Investors have been forced to get comfortable with richly priced stocks of late. After all, they're the only ones that have been performing well. If you're willing to do a little digging though, you'll find a handful of names worth owning that have actually fallen back to dirt-cheap valuations.

Here's a closer look at three of these best bets in the market today.

Image source: Getty Images.

Sprouts Farmers Market

It's been a wild ride for Sprouts Farmers Market (SFM +4.31%) since 2024. The stock soared that year thanks to the health-minded grocery chain's growth. Since peaking in the middle of last year, SFM stock has tumbled more than 60%, reaching a two-year low just this month.

The sellers, however, have arguably overshot their target. The stock is now priced at less-than 12 times this year's very plausible, projected per-share profit of $5.74, up from 2025's likely full-year comparison of $5.27. The stock's also currently trading 60% below analysts' current consensus price target of $108.73.

NASDAQ: SFM

Key Data Points

The crux of the bullish argument here, of course, is the growth of its core business. While consumers tend to talk about eating healthier more than they actually do it (recent Pew Research says cost and taste are still the most important factors), industry research outfit Technavio predicts the health and wellness food business is poised to grow by nearly 10% per year through 2029.

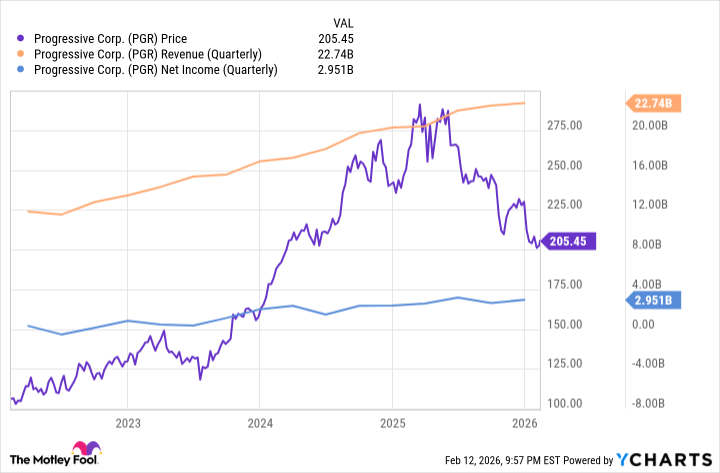

Progressive

The insurance business can be a tricky one for insurers to navigate. Reimbursements are practically impossible to predict with any precision from one year to the next, while competitive and regulatory factors are forever changing. That's one of the big reasons shares of insurer Progressive (PGR +0.98%) have struggled for nearly a year now -- its revenue growth seems to be slowing.

NYSE: PGR

Key Data Points

As was the case with Sprouts, the bears may have overshot their target and done so for a misunderstood reason. You can step into this name at less-than 13 times the coming year's projected earnings. Perhaps just as compelling, you can step into it while the stock's forward-looking dividend yield stands at just under 6.7%.

And the misunderstanding? While this company's rate of revenue growth may be slowing, on a whole-dollar basis, it's making as much (no word play intended) progress as it ever has.

It's also worth adding that while the insurance business can be volatile from one year to the next, for multi-year time frames, it tends to do reliably well. These companies' actuaries have gotten very, very good at the industry's mathematics.

PayPal

Lastly, while there's no denying PayPal's (PYPL 2.00%) growth is slowing down as the well-matured digital payment space becomes even more crowded with new competition, the market seems to be pricing in an outright collapse that just isn't in the cards. As of the latest look, PayPal stock is valued at less-than eight times this year's expected profits of $5.34 per share.

Do keep your expectations in check. Again, the digital wallet space has become fiercely competitive. Single-digit revenue growth is the new norm here.

NASDAQ: PYPL

Key Data Points

Just respect the fact that the original powerhouse of this space still enjoys a commanding control of about 40% of the online payment market. Incoming CEO Enrique Lores -- currently CEO of HP -- will have a great foundation to start with when he takes the helm next month and brings some fresh ideas and perspective to the table. This may be exactly what PayPal's been needing for a while now.