With a market cap of $400 billion, big data analytics company Palantir Technologies (PLTR +1.25%) has proven itself to be one of the biggest winners in the generative artificial intelligence (AI) boom. Investors are betting on its ability to help introduce its powerful software-as-a-service (SaaS) tools to the U.S. military and other public sector clients while also enjoying solid adoption with regular enterprise customers.

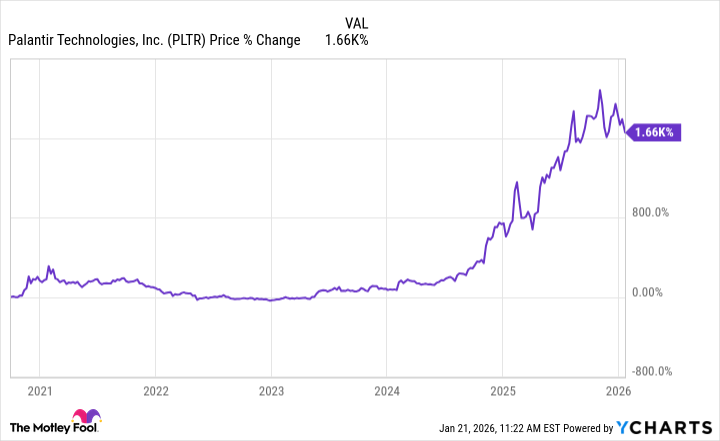

Palantir's business momentum has begun to accelerate in recent years. The company's shares have responded by jumping over 1,700% from their initial public offering (IPO) in 2020. But past performance doesn't guarantee future results, and new investors will be curious to know if Palantir is still capable of multibagger growth. Let's dig deeper to find out.

NASDAQ: PLTR

Key Data Points

What is Palantir's edge?

Organizations generate a massive amount of unstructured data during their operations. And at its core, Palantir's role is to sift through this information to find actionable insights such as fraud patterns, operational trends, and business opportunities. This type of data mining is distinct from the generative AI behind large language models (LLMs). But the two technologies synergize exceptionally well with each other.

Generative AI can allow an operator to interact with data analytics software with simple text-based prompts instead of complex workflows that require significant training. AI can also speed up the data mining process by giving real-time insights in fast-paced scenarios. This technology obviously has military applications. And Palantir is working with the armed forces of U.S. allies like Israel and Ukraine for targeting enemy assets, mine removal, and other battlefield technologies.

The release of Palantir's official Artificial Intelligence Platform (AIP) in mid 2023 seems to have been a watershed moment for the company. It made analysts and investors really start paying attention. Palantir's recent operational performance has also been highly encouraging.

Business is booming

Palantir's third-quarter earnings were a slam-dunk success. Revenue surged 63% year over year to $1.18 billion, driven by eye-popping strength in its U.S. commercial business where sales grew by 121% to $397 million -- roughly 33% of the total. While Palantir's brand image is usually centered around its work with intel services and other government clients, private sector contracts have become the company's core growth driver. This transition comes with opportunities and challenges.

The main advantage is that the private sector is generally larger and more in need of data analytics services (profit-driven companies are under more pressure to drive efficiency gains). These new clients also help diversify Palantir away from political risk, which could become a key challenge because of its involvement in international conflicts and co-founder Peter Thiel, who is an outspoken backer of the Trump administration and close associate of Trump's vice president, JD Vance.

Image source: Getty Images.

The risk is that a future administration may be less willing to do business with a company that is perceived to be too close to partisan politics. Recently, other companies like Tesla, Target, and Anheuser-Busch have demonstrated how dangerous political exposure has become.

Palantir's growing focus on private sector contracts could also expose it to competition from other big data analytics companies like Microsoft (which offers a similar platform called Fabric) and Snowflake. It is important to note that Palantir's AIP hasn't created its own large language models, making it unclear how deep the company's economic moat really is in AI-related services.

What will the next 10 years have in store?

With a price-to-earnings (P/E) multiple of 170, Palantir shares are priced for perfection. Investors who buy the stock now are betting that the company's long-term growth is just getting started. Over a decade-long investment horizon, those investors might be right. However, in the near term, it might make more sense to wait until Palantir's valuation drops a little bit before considering a position in the stock.