Advanced Micro Devices (AMD +1.78%) stock got off to a promising start in 2026, but it has lost its wheels of late following the release of its fourth-quarter 2025 results on Feb. 3.

The sell-off triggered by AMD's quarterly report explains why the stock is down 4.8% so far in 2026. The PHLX Semiconductor Sector index, on the other hand, has jumped roughly 15.5% this year. Savvy investors may now be wondering if it would be a good idea to capitalize on AMD stock's pullback and buy it right now.

Image source: Getty Images.

AMD's sell-off isn't justified

Shares of AMD dropped more than 17% after its latest quarterly report, even though the company delivered impressive growth in both revenue and earnings. What's more, AMD's guidance for the current quarter was solid, with the company projecting a 32% increase in revenue in Q2 to $9.8 billion. The chip designer anticipates its non-GAAP (adjusted) gross margin to land at 55% in the current quarter, an improvement of 2 percentage points over last year.

NASDAQ: AMD

Key Data Points

So, AMD seems poised to register a nice jump in its bottom line once again in Q2, following a 40% year-over-year jump in the previous quarter. It is worth noting that AMD's earnings and outlook exceeded Wall Street's expectations. Investors, however, were probably expecting faster growth from AMD, especially considering that the stock has clocked terrific gains of 83% in the past year.

Simply put, it looks like AMD investors were looking for a reason to book profits in the stock following its healthy surge in the past year. However, the good news is that the drop has opened an opportunity for investors to buy AMD stock at a relatively attractive valuation.

It is trading at 31 times forward earnings right now, and buying it at this level looks like a no-brainer.

Terrific earnings growth should help AMD regain its mojo

AMD's data center and the client and gaming business segments are seeing robust growth. The central processing units (CPUs) and graphics cards that AMD designs are deployed in both data centers and personal computers (PCs). The proliferation of artificial intelligence (AI) in these applications is a tailwind for the company.

While data center operators employ AMD's Epyc server processors and Instinct graphics accelerators to tackle AI workloads, its Ryzen PC processors are gaining share on the back of the company's AI-focused push in this market.

Importantly, the ramp-up of the company's latest AI data center processors boosted its margins. The improvement in the product mix explains why AMD anticipates an improvement in its gross margin in the current quarter. This is probably the reason why analysts forecast a 60% increase in AMD's earnings in both 2026 and 2027, well above the average earnings growth of companies in the S&P 500 index.

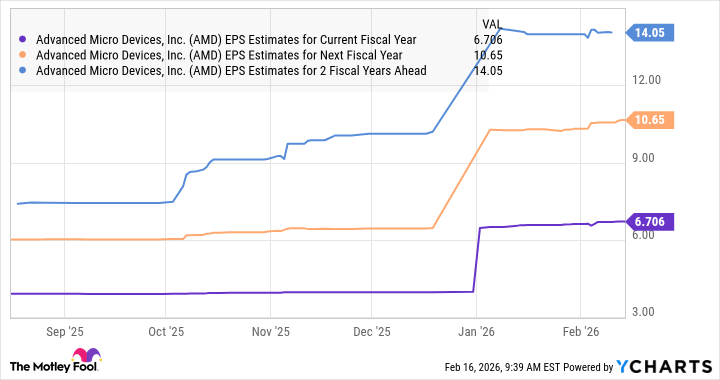

Data by YCharts.

AMD delivered $4.17 per share in earnings last year. The above chart tells us that its bottom line is on track to more than triple in just three years. Assuming AMD trades at 22 times earnings after three years (in line with the S&P 500 index's forward earnings multiple) and achieves $14.05 per share in earnings, its stock price could hit $309 -- a potential increase of 51% from current levels.

This AI stock, however, could do better than that as its soaring earnings growth is likely to be rewarded with a higher multiple, which is why it makes sense to buy AMD following its recent dip, as it can regain its momentum.