On Feb. 19, Walmart (WMT +1.47%) reminded investors why it's one of the strongest businesses in the world when it reported financial results for the fiscal fourth quarter of 2026. In fiscal 2026 (which ended in January), the company generated revenue of more than $700 billion, up nearly 5% year over year.

But the bigger news was that its profits jumped even further.

Few businesses stand toe-to-toe with Walmart's scale. But Costco Wholesale (COST +1.10%) comes closer than most. The company will report financial results for the fiscal second quarter of 2026 on March 5. Over the previous four quarters, it's generated revenue of more than $280 billion.

Image source: Getty Images.

Walmart and Costco stand tall among the largest consumer stocks in the world. But I believe Walmart stock is the better buy today, as I'll explain.

Costco's incredible strength

In a nutshell, Costco sells its products with very little markup, choosing instead to make most of its money from membership sales. This business model makes sense: The better deals it has, the more likely people are to want a membership.

Memberships at Costco are booming. In the fiscal first quarter of 2026, overall memberships were up 5% year over year to 146 million. And its higher-priced executive memberships were up a stronger 9%. This resulted in a 14% jump in membership income.

NASDAQ: COST

Key Data Points

This double-digit jump in membership income greatly helps Costco's bottom line. Q1 net income was up 11%, which is impressive for a business of this size with relatively low growth.

Walmart's digital drive

As mentioned, Walmart's profits are growing faster than sales, just like Costco. For Walmart, this multi-year trend is the direct result of the company's growth in digital offerings, including e-commerce and advertising.

Walmart's global e-commerce sales reached 23% of total sales in fiscal 2026, a record high. The company's e-commerce platforms have better economics than in-store sales. But the platforms also allow for high-margin third-party sales.

NASDAQ: WMT

Key Data Points

Additionally, Walmart is boosting profits with digital advertising. Again, its e-commerce platforms are helpful here. But the company also has a connected-TV advertising platform through its acquisition of Vizio. Walmart is in a better position than most with digital advertising because it has an incredible amount of first-party consumer data.

Walmart's digital drive is expected to keep profits rising slightly faster than sales, which is a good trend for investors.

Why Walmart wins for me

In reality, the business prospects for Walmart and Costco are about the same, in my view: I expect sales to rise at a modest pace, with profits rising by a slightly greater amount. Therefore, I would expect the stocks to provide roughly the same returns, all else being equal.

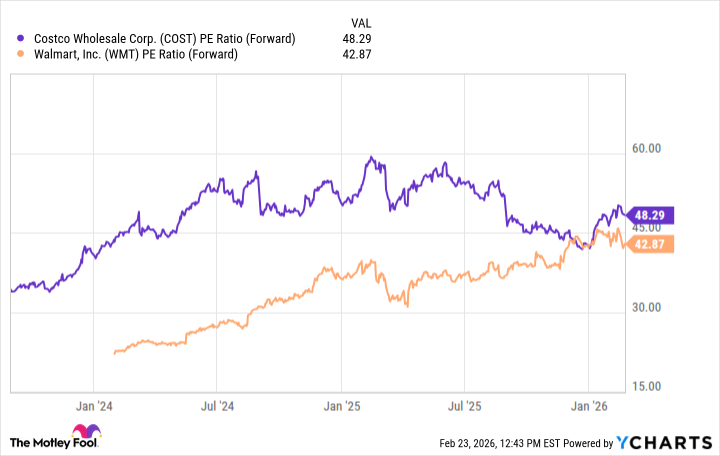

But all is not equal. From a forward earnings perspective, both Costco stock and Walmart stock are expensive, trading at more than 40 times forward earnings. But as the chart shows, Costco's valuation is meaningfully higher than Walmart's, which may limit its potential for shareholders.

COST PE Ratio (Forward) data by YCharts

Moreover, both companies pay quarterly dividends, but Walmart's dividend yield is higher, giving it an extra boost. I believe Costco stock could still be a good investment, given the strength of the business. But I think that Walmart stock could provide better returns for those buying today.