Kraft Heinz (KHC 1.02%) is a food conglomerate anchored by its two familiar namesake brands. Kraft and Heinz, however, are only two product lines in a large food and beverage portfolio that includes assets such as Kool-Aid, Oscar Mayer, and Jell-O.

But it isn't easy to cook up a tasty stock from such a disparate collection of veteran brands. Kraft Heinz hasn't been all that delicious for its shareholders -- at least, in its present form.

Image source: Getty Images.

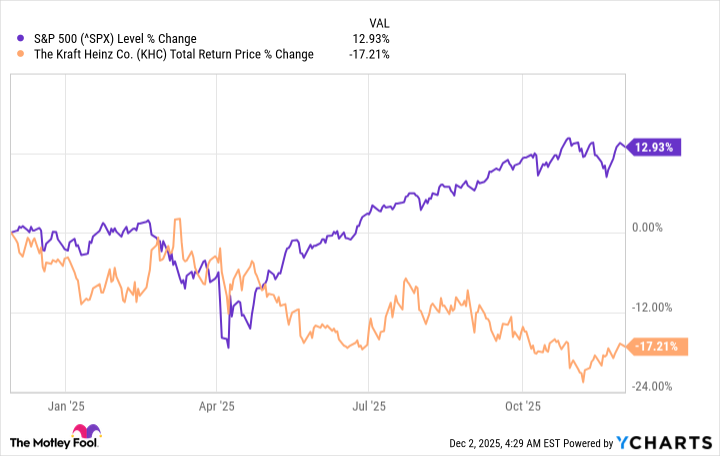

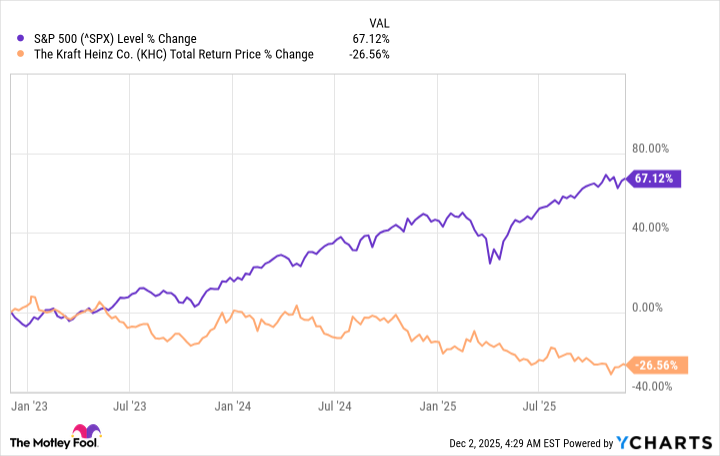

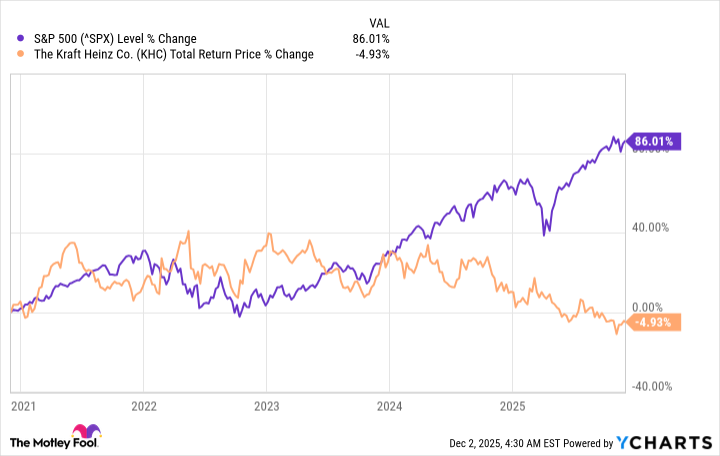

A chronic underperformer

When looking at a trio of trailing time periods -- one, three, and five years -- what's striking is how consistently Kraft Heinz has underperformed the market (represented here by the S&P 500 index). That's when accounting for the stock's total return, which includes both capital gains and the company's regular quarterly dividend payments.

To me, the two main challenges for Kraft Heinz are: 1) the bulk of its portfolio is mature (some might even say stale), and 2) most of these products aren't as favored as they once were, since a great many people have shifted to healthier or more exotic choices over the years.

As a result, the company hasn't managed to gain any altitude on the top line. Since 2020, it has posted only two increases in annual revenue. The 2024 take of $25.8 billion represented a 3% slide from the previous year's result, and was also notably below the 2020 figure ($26.2 billion).

NASDAQ: KHC

Key Data Points

Splitsville

In September, management announced plans to divide the present Kraft Heinz into two separate businesses.

It's essentially attempting to split up the company's billion-dollar (in terms of annual sales) brands. One company will be anchored by Heinz, along with Kraft Macaroni and Cheese and Philadelphia Cream Cheese. The other is to be led by Oscar Meyer, Lunchables snacks, and the Kraft Singles cheese line.

Kraft Heinz essentially stated that the split will enable its successors to devote more resources and attention to the respective products in their portfolios.

I'm not sure I buy this, since those uninspiring revenue numbers don't feel like they're the result of brand neglect. Personally, I see Heinz, Philly, Lunchables, and Singles nearly everywhere I shop. To me, the problem is that these products are steady, unexciting refrigerator mainstays in a world where tastes have evolved and broadened.

One major attraction of Kraft Heinz stock (at least in its present form) is its high-yield dividend, which presently pays out at 6.3%. While top-line growth is lacking, the portfolio certainly generates a lot of the green stuff. The company's free cash flow was just under $3.2 billion in 2024, far more than enough to fund that juicy payout.

While I'm a dividend fan, I wouldn't yield to temptation with this one. In the likely event that Kraft Heinz (and its successors) continue to post mediocre results, the stock's price is unlikely to tread water. The same goes for the total return.

Kraft Heinz has its advantages as a business. It isn't easy to build and maintain a robust portfolio of high-visibility brands, and that high-yield dividend is tantalizing. Neither looks like it'll push the stock higher, though, and that makes it a pass for me.