Artificial intelligence (AI) has supercharged several technology stocks over the past three years, as the proliferation of this technology has driven phenomenal revenue and earnings growth for many companies.

AI infrastructure companies that build hardware to run AI workloads in data centers have been among the biggest beneficiaries of this technology's adoption. Micron Technology (MU +3.00%) is one such pick-and-shovel play that enables various AI accelerator chips to handle massive amounts of data for training AI models and inference applications through its memory chips.

Shares of the memory specialist have already shot up nearly 28% in 2026. It won't be surprising to see Micron stock heading higher for the rest of the year, and it may even become one of the best ways to capitalize on AI's growth this year. Let's look at the reasons why.

Image source: Micron Technology.

Unprecedented memory demand will be Micron Technology's biggest catalyst

In a recent interview with Bloomberg, Micron executive Manish Bhatia noted that the shortage of memory chips has intensified in the past quarter. The shortage is a result of the red-hot demand for high-bandwidth memory (HBM) deployed in AI chips such as graphics processing units (GPUs) and custom AI processors.

NASDAQ: MU

Key Data Points

Bhatia added that smartphone and personal computer (PC) manufacturers are also trying to secure their own supply of memory chips. These industries aren't getting enough memory chip supply as data centers are reportedly set to consume a whopping 70% of the memory chips manufactured this year. Moreover, other industries such as automotive, consumer electronics, and television are also trying to secure memory supply for their devices.

It is worth noting that memory chip content in data centers, smartphones, PCs, and other applications has increased due to AI. Companies such as Nvidia and Broadcom are packing more HBM into their chip systems to handle larger datasets more rapidly. Additionally, AI-capable smartphones and PCs require more memory to process on-device AI workloads.

As a result, it is easy to see why Micron management expects the memory crunch to persist beyond this year. Counterpoint Research adds that memory manufacturers are already selling out their 2028 manufacturing capacity. This shortage is pushing up memory prices, which explains why market research firm Omdia sees the memory industry's revenue jumping by more than 80% in 2026 to just over $400 billion.

The company is on track to clock stunning growth in 2026

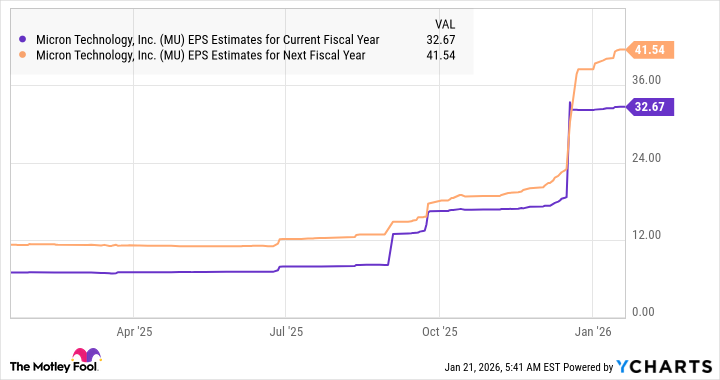

Micron is already clocking stunning revenue and earnings growth, thanks to favorable memory market dynamics. Consensus estimates are projecting a 294% spike in earnings this year to $32.67 per share, followed by another healthy increase next year.

MU EPS Estimates for Current Fiscal Year data by YCharts

Micron, however, could easily outpace the 27% bottom-line increase analysts are forecasting for the next fiscal year (which will begin in August 2026), given the supply-constrained nature of the memory market. Micron's continued outperformance of Wall Street's expectations should pave the way for more upside in this AI stock, both in 2026 and beyond, especially because it trades at just 11.5 times forward earnings.

That's a discount to the tech-laden Nasdaq-100 index's forward earnings multiple of 25.6 (using the index as a proxy for tech stocks). If Micron achieves the remarkable bottom-line growth that it is anticipated to clock and trades in line with the index's average, its stock price could skyrocket further. All this makes Micron one of the best ways to capitalize on the AI boom this year.