The last few weeks have been abysmal for the technology sector -- with software stocks in particular taking a beating. While the Invesco QQQ Trust, which tracks the Nasdaq-100 index, has only lost 2% over the last month, the iShares Expanded Tech-Software Sector ETF has plummeted by nearly 18%.

Throughout the ongoing "SaaSpocalypse," some quantum computer stocks have also gotten whacked. For example, shares of D-Wave Quantum (QBTS 5.55%) have fallen by 37% over the last month.

Is this sell-off an opportunity to buy the dip, or is D-Wave a falling knife in the making?

NYSE: QBTS

Key Data Points

A reckoning for AI software stocks

There are a few macro reasons for the software carnage.

First, hyperscalers Microsoft, Amazon, and Alphabet each recently announced materially higher capital expenditure budgets for 2026 than Wall Street was anticipating. As big tech doubles down on its data center infrastructure buildout to support artificial intelligence (AI), some investors are becoming skittish about the pace at which this spending is occurring versus the realized returns on those investments.

From a financial perspective, this means that many investors are not happy that the big three cloud infrastructure platforms are sacrificing short-term free-cash-flow generation for a possible AI-driven payoff at some point in the future. These dynamics have caused investors to increasingly rotate capital out of big tech for the time being.

Another pocket of the technology realm that's currently getting bruised is enterprise software. Major announcements from Anthropic, OpenAI, and vibe coding platforms have spawned the idea that incumbent data analytics and workplace productivity suites could be replaced by generative AI models.

Hence, software-as-a-service (SaaS) stocks, which generally boast premium valuations, have been losing ground as of late.

Image source: Getty Images.

Should you buy the dip in D-Wave Quantum stock?

While shares of D-Wave Quantum have also been on the decline, looking at a stock's percentage gains or losses doesn't reveal much about the underlying company's valuation profile. In order to assess whether a stock is overvalued or undervalued, one must analyze financial trends relative to that company's growth profile.

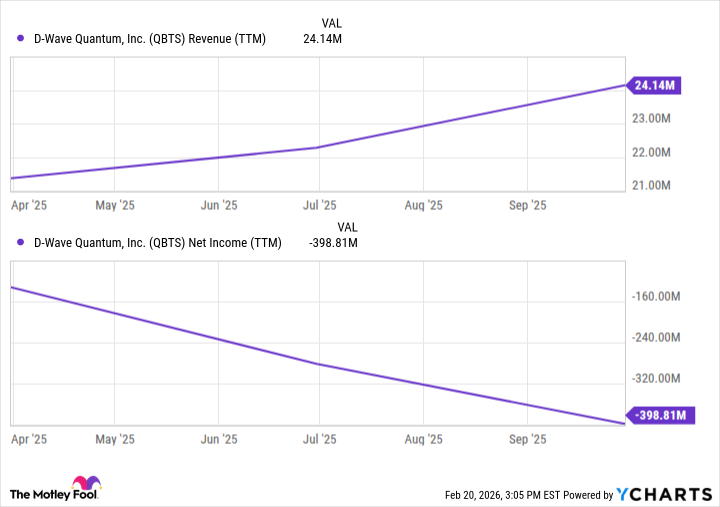

QBTS Revenue (TTM) data by YCharts.

Over the last year, D-Wave's revenue and profitability have traveled along opposite trajectories. While its sales growth is accelerating, its overall revenues remain fairly minimal. At the same time, the company's operating losses are steepening.

By most estimates, it will be years before quantum computing systems reach the level of development where they will be suitable for commercial adoption. Given that, I think D-Wave may face liquidity pressures sooner rather than later. To boot, it's not as if big tech companies are attributing their widening capex budgets to the development of quantum computers.

In short, D-Wave Quantum's outlook is extremely unpredictable. Yet even after its latest sell-off, it still trades at an unsustainably high price-to-sales (P/S) ratio of 237. That's a hefty premium. Any investor who buys the stock on this downturn is falling for a classic value trap.

To me, there isn't a compelling case for long-term investors to buy D-Wave stock at its current price. This quantum computing hopeful is best left for risk-seeking day traders.