Palantir (PLTR 3.47%) has been one of the top stocks to own in 2025, as it has more than doubled. However, it's down about 20% from its all-time highs as the market has shown a bit of disdain toward high-flying artificial intelligence (AI) stocks. The primary question to answer: Is this pullback warranted, or is it a buying opportunity?

I think there's one warning signal that's fairly obvious that investors must take note of, and it could save them from making a huge investment mistake.

Image source: Getty Images.

Palantir's business is rapidly growing

Palantir makes artificial intelligence-driven data analytics software that helps its clients make the best decisions possible. Originally, Palantir's software started off as a government-focused product, but eventually expanded to the commercial side and saw huge adoption there as well.

Both customer cohorts are extremely important for Palantir, as commercial revenue totaled $548 million during Q3 and government revenue reached $633 million. That's a healthy split between each customer base, and it can provide some balance if one segment is struggling while the other is booming. However, both customer groups have been rapidly expanding their spending with Palantir.

NASDAQ: PLTR

Key Data Points

One of the primary growth drivers for Palantir is AIP, which allows its clients to deploy generative AI-powered agents to automate some of the decision-making tasks that humans would normally do. This product has seen widespread adoption and has pushed Palantir's stock to new heights.

During Q3, revenue rose 63% year over year to $1.18 billion. The split between commercial and government growth was fairly even, with commercial revenue rising 73% and government revenue increasing by 55%. The primary difference was in Palantir's U.S. versus international growth, as Palantir's U.S. commercial revenue rose a jaw-dropping 121% while U.S. government growth was 52%. That indicates that foreign governments are adopting Palantir's software faster than the U.S., but international commercial clients are less likely to be AI adopters. This shouldn't come as a surprise, as AI adoption has been relatively slow in key markets like Europe.

However, this also isn't a flashing warning sign that investors should be paying attention to.

Palantir's stock is still valued at a massive premium

Despite the sell-off, Palantir's stock trades for a very high premium.

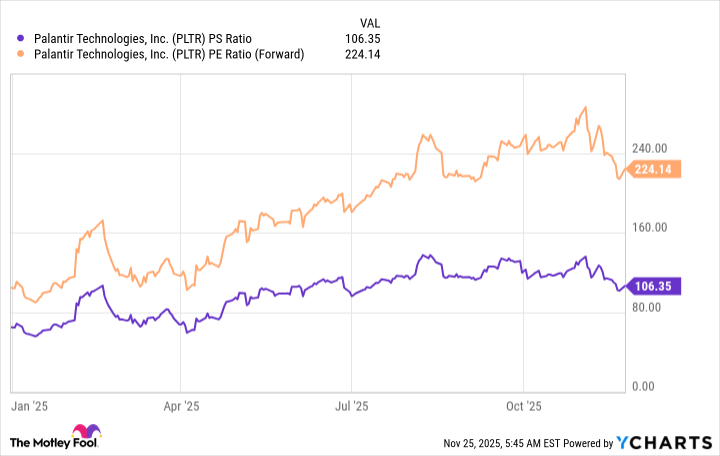

PLTR PS Ratio data by YCharts

At 224 times forward earnings and 106 times sales, Palantir is among the most expensive stocks in the market. This is the big, flashing warning signal that investors can't afford to miss, as these valuations convey massive growth baked into the stock.

For example, take Nvidia. Nvidia is posting fairly similar results to Palantir, as its revenue grew 62% year over year versus Palantir's 63% growth. I'll buy the argument that Palantir should have some premium over Nvidia due to Palantir's product being a recurring expense. However, Nvidia's stock trades for 39 times forward earnings and 24 times sales.

For Palantir to return to a far more reasonable valuation, let's say 50 times forward earnings, it would need to more than quadruple its earnings over the next few years. Should it maintain a 60% growth rate, it will take a little over three years to accomplish that goal.

So, the question is: Is it worth paying for three years' growth up front to own Palantir's stock when other investments are growing at a similar pace that trade for a reasonable valuation now? I don't think the answer is yes, as the price you must pay for Palantir's stock is far too high. Palantir's stock still has a ways to tumble before it makes sense to invest in, but if it does decline and can maintain its growth, I'll be among the first to buy, as it is a truly incredible business.