In its first-quarter earnings report, Palantir (PLTR +2.53%) delivered strong results. It beat Wall Street estimates for adjusted earnings per share (EPS) and revenue, which grew 85% year over year.

The company also issued second-quarter and full-year guidance above Wall Street estimates across every metric, according to Visible Alpha. Guidance for revenue, U.S. commercial revenue, adjusted income from operations, and adjusted free cash flow guidance all came in better than expected.

Image source: Getty Images.

However, as of 2 p.m. ET today, the stock traded nearly 7% lower.

At first glance, it's hard to understand how this fast-growth artificial intelligence (AI) stock could be sinking after such strong growth and a beat-and-raise quarter. Here are two issues plaguing the stock right now.

AI valuations are under pressure

As I wrote in my Palantir earnings preview yesterday, I expected a lot of focus on the U.S. commercial segment, which investors likely see as a big future growth vertical, given that Palantir has already made substantial headway in the government market.

U.S. commercial revenue came in at $595 million, below estimates calling for $605 million. As I wrote previously, for a high-growth company, even a slight miss can send the stock down in a big way, given how high expectations are for the company.

Now, interestingly, Palantir's guide for full-year U.S. commercial revenue of $3.224 billion came in above full-year estimates of $3.14 billion, so I would have thought that could have offset some of the disappointment. However, the miss may also prompt investors to doubt the full-year guidance for U.S. commercial revenue.

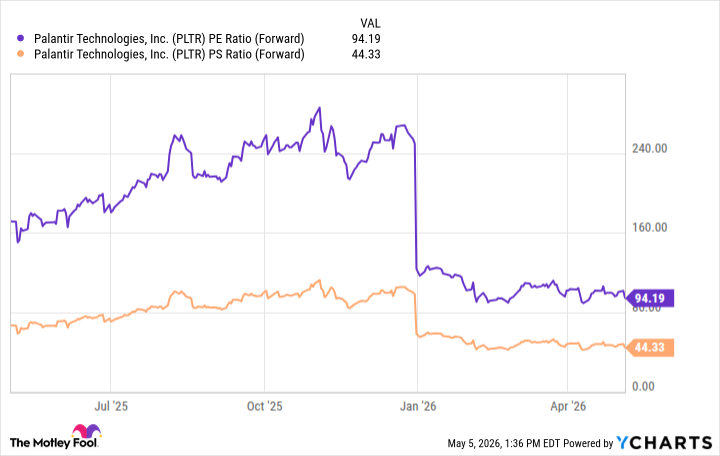

This brings me to the second major issue plaguing the company: valuation concerns.

This has been an issue across the AI and software sectors this year, as investors are beginning to doubt the AI supercycle and whether it will soon, at the very least, run into obstacles. Here are Palantir's valuation metrics after today's sell-off.

PLTR PE Ratio (Forward) data by YCharts

As you can see, they've come down a great deal, but are by no means cheap.

"We continue to view risk/reward as unfavorable. PLTR's fundamentals are exceptional, but the stock requires a heroic durability assumption to justify the current multiple," Jefferies analyst Brent Thill said in a research note following the earnings report. "We believe PLTR remains vulnerable to any moderation in AI enthusiasm or even modest headline deceleration."

Thill has an underperform rating on the stock and a $70 price target, implying significant downside from current levels. After two years of delivering incredible gains for shareholders, Palantir's stock is down 19% this year.

As Thill said, because the stock is no longer trading on fundamentals, it's likely to be more vulnerable to the ebbs and flows of the AI sector. Furthermore, competition posing a threat to Palantir could easily spook investors, who will be worried about a loss of pricing power and margin contraction.

Sentiment could flip positive later this year for any number of reasons. Interest rate cuts could materialize, and investors could get more of their questions answered about AI investments and returns, as well as greater visibility into the impact of the expected hurdles.

Palantir investors should expect volatility for the rest of the year. It's a very exciting company, but at a very high valuation. I am not interested in owning the stock at this time.