Duolingo (DUOL +0.80%) operates the world's most popular digital language education platform. Its stock was trading at a record high of around $540 back in May, as investors rewarded the company's rapid growth in users, revenue, and profits this year.

However, Duolingo stock has since plunged by 63% from its peak. Investors are concerned about a recent change in the company's strategy, which could slow its growth in favor of a more sustainable expansion over the long term. Plus, more broadly, investors have recently become cautious about owning stocks with very high valuations.

But Duolingo stock has declined to a very attractive level, especially considering the company's progress in the artificial intelligence (AI) space, which could unlock significant amounts of revenue over time. Here's why this could be a great opportunity to buy Duolingo stock.

Image source: Getty Images.

AI is a huge draw for Duolingo subscribers

Duolingo's success stems from its highly interactive, gamified lessons that drive high levels of engagement. Plus, its mobile-first approach places language education at the fingertips of anybody with a smartphone. During the third quarter of 2025 (ended Sept. 30), the platform had 135.3 million monthly active users, which was up 20% year over year.

Duolingo makes money by showing ads to its free users, but it also offers a range of paid subscription options for those who want to unlock additional features to accelerate their learning. A record 11.5 million users were subscribed at the end of the third quarter, which represented a 34% increase from the year-ago period.

Duolingo Max is the platform's most expensive subscription tier. It offers a growing list of AI-powered features like Explain My Answer, which provides users with personalized feedback after each lesson, and Roleplay, which uses a chatbot interface to help users practice their conversational skills. Duolingo also launched a new Max feature last year called Video Call, which uses an AI-powered digital avatar named Lily to help people practice their speaking skills in a language of their choice.

Max accounted for 9% of Duolingo's total subscriber base at the end of the third quarter, and bookings doubled year over year. Management actually feels Max could be doing even better, and as more users realize AI can help accelerate their learning experience, this subscription tier could become a major source of revenue for Duolingo.

NASDAQ: DUOL

Key Data Points

Duolingo's profits continue to soar

Duolingo's third-quarter revenue grew by 41% year over year to $271.1 million, clearing the company's guidance range of $257 million to $261 million. The strong result prompted management to increase its 2025 guidance for the third time, and it now expects to end the year with up to $1.031 billion in revenue.

But Duolingo's bottom line was the real story in the third quarter, because its net income soared more than tenfold to $292.2 million on a generally accepted accounting principles (GAAP) basis. The company had some help from a one-off tax benefit worth $245.7 million, which skewed the result, so its blistering growth wasn't entirely on merit.

However, even if we exclude all one-off and noncash expenses, the company still delivered adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of $80 million, which was up 68% year over year.

Duolingo stock has crashed to a very attractive level

Last week, Duolingo CEO Luis Von Ahn told investors that monetization won't be as much of a priority going forward. Instead, he wants the company to focus on acquiring more users and creating an even better learning experience. Investors are concerned this strategy shift will lead to slower revenue and earnings growth from here, which is why Duolingo stock fell by 25% immediately after the release of the Q3 report.

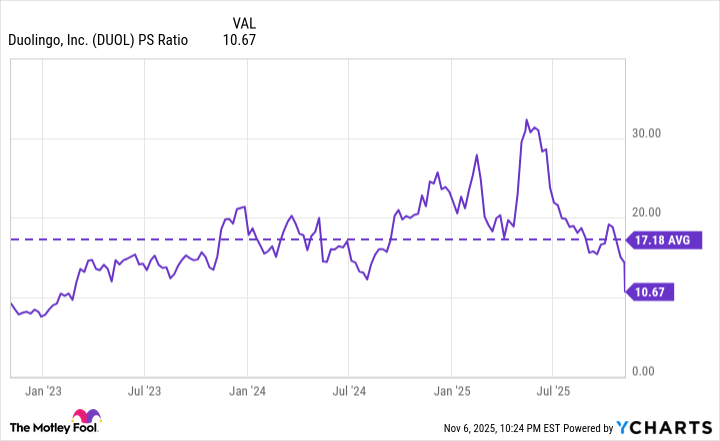

However, Duolingo is starting to look very attractive. Its price-to-sales (P/S) ratio was over 30 when its stock peaked back in May, which was completely unsustainable. But following the 63% crash in its stock since then, Duolingo's P/S ratio is now just 10.6, which is actually a sizable discount to its three-year average of around 17:

DUOL PS Ratio data by YCharts

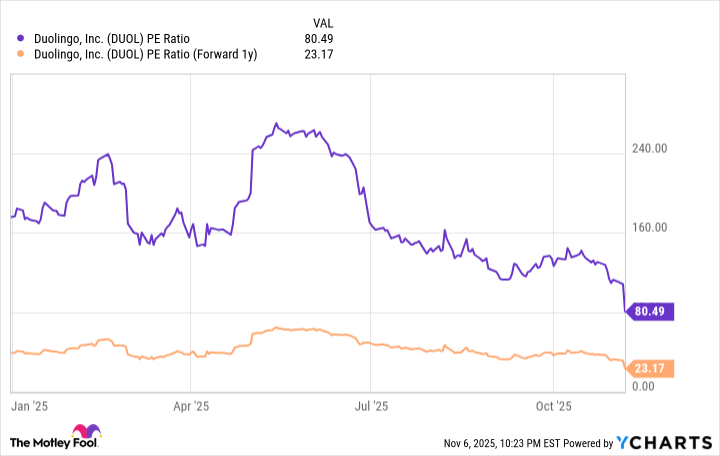

Similarly, Duolingo's price-to-earnings (P/E) ratio has plummeted from over 240 earlier this year to around 80 as I write this. That's still very high considering the S&P 500 (^GSPC +0.32%) trades at a P/E ratio of 26.2. However, Wall Street's consensus estimate (according to Yahoo! Finance) suggests Duolingo's earnings could come in at $8.04 per share in 2026, placing its stock at a forward P/E ratio of just 23.1.

DUOL PE Ratio data by YCharts

In summary, after being undeniably expensive just six months ago, Duolingo stock is starting to look cheap. The key risk is how much the company's recent strategy shift will affect its future financial results, but as long as users continue to find value in the platform, strong revenue and earnings growth should follow.