The sell-off in software-as-a-service (SaaS) stocks has evolved from a pullback to a downturn, and now to a full-throttle crash. An exchange-traded fund (ETF) that closely tracks the sector -- The iShares Expanded Tech Software Sector ETF (IGV 0.88%) -- is down 24.6% year to date at the time of this writing, while the broader tech sector has fallen 5.8%.

Last week, Anthropic announced a new plugin for legal applications on its Claude Cowork platform that could challenge the functionality of existing enterprise software. Then on Feb. 5, Anthropic published a press release introducing Claude Opus 4.6 -- its latest model. Opus 4.6 improves Claude's coding skills, agentic tasks, and capabilities within the Cowork platform, including the ability to run financial analyses, conduct research, and create documents, spreadsheets, presentations, and more.

SaaS companies used to command premium valuations relative to the market because of their recurring revenue and wide moats. But those moats are being eroded by artificial intelligence (AI) models that can perform tasks normally handled manually using enterprise software. Additionally, SaaS companies depend on user growth, but if a single user can now accomplish the workload that used to require several subscriptions, that means less revenue for enterprise software companies.

With that, here are three big mistakes folks invested in software stocks or those interested in buying the dip should avoid.

Image source: Getty Images.

1. Assuming a stock can't go lower

If you've been investing long enough, then you've seen euphoria and panic take over stock prices. Unprofitable companies with investment theses built on houses of cards can run to nosebleed valuations. And companies with exceptional business models and long runways for earnings growth can sell off at dirt-cheap prices for reasons that have nothing to do with fundamentals.

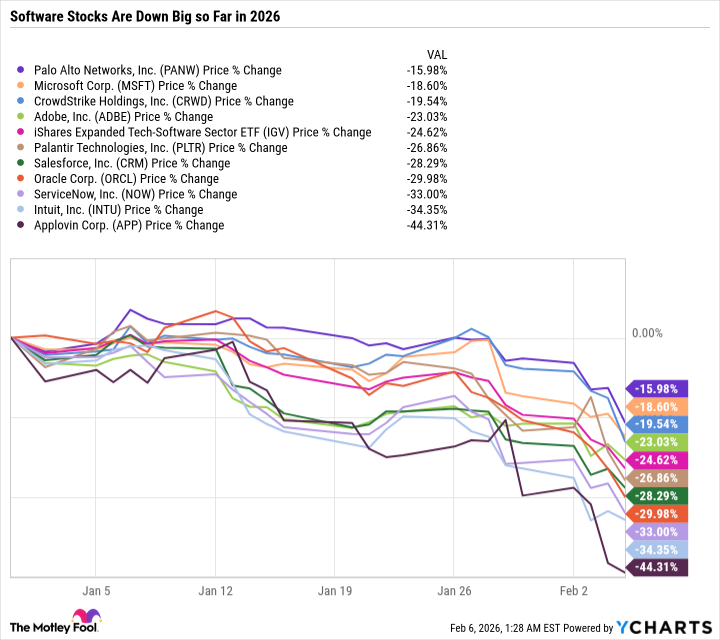

It's a common mistake to look at a beaten-down stock, especially one that is down big in a short period, and assume that it can't keep falling. Just look at a chart of the 10 largest holdings in the iShares Expanded Tech Software Sector ETF.

Data by YCharts.

The sell-off was already in full swing in mid-January, but it has intensified in recent weeks. So, assuming that just because a stock was down a lot to kick off the year would have been a big mistake. Or assuming that just because Microsoft (MSFT 0.73%) is highly diversified doesn't mean it can't sell off in a major way.

It's also worth noting that many top software stocks didn't begin falling in 2026. Salesforce was one of the worst-performing stocks in the Dow Jones Industrial Average last year.

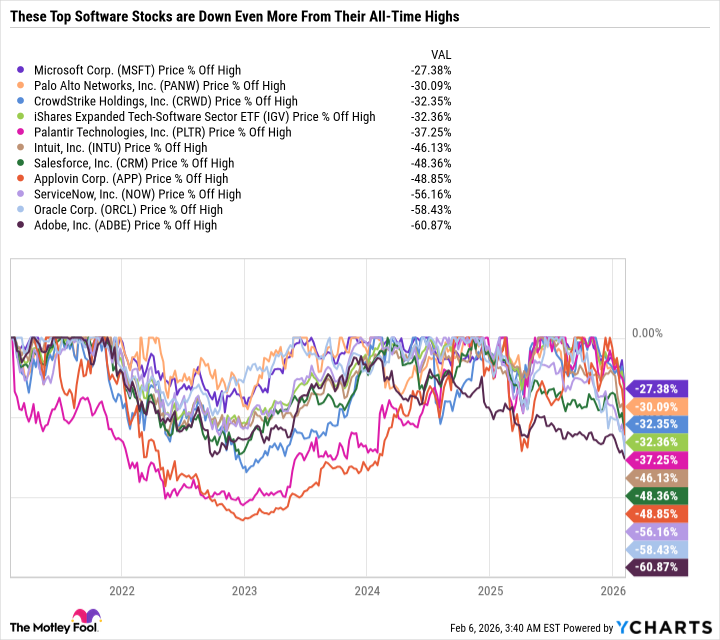

Here's a look at those same 10 companies, showing how much they are down from their all-time highs.

Data by YCharts.

Not long ago, stocks like Adobe (ADBE 1.43%) and Salesforce (CRM +2.36%) were among some of the largest companies in the tech sector by market cap. Now Salesforce has been kicked out of the top 10, and Adobe isn't even in the top 20.

2. Buying a stock just because it fell

As consumers, we're conditioned to see a lower price as a better buying opportunity. But shares of stock represent partial ownership in a company, not ownership of a good or commodity. So if the price falls while the fundamentals also deteriorate, the sell-off is justified.

While some software stocks are certainly way oversold, unprecedented disruptions are impacting the industry. So instead of just buying the stocks that have sold off the most, investors should focus on buying companies that are the best value based on their fundamentals, like financial health, revenue streams, earnings potential, etc.

As an example, I find Microsoft to be the most compelling buy amid the software stock crash. There are plenty of stocks that have fallen much more than Microsoft, but Microsoft stands out as the best value on a risk-to-reward basis. The company is the second-largest player in cloud computing behind Amazon Web Services, and is a major player in AI with its partnership with OpenAI, which powers a lot of its embedded intelligence, like Copilot.

Microsoft also makes money from gaming, consumer products, and owns LinkedIn and GitHub. Microsoft's software suite is heavily embedded in both enterprise, consumer, and student workflows. And Microsoft is an AI-forward company that can rapidly deploy user-friendly AI tools.

Microsoft is selling off because investors are worried it is overspending on AI and is too dependent on OpenAI, which is being heavily challenged by Anthropic's Claude model. But at just 24.6 times earnings, those risks are already baked into Microsoft's valuation.

3. Amplifying the pros and downplaying the cons

Focusing solely on a company's strengths without considering risks is a mistake that is magnified during a sell-off. As optimistic as I am about Microsoft's long-term potential, I also understand why the stock is under pressure and could continue selling off if Microsoft fails to convert its ramped-up AI spending into earnings growth.

Many software stocks are generating impeccable earnings growth and all-time high profits. The sell-off in a company like ServiceNow (NOW 2.30%) can be especially perplexing given that it reported excellent AI-driven and agentic AI growth in its latest quarter.

ServiceNow is also trading at a multiyear low valuation. At first glance, it seems like one of the most no-brainer software stocks to buy now. But before backing up the truck, it's important to consider risks to its business -- namely that rival AI tools will be able to automate tasks and improve operational efficiency more effectively than ServiceNow's offering. Additionally, ServiceNow has been spending billions acquiring companies -- which could accelerate future growth but adds risks if the deals don't pay off.

Stay even-keeled amid market turbulence

Industrywide sell-offs present impeccable buying opportunities, but they also require significant discipline.

Before buying software stocks on the dip, challenge yourself by asking what could go wrong, and then decide whether those risks are worth taking or if there are better opportunities elsewhere.