If you were to look at Microsoft (MSFT 1.13%)'s share price, you might think that the business is struggling. It has fallen 21% this year, and over the past 12 months, the stock has declined by 1%. That's not the type of performance you might expect from a company that's as robust and diversified as Microsoft, particularly as it's investing in new opportunities in artificial intelligence (AI).

The tech stock needs a positive catalyst, and investors may be hopeful that when it reports its latest earnings on April 29, it could finally get one. Should you buy the stock before then?

Image source: Getty Images.

Recent earnings reports haven't been kind to the stock

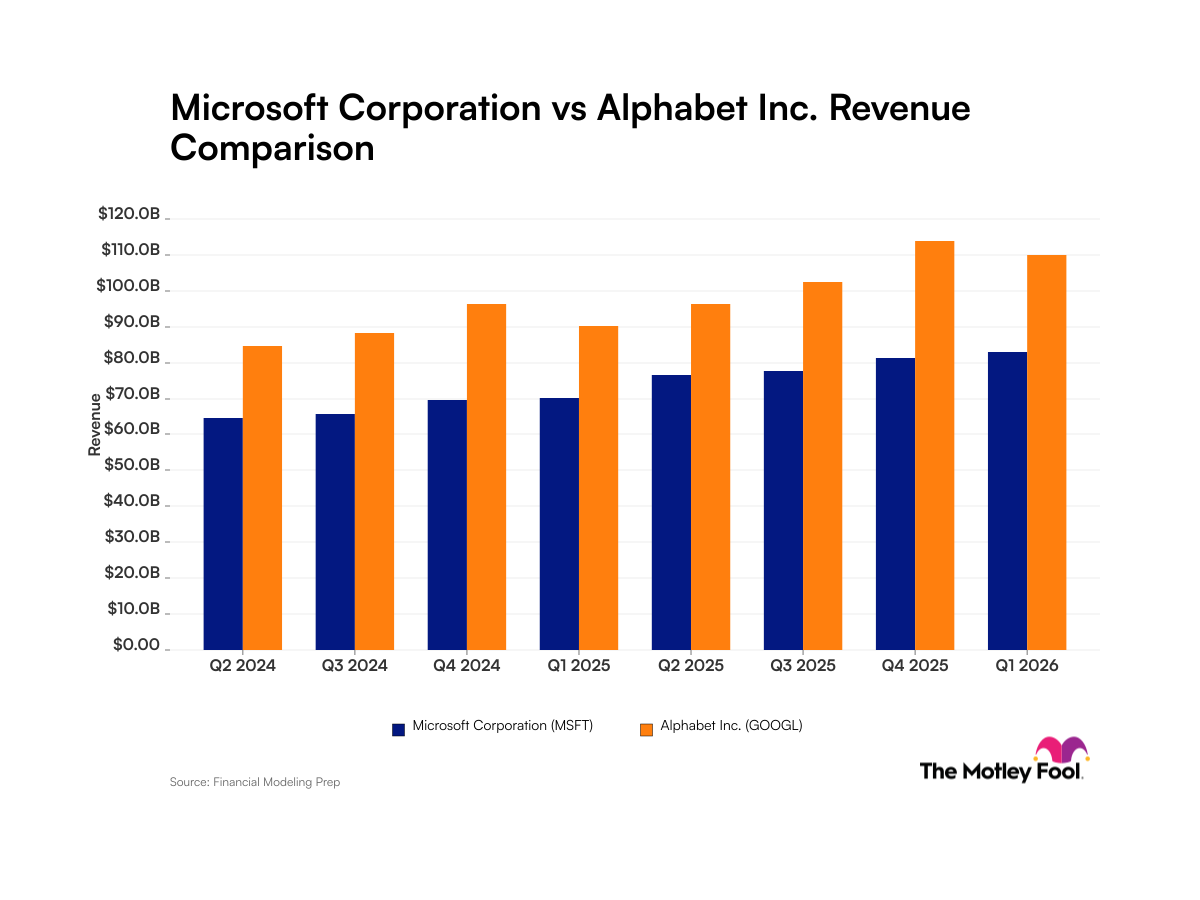

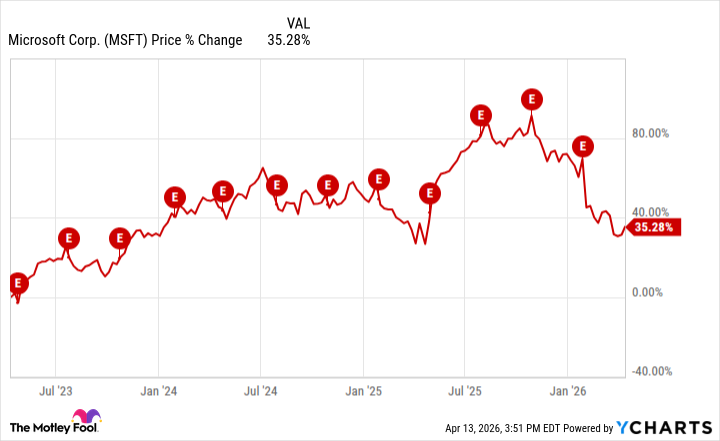

A big concern for investors recently has been that Microsoft's cloud business, Azure, has been growing at a slower pace of late. And that could be a key number that yet again dictates how the stock does after it reports earnings. Back in January, the stock fell heavily, as you'll see in the chart below, as Azure's growth rate came in at 39% -- down from 40% a quarter earlier.

The past two earnings reports have resulted in significant declines for Microsoft's stock. Back in October, it was an increase in capex spending that spooked investors, calling into question whether its AI strategy was worth the price.

At this stage, however, unless there's a troubling new development, much of the negativity around the stock may already be priced in.

NASDAQ: MSFT

Key Data Points

Microsoft's stock might be too cheap to pass up

Shares of Microsoft have dipped so low that the stock is now trading at just 23 times its trailing earnings, and 19 times forward earnings (which are based on analyst expectations). By comparison, the average S&P 500 stock trades at a trailing earnings multiple of more than 24 and an expected future profit multiple of 21. Microsoft's stock is cheaper against both metrics.

There's some good value with Microsoft's stock today, which may make it too tempting an investment to pass up. This is one of the safest tech stocks you can own. It generates margins of around 40%, and even if its growth rate in one area of its business is slowing down, I don't think that justifies it trading at a discount to the S&P 500. This is still a company that has some fantastic long-term growth prospects, and buying it ahead of earnings, regardless of what happens, may prove to be a great move for patient investors.