Palantir Technologies (PLTR 6.87%) reported stellar fourth-quarter earnings on Feb. 2, crushing analyst expectations. The stock popped on the news. Still, the shares are 33% below their November peak. So is now the time to buy?

What does Palantir actually do?

Palantir's main business is building software platforms that help large organizations make sense of their data. Its two flagship products -- Gotham for government and defense clients, and Foundry for commercial clients -- are like an operating system that integrates information and data scattered across disparate systems into a single, usable platform.

Then, decision-makers, with the help of AI, can easily spot patterns, run analyses, predict outcomes, and run their organizations more effectively.

NASDAQ: PLTR

Key Data Points

The numbers tell a compelling growth story

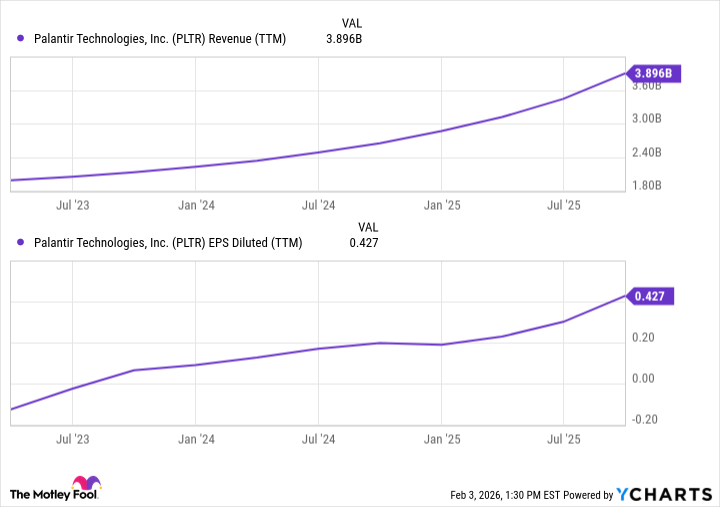

It's clear the company is doing something right. Palantir's sales and earnings growth have been incredible during the past few years. You can see the lightning pace in the chart below.

Palantir's incredible revenue and earnings growth.

PLTR Revenue (TTM) data by YCharts.

Although Palantir's bread and butter has always been serving government and defense clients, and it continues to see success there, the key driver of the eye-popping, top-line growth is what appears to be an insatiable demand from U.S. commercial clients. In the fourth quarter the company reported 137% year-over-year (YOY) growth in its domestic commercial business, up nearly 28% from the previous quarter.

This acceleration in commercial demand was fueled largely by the company's Artificial Intelligence Platform (AIP), which leverages recent advances in generative AI to supercharge its Foundry product.

Palantir's competitive advantage is strong

The real differentiator here is Palantir's bespoke approach. Rather than selling software and wishing customers good luck, the company carefully tailors its platform to each customer, taking great pains to truly understand the organization and its needs. Its forward-deployed engineers (FDEs) embed themselves with the client for months. And although the upfront investment is greater, the end result is so much more powerful -- not just for the client but for Palantir too.

This hands-on approach creates a formidable and durable competitive moat. Once Palantir's engineers have spent months integrating with a client's systems and training their teams, switching to a competitor means repeating that entire expensive process or attempting to build their own system in-house; most organizations quickly realize this isn't feasible.

Image source: Getty Images.

The moat is strengthened, too, by Palantir's use of combat jargon and military language -- like calling FDEs "Deltas" (members of an elite U.S. Army special operations group). It's a clever way to create an emotional bond with its clients, facing a common enemy.

Beyond the valuation, there's an issue investors can't ignore

As well as the company is executing, the very large elephant in the room is its valuation: Its forward price-to-earnings ratio (P/E) of about 160 is extreme by any standard.

To justify its more than $360 billion market cap, Palantir would have to grow consistently by about 30% to 40% annually for the next decade. While it is easily beating that right now, I'm not convinced it will be able to a few years from now.

The company will have its hands full trying to stay ahead of the competition, whether tech behemoths like Microsoft or private players like Databricks. The company will likely need to look outside of the U.S. to sustain serious growth over time, and I think this will be a major hurdle. In fact, it has already hit a wall outside the U.S. Its year-over-year growth in the U.K. has stalled at 10%, while growth has slowed in the rest of the world.

Although the headlines focus on its domestic growth, I think this is the real story for long-term investors.

Palantir is priced for perfection. And that's why I continue to believe it's overpriced. I would caution investors to look elsewhere.