoc made several acquisitions, including that of UpLift, a virtual mental health services provider. While Teladoc's own BetterHelp is not covered by insurance, UpLift has agreements with third-party payers that cover 100 million potential patients.

Teladoc has long said that insurance coverage for its therapy services could help attract more people to the BetterHelp platform, which it has marketed aggressively to drum up business. Now, through UpLift, it can target its marketing efforts toward patients who already have coverage for these services but have yet to opt in.

NYSE: TDOC

Key Data Points

Teladoc is also betting on international expansion efforts to help turn things around. The company's international sales have been growing faster in recent quarters.

Overall financial results haven't been strong. Second-quarter revenue dropped by 2% year over year to $631.9 million. But the company's well-established presence in a telemedicine market, which seems here to stay thanks to its convenience, along with efforts to boost its virtual therapy business and gain a footing abroad, might enable it to mount a comeback.

Which is the better buy?

To be clear, both of these companies are very risky. In my view, they are more likely than not to destroy shareholder value in the next five years. That said, Teladoc is the better option right now. It generates higher revenue and lower net losses, and has a deep ecosystem and a somewhat recognizable brand name in its industry.

IOVA Revenue (Quarterly) data by YCharts

Iovance's Amtagvi might seem promising, but the medicine's complexity makes it hard to bet on the biotech. Chances are that if Amtagvi were commercially viable, given Iovance's terrible stock performance over the past 18 months and its market cap well under $1 billion, a larger drugmaker with deep pockets might have swooped in to acquire the whole company at its current levels.

Of course, that might still happen, and there is also the chance that Amtagvi will succeed after all. Still, given the available information, contrarian investors with above-average risk tolerances should consider opting for Teladoc.