Applied Digital (APLD 3.55%) has $16 billion in contracted lease revenue -- a pipeline that makes most AI infrastructure companies jealous and reassures investors with years of locked-in cash flow. The company is executing, delivering 100 megawatts of data center capacity on schedule at its Polaris 1 campus, even as other data center builders run into delays.

But as much as things look bright right now, the risks are real. Here's why.

NASDAQ: APLD

Key Data Points

A Russian nesting doll of counterparty risk

Applied Digital's $16 billion pipeline is not exactly as guaranteed as it may seem at first glance. The truth is that $11 billion of that $16 billion comes from a single customer that, in my opinion, is playing with financial fire.

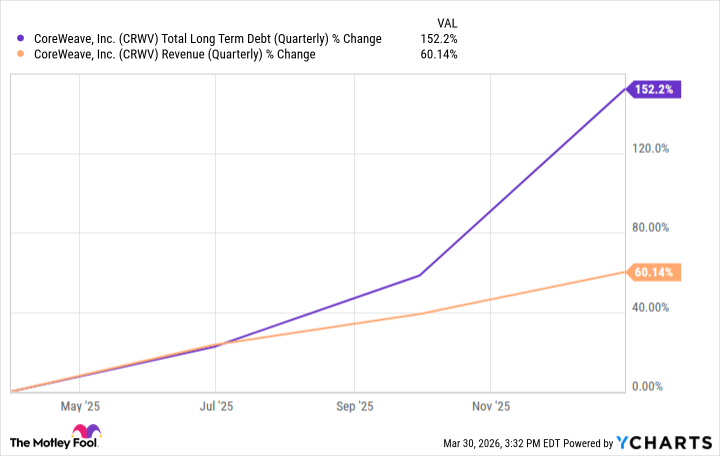

CoreWeave is a highly leveraged, unprofitable company that is attempting a tightrope walk even in the best conditions. While its revenue growth is impressive -- up nearly 170% from 2024 to 2025 -- to fuel that growth, the company is now carrying over $21 billion in total debt, up from $7.9 billion last year. Its debt is growing significantly faster than its revenue. Take a look at the chart below.

CRWV Total Long Term Debt (Quarterly) data by YCharts.

The debt isn't cheap. CoreWeave is now on the hook for about 25% of its total revenue just to pay the interest, while losing about $1.2 billion last year, up from about $860 million the year before. CoreWeave, in turn, relies heavily on another deeply unprofitable company: OpenAI.

The ChatGPT creator projects $14 billion in losses for 2026 alone, with a cumulative cash burn of $115 billion through 2029. While the company believes revenue growth will compensate, I'm not convinced.

Operating margins are moving in the wrong direction, and we have already seen signs of user growth soften, even with the company heavily subsidizing usage. Once OpenAI starts to charge rates that would actually be profitable, I think users will leave in droves.

I foresee OpenAI struggling to raise the kind of capital it has up to this point for much longer, especially if the macroeconomic picture continues to darken.

Image source: Getty Images.

So, Applied Digital depends on CoreWeave, which depends on OpenAI, which depends on the continued willingness of investors to fund AI spending at a pace never seen before. If any link in that chain breaks, the consequences flow directly downhill to Applied Digital's shareholders.

Where will Applied Digital be in five years?

Five years from now, Applied Digital could be collecting billions in annual lease revenue. But getting there requires a whole lot to go just right for each link in the chain. With the macro picture looking the way it does, I think there's a better chance things won't go according to plan. And with the sort of expensive debt Applied has taken on to finance its growth, the downside risk is substantial.

I see Applied Digital stock having failed to keep pace with the market five years from now.