The semiconductor industry sits at the heart of the artificial intelligence (AI) boom -- without advanced chips, this revolutionary software wouldn't be possible. But more than just processing power is required.

Micron Technology (MU +7.99%) is a leading supplier of memory and storage chips, not only for data centers (where most AI development happens), but also for personal computers and smartphones, where AI workloads are gradually migrating.

It was one of the best-performing stocks in the semiconductor space in 2025, with a gain of 239%. It's grabbing headlines yet again in 2026 because it has already risen a further 29% in January alone. The question investors have to ask themselves now, though, is how much longer this incredible rally can run.

Image source: Getty Images.

Micron is attracting some high-profile customers

Graphics processing units (GPUs) like those supplied by Nvidia are the primary parallel processing chips used to power AI development and inference. High-bandwidth memory (HBM) in close proximity to those chips unlocks maximum processing speeds from large GPU clusters by keeping the data flowing to them seamlessly. Without it, GPUs would have to constantly pause in their workloads while they wait to receive more information, which is far from ideal with AI software.

Micron's HBM3E data center chip provides 50% more capacity than the competition while consuming 30% less energy. As a result, both Nvidia and Advanced Micro Devices are embedding it in their latest GPUs.

And Micron is preparing to ramp up production of its new HBM4E chip, which it says will improve capacity and energy efficiency by a further 60% and 20%, respectively. The company's entire 2026 supply of those chips is already sold out.

NASDAQ: MU

Key Data Points

Micron CEO Sanjay Mehrotra predicts the market for data center HBM will triple in value by 2028, to over $100 billion annually. This is the company's biggest financial opportunity, but there is also a lot of money to be made in memory chips for consumer devices as a greater share of AI workloads gradually shifts to smartphones and personal computers.

During Micron's fiscal 2026 first quarter, which ended Nov. 27, 59% of its customers' flagship smartphones needed at least 12 gigabytes of memory to support AI applications. That percentage was more than twice what it was in the prior-year period.

Data center growth is fueling a surge in Micron's profits

Micron's total revenue soared 56% year over year to a record $13.6 billion during its fiscal first quarter. The company's cloud memory segment (where it reports its data center HBM sales) was responsible for about $5.3 billion of that -- twice as much revenue as in the prior-year period.

Since there's a general shortage of HBM and Micron's supply is selling out so far in advance, the company has incredible pricing power, which is fueling a surge in its profits. Its earnings soared by 175% to $4.60 per share in fiscal Q1, and there could be even faster growth ahead.

According to management's latest guidance, revenue could rocket higher by 132% year over year to $18.7 billion during its fiscal Q2, which will conclude at the end of February. This is forecast to fuel 480% growth in earnings, which are expected to come in at $8.19 per share.

Investors are now revaluing Micron in light of the incredible earnings growth in its pipeline -- hence, the recent gains in its stock.

How much higher can the stock go?

The semiconductor industry has historically been highly cyclical. In the past, companies would spend a fortune building out infrastructure, but once that process was completed, they wouldn't buy any more chips for a few years (basically until it was time to upgrade). But AI requires so much computing power that some of the biggest data center operators are buying new chips on an annual basis.

Micron stock is positioned to trend higher for as long as this ultra-short upgrade cycle continues. Nvidia CEO Jensen Huang believes infrastructure spending will continue to grow for years, with data center operators potentially investing up to $4 trillion annually by 2030 to meet AI developers' demand for cloud capacity. That would be a huge tailwind for Micron, considering its memory chips are embedded into the industry's best GPUs from both Nvidia and AMD.

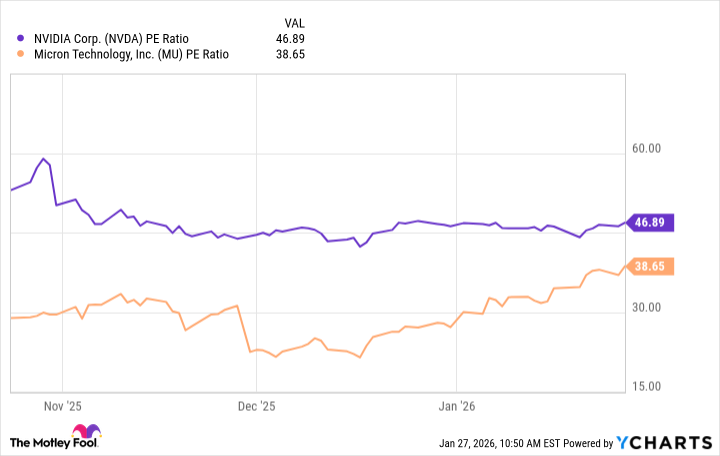

Based on Micron's trailing-12-month earnings of $10.52 per share, its stock is trading at a price-to-earnings ratio (P/E) of 38.6. That's still much cheaper than Nvidia, which trades at a P/E of 46.8.

NVDA PE Ratio data by YCharts.

The picture looks even better on a forward basis. Wall Street's consensus estimate (provided by Yahoo! Finance) is that Micron's earnings will soar to $33.17 per share in fiscal 2026, giving it a forward P/E of just 12.2. From that perspective, it looks like an absolute bargain -- shares would have to more than triple over the next year just to maintain the current P/E of 38.6.

I'm not sure how likely that is to happen because Wall Street knows no company can grow at this pace forever, so investors might want to temper their expectations. However, even if Micron stock doesn't triple this year, it's still likely to crush the broader market, just like it did in 2025.