Over the last few decades, banking in the United States has gone digital. The same transition is now happening in Latin America, and it is being driven by one company above all else: Nu Holdings (NU 3.33%). The digital banking mobile app is disrupting the stodgy legacy institutions in Brazil and Mexico, and now has over 100 million customers, making it larger by customer count than every bank in the United States.

The stock has soared over the last year, but still trades below $18 as of this writing on Jan. 20, 2026. Does that make it a buy right now?

NYSE: NU

Key Data Points

Rising revenue, declining per-customer costs

Given the aggressively punitive business models of legacy banks in places such as Mexico and Brazil, Nu Bank has easily been able to win customers to its digital-only banking solution. Instead of charging high fees on cash withdrawals, making customers wait hours in line at branches, and utilizing frustratingly slow technology solutions, Nu Bank has built a customer friendly banking app.

Unsurprisingly, this has led to the wide adoption of its financial services products. Customers now number 110 million in Brazil and 13 million in Mexico, with the latter growing at an exponential rate. Colombia is also seeing wide adoption, but it will be less important for the Nu Holdings business given its smaller economy.

At the same time it is adding a massive amount of customers, Nu Bank is also growing its revenue per customer while decreasing per-customer costs. Average revenue per active customer is now $12.50 in Mexico as of the latest quarter, compared to $5.20 in 2021. The cost per customer has gone from $3 to $1 as it gains greater scale.

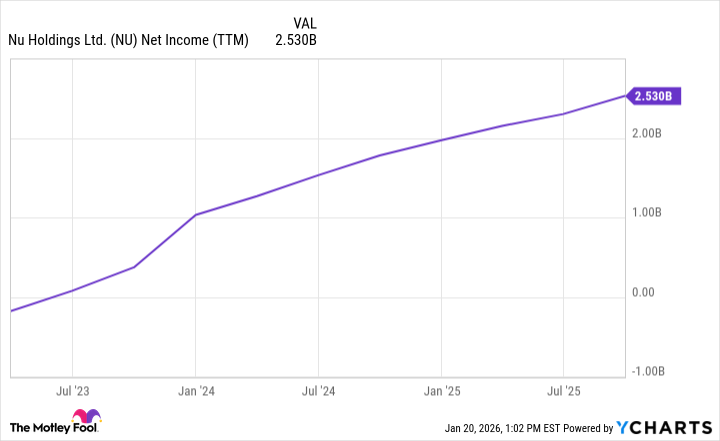

This dynamic -- which is also happening in Brazil -- is why Nu Holdings' net income has gone from breakeven to $2.5 billion within the last three years.

Image source: Getty Images.

Multiple new markets to tackle

Even though Nu Bank has over 100 million customers today, it is only operating in three Latin American countries: Brazil, Mexico, and Colombia. These are the largest countries in the region by population, but it still leaves the business with many other markets to disrupt, with the total population of the greater region exceeding 600 million and growing.

Management has hinted it will soon enter new markets such as Chile, Argentina, or Peru. It also recently applied for a banking license in the United States, which could enable it to offer cross-border services to immigrants in the region, helping them connect with friends and family back home.

Overall, Nu Bank not only has room to significantly expand revenue per customer and customer count in Brazil, Mexico, and Colombia, but also a long runway to expand into new markets in North and South America. This gives the business outsize growth potential over the next decade.

NU Net Income (TTM) data by YCharts

Is Nu Holdings stock a buy today?

Today, Nu Holdings trades at a market cap of $81 billion and a price-to-earnings ratio (P/E) of 32.4, based on trailing net income of $2.5 billion.

While expensive for a banking stock, this may prove cheap for investors who hold for the next decade. Nu Holdings has the opportunity to significantly grow its top-line revenue through new customer acquisition and by layering on additional financial services, such as credit cards. At the same time, it is decreasing its cost per customer, which should help its profit margin grow.

It wouldn't be surprising if, five years from now, Nu Holdings is generating $10 billion in annual net income, especially once it tones down its major customer acquisition spending. That would give the stock a P/E of 8 based on the current stock price, which looks cheap even on a five-year forward basis.

Don't think Nu Holdings is a stock to avoid after rising close to 50% in the past year. Shares still look cheap for long-term investors at $18 or below right now.