Tesla (TSLA 2.97%) is one of nine American companies with a market capitalization of $1 trillion or more, but I think it could drop out of that exclusive club in 2026. Its stock is trading at a sky-high valuation, which not only limits potential upside in the near term, but also opens the door to a sharp correction.

Investors are paying a hefty premium for Tesla stock in the hope the company's Cybercab autonomous robotaxi and Optimus humanoid robot become wildly successful. It's entirely possible that will happen, but both products are years away from commercializing at scale. In the meantime, most of Tesla's revenue comes from its electric vehicle (EV) business, which is on track for a second straight year of declining sales.

Image source: Tesla.

The competition is eating Tesla's lunch in the EV business

Tesla used to be the dominant player in the EV industry. After launching its flagship Model S in 2011, it expanded its fleet to include the Model 3, Model Y, Model X, and Cybertruck, which fueled consistent annual sales growth until 2024, when deliveries declined by 1% to 1.79 million cars.

The decline accelerated in 2025, with deliveries sinking by 6% through the first three quarters of the year. According to prediction platform Kalshi, Tesla is expected to sell around 430,000 EVs during the fourth quarter, which will take its 2025 total to 1.64 million units. That would be down 8% from its 2024 result.

A sharp increase in competition in key markets like China and Europe has pressured Tesla's sales all year. In November, for example, new Tesla registrations plummeted by 20% year over year in Germany, by 49% in Denmark, by 58% in France, and by 59% in Sweden.

Consumers are opting for cheaper EVs instead. China-based BYD (BYDDY 0.32%) sells its entry-level Dolphin Surf EV for just $26,900 across Europe, so it's much cheaper than Tesla's Model 3, which starts at around $44,300. As a result, it's no surprise BYD sold more than twice as many cars as Tesla in Germany during November, with its deliveries surging ninefold year over year in that country.

The Cybercab and Optimus are years away from meaningful revenue

Tesla is on track to generate $95 billion in revenue this year, with around 75% coming from EV sales. However, forecasts from Wall Street analysts and even CEO Elon Musk himself suggest the company's Cybercab robotaxi and Optimus robot could fuel astronomical growth in the future.

NASDAQ: TSLA

Key Data Points

The Cybercab will run on Tesla's artificial intelligence-powered full self-driving (FSD) software, so it will be capable of autonomously hauling passengers, which will unlock a new revenue stream. Cathie Wood's Ark Investment Management believes the robotaxi will add a whopping $756 billion to Tesla's annual revenue by 2029, so it could trounce the EV business.

But there are some caveats. First, Tesla's FSD software isn't approved for unsupervised use anywhere in the U.S. right now, leaving the Cybercab grounded. Second, the robotaxi won't enter mass production until 2026, and it will take a couple of years to achieve scale. Third, Tesla is already behind, because Alphabet's Waymo is completing a whopping 450,000 paid autonomous trips per week across five U.S. cities with its robotaxi.

Turning to Optimus, Musk believes the humanoid robot will contribute a staggering $10 trillion to Tesla's revenue over the long term. He thinks robots will outnumber humans by 2040 because they can be applied practically anywhere, from households to factories.

Tesla's latest version, Optimus 3, won't enter mass production until late 2026, so it will be a while before it generates meaningful revenue. But Musk expects production to scale to 1 million annual units very quickly, and he thinks Tesla could be making up to 100 million robots annually within a few years.

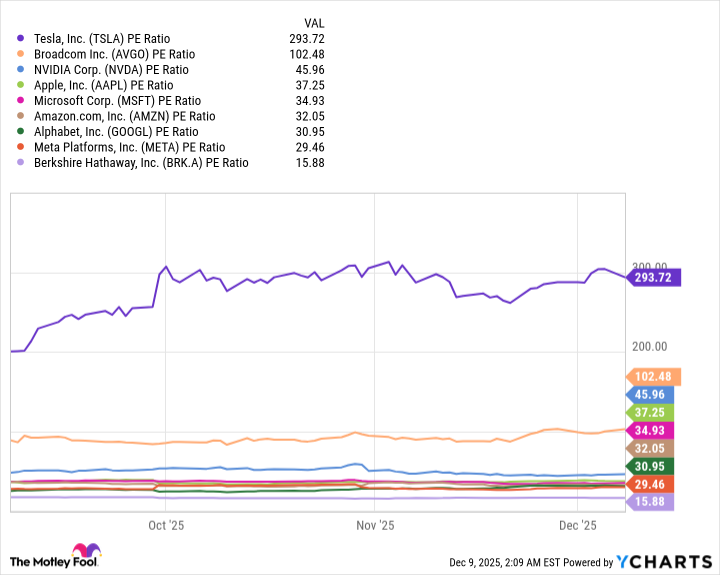

Tesla is the most expensive trillion-dollar stock by far

Based on Tesla's trailing-12-month earnings of $1.44 per share, its stock is trading at a sky-high price-to-earnings (P/E) ratio of 293. That makes it the most expensive stock in the $1 trillion club by a country mile:

Data by YCharts

The majority of Tesla's revenue is likely to come from its EV business yet again in 2026, so if sales continue to decline, I think a sharp correction in its stock might be in the cards, especially if there are any delays to the commercialization of the Cybercab and Optimus.

Tesla has a market cap of $1.38 trillion as I write this, so its stock would have to fall by 28% next year for the company to drop out of the trillion-dollar club. However, the stock would have to plunge by 65% just to trade in line with the next most expensive trillion-dollar stock, Broadcom, which has a P/E ratio of 102. That would push Tesla's market cap down to $483 billion, and yet its stock would still be pricey.