The bond markets and equity markets appear to be taking different views on the sustainability of artificial intelligence. There are clear signs of stress in credit default swap (CDS) pricing -- the cost to insure against default -- for companies like Oracle (ORCL +4.77%). Yet, in general, stock markets have continued to invest in AI companies. Which side is right, and is AI in a bubble?

Widening bond market skepticism

Oracle's CDS pricing spiked in November. While bond markets can get jittery from time to time, they have remained at elevated levels. Currently, they're at almost four times the levels they were in September. This is a clear sign that the bond market is concerned about Oracle's debt.

Image source: Getty Images.

The concerns center on the ballooning cost of building out data center infrastructure to support AI growth, and specifically on Oracle's $300 billion deal with OpenAI. The latter is widely reported to have internal projections of burning through over $100 billion in cash before it starts generating cash in 2030. That's reportedly the company's view, but the markets are having some doubts over it.

Does it matter?

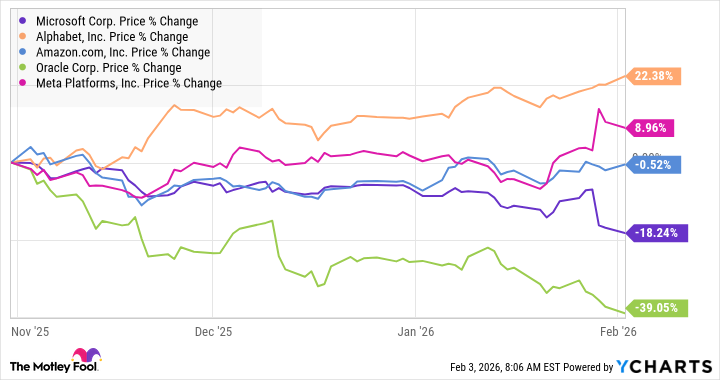

The CDS pricing blowout is concerning, but on closer inspection, the bad news appears to be limited in scope. On that, the equity market appears to agree. Below is a look at share price charts of leading hyperscalers.

It's no accident that Oracle and Microsoft have underperformed, as Microsoft recently disclosed that 45% of its backlog is due to OpenAI. Meanwhile, the outperformer, Alphabet (GOOG 2.48%) (GOOGL 2.46%), has minimal exposure to OpenAI.

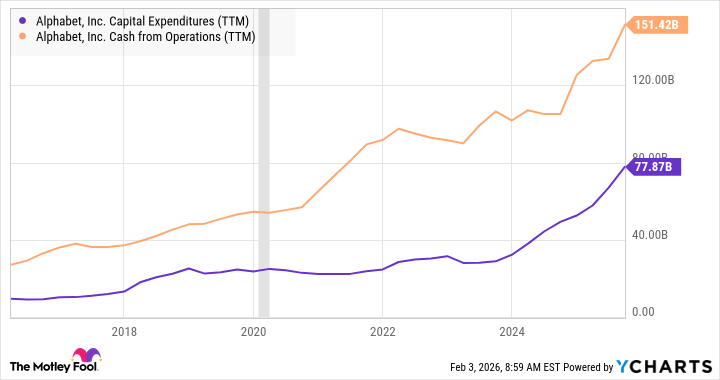

Alphabet is also in a much better financial position to support its AI-related capital spending.

GOOG Capital Expenditures (TTM) data by YCharts.

Is AI in a bubble?

As ever, the answer to whether AI is a bubble is nuanced. History suggests that companies overreach during technological revolutions, and capital will inevitably flow to ultimately unproductive sources, driven by a "me too" mentality. That's just how human beings and cycles work.

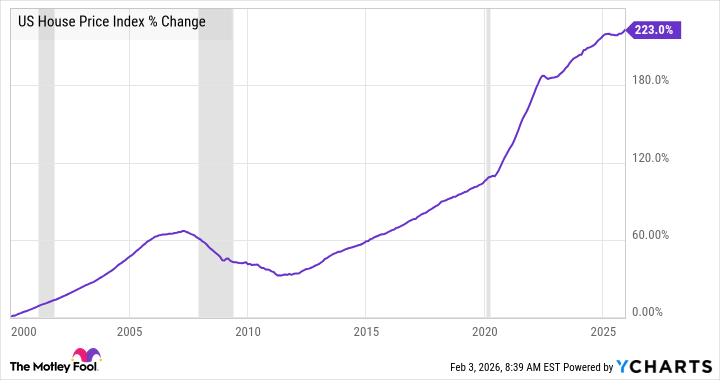

However, it's very difficult to predict when this will happen. For example, U.S. housing prices peaked in July 2006, about two years before the financial crisis of 2008-2009, and are now significantly higher. No one knew when the peak would come, and selling your house during the crash didn't turn out to be a great long-term decision.

US House Price Index data by YCharts.

If the bond and equity markets are becoming more discerning about the quality of the AI-exposed companies they invest in, with Alphabet the highest-quality company, it's likely to rein in some of the less realistic plans. That would be a good thing and make AI growth more sustainable over the long term, as markets need the effective pricing of risk to function properly.