There are countless retail businesses, but only a few can match the scale of Walmart (WMT 0.93%) and Costco Wholesale (COST 0.63%). As of market close on May 1, they are the 11th- and 26th-largest companies in the world by market cap, respectively.

Both companies have rewarded their investors handsomely over the years and have great growth opportunities ahead. However, one stands out as the better buy right now. I believe it's Walmart, for a few key reasons. Let's take a look.

Image source: The Motley Fool.

Different approaches to retail

Both Walmart and Costco sell everything from groceries and home supplies to clothing, electronics, and more. The difference is how they manage their sales.

Walmart's focus is on selling as much as possible, as cheaply as possible, across as many categories as possible to as many people as possible. Costco's business model is more straightforward and a bit more selective: sell a specific group of products (many on a bulk basis) at razor-thin margins, and rely on membership fees from those willing to join a select group for much of the profits it generates. Costco also tends to be more intentional about what it sells compared to Walmart.

Both models work well for their respective companies -- in their latest quarters, Walmart reported $190.7 billion in revenue, and Costco $68.2 billion -- but I prefer Walmart's omnichannel approach for its sheer reach and ability to serve virtually every demographic. It has also leveraged its reach to support e-commerce and logistics, treating stores as de facto fulfillment centers.

Costco is consistently expanding its store base, but it will never come close to Walmart's scale. Meanwhile, Walmart operates its membership-only Sam's Clubs as direct competitors to Costco.

NASDAQ: WMT

Key Data Points

Business beyond traditional retail

Investing in Costco is investing in a pure-play retail stock, though its bread and butter is undoubtedly its memberships. It has 147.2 million cardholders, including 83.1 million paid memberships (up 4.8% year over year), 40.4 million of which were executive memberships. (Paid memberships include an extra card for another household member.) In its most recent quarter (ended Feb. 15), memberships provided 2% of its total revenue and 50% of its operating income.

Costco has been expanding its digital footprint and e-commerce, but it's not growing at the same speed as Walmart in those areas. Walmart is a retail company at its core, but it has been making impressive progress in other high-margin areas like digital advertising (Walmart Connect), its third-party marketplace (Walmart Marketplace), and memberships (Sam's Club and Walmart+).

It has the data and traffic that advertisers want, and the reach to make its marketplace valuable. And faster shipping speed and convenience have strengthened Walmart+'s appeal to customers who would have otherwise gone with Amazon Prime.

NASDAQ: COST

Key Data Points

How each stock acts as an income source

Both Walmart and Costco offer a dividend, though their yields don't jump off the screen. Walmart's quarterly dividend is $0.2475, with a current yield of around 0.7%. Costco's quarterly dividend is $1.47 with a yield of around 0.5%.

One major difference, though, is that Walmart is a Dividend King (a company with at least 50 years of consecutive increases). It has increased its dividend for 53 consecutive years, while Costco has done so for 22. Both dividends are secure, but you can't go wrong with Walmart's stability and consistency.

Costco's dividend, however, is growing at a much faster pace than Walmart's. Its dividend has increased by 86% over the past five years, compared with Walmart's 35% increase. Costco also offers irregular special dividends that tend to be sizeable.

Which stock looks like the better value?

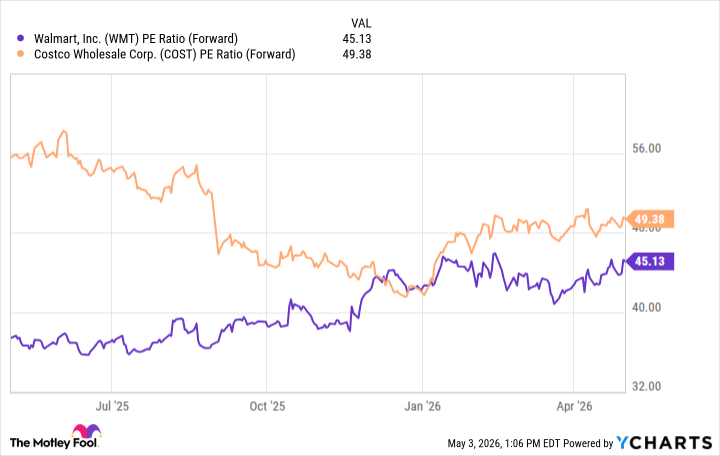

Valuation alone doesn't make one stock a better buy than another, but it should be considered. As of market close on April 29, Walmart was trading at 45.1 times its projected earnings over the next 12 months, while Costco was trading at 49.4 times:

Data by YCharts.

Neither stock is "cheap" or a "good value" by most valuation metrics. However, Walmart's stock is cheaper and has more momentum right now (up 33% in the past 12 months versus Costco's relatively flat performance). Aside from a short period at the end of last year and the beginning of this one, that has been the trend.

You aren't likely to see consistent double-digit revenue growth from either company, but I'm impressed by the growth and direction of Walmart's higher-margin non-retail businesses. Walmart's stock is the cheaper option with more long-term upside.