With well-known tools for image and video editing, document creation, and design, Adobe (ADBE +4.52%) is one of the most renowned software businesses in the world. Adobe stock is also one of the greatest, turning a $10,000 investment 30 years ago into nearly $400,000 today.

However, Adobe stock has been quite disappointing lately. Shares have lost over half of their value over the last four years, and this timing isn't coincidental. The rise of artificial intelligence (AI) has investors concerned about the long-term viability of this tech stalwart.

NASDAQ: ADBE

Key Data Points

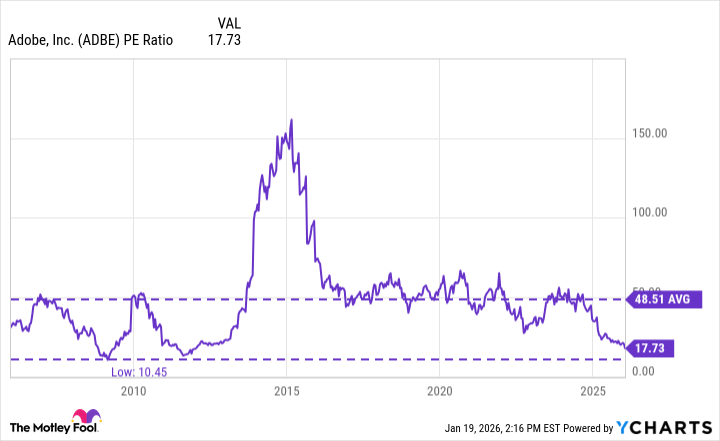

Concerned investors have dropped Adobe stock to a once-in-a-decade valuation. As of this writing, the price-to-earnings (P/E) ratio is 18. In other words, the company's value is about 18 times higher than the profit it's earned over the past year. As the chart shows, it hasn't been this cheap in nearly 20 years.

ADBE PE Ratio data by YCharts

Adobe stock certainly looks cheap. But before investors buy shares, it's important to size up the AI risk -- investors are concerned for good reason.

Is Adobe stock a buy?

Adobe is primarily a high-margin software business. Take one of its most popular products: Photoshop. Photographers rely on Photoshop for image editing and pay a monthly subscription. Adobe isn't the only show in town, but it enjoys a commanding gross profit margin of 89% as of this writing, an all-time high.

Adobe's all-time-high gross margin suggests it has a brand moat -- users highly value its services. However, generative AI tools continue to improve by the day.

Take Alphabet's recent launch of Nano Banana. It offers incredible video editing features, and it's free. This can be incredibly disruptive to a software business and quickly breach any moat that Adobe might have.

Image source: Getty Images.

While the concern is valid, fears may be overblown. Consider that 72% of Adobe's fiscal 2025 revenue came from its Creative & Marketing Professionals segment. This customer base may be a bit more concerned about quality control issues that could come from free AI tools.

Of course, there are higher-quality AI tools that offer paid subscriptions, which could disrupt Adobe. But then again, Adobe offers its own competing AI tools. And these AI products continue to drive top-line growth for the company, considering that its fiscal 2025 annual recurring revenue (ARR) grew by nearly 12% year over year.

I'm inclined to believe that Adobe is safe from the disruption threat of AI due to its large professional customer base and its own AI offerings. If I'm right, Adobe stock is a great deal today at a once-in-a-decade valuation.

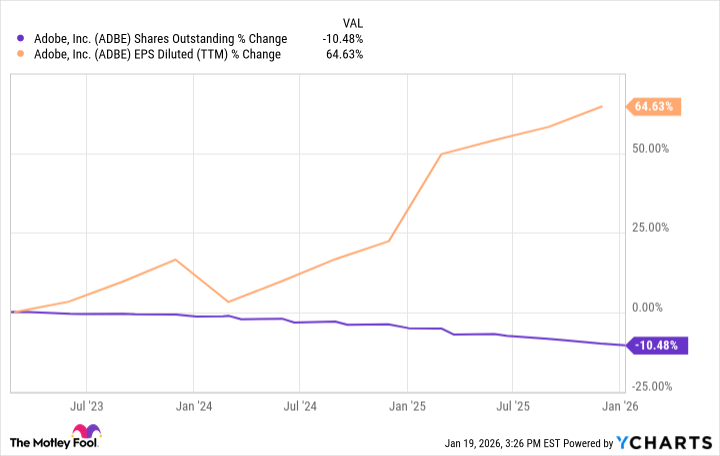

Adobe's management is taking advantage of the cheap stock price by buying back stock. As the stock price has languished, management has reduced the share count by over 10% in just the past three years. Combined with ongoing sales growth and high profitability, the company's per-share profits are growing fast, leading to a forward P/E ratio of just 13.

ADBE Shares Outstanding data by YCharts

In conclusion, the valuation for Adobe stock may be too cheap for opportunistic investors to pass up.