An outbreak of the hantavirus on a cruise ship recently sparked a bit of a rally in the pharmaceutical and biotech industries. While no one hopes this will become a global health crisis, if it does, those companies that develop and market effective vaccines for the hantavirus may be financially rewarded, so the argument goes. However, at this stage, it is likely not a good idea to buy into this rally. Let's consider three reasons why.

Image source: Getty Images.

1. It's not as contagious as the coronavirus

While this is an evolving situation and we may not have all the facts yet, the information we have suggests that this is unlikely to become a global health crisis on the scale of the coronavirus pandemic. Here's why. COVID-19 spreads through respiratory droplets from an infected person. The hantavirus, by contrast, is primarily transmitted by contact with the saliva, droppings, or urine of infected rodents.

There is a known variant, the Andes virus, that can spread from person to person. Even that strain has a much lower transmission rate than COVID-19, according to health officials. The hantavirus can be deadly, just like the coronavirus. But its limited person-to-person transmission could make it easier to contain and help us avoid another pandemic. That means the market for hantavirus vaccines may be very limited.

NASDAQ: MRNA

Key Data Points

2. It's hard to pick the winners

Even if the worst-case scenario happens and this turns into another pandemic, it still wouldn't be a good idea to jump into the biotech rally. Here's a key reason: It's almost impossible to predict which companies will successfully develop and market hantavirus vaccines. The experience of the COVID-19 pandemic is instructive here. Many companies tried to launch effective coronavirus vaccines. Most of them failed to develop a competitive vaccine in a timely manner and dominate the market. The list included small biotechs, such as Ocugen, and major pharmaceutical giants, like Sanofi and Merck.

The fact that Sanofi and Merck were not major winners here is especially noteworthy, given that both have strong vaccine businesses. So, one might have expected them to be among the leaders. This shows that even investing in well-established vaccine makers doesn't guarantee anything. For all we know, if the recent hantavirus outbreak becomes a pandemic, the companies that will succeed in developing effective vaccines in a timely manner may turn out to be under-the-radar corporations.

3. Picking the winners might still result in losses

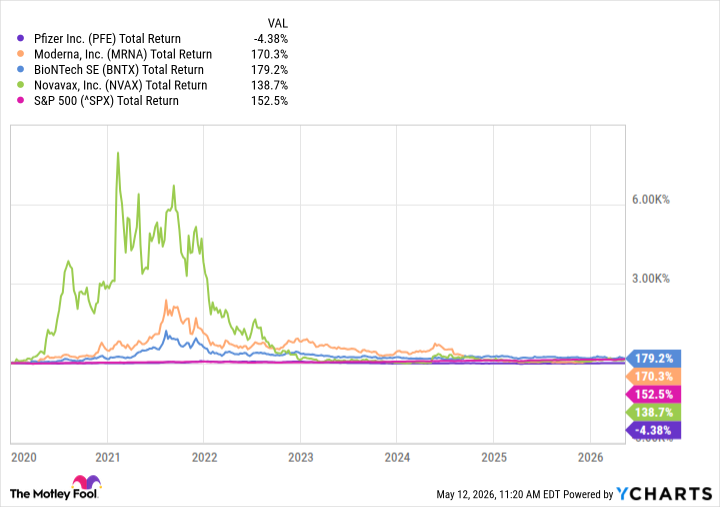

Let's go one step further: Suppose there is a pandemic, and an investor purchases shares of a company that successfully develops a vaccine for the hantavirus in a timely manner. Even under this scenario, market-beating returns aren't guaranteed. Below is the performance of four of the vaccine companies, those that dominated the COVID-19 market at its peak, since January 2020: Pfizer, Moderna, BioNTech, and Novavax.

PFE Total Return Level data by YCharts

Notably, two have underperformed the S&P 500 during this period -- Pfizer by a substantial margin. Investors focused on the long game shouldn't try to pick out which company might make the biggest splash in this hypothetical market. Investing in an ETF that tracks major indexes such as the S&P 500 or the Nasdaq is a safer way to achieve excellent returns over the long run.

NYSE: PFE

Key Data Points

Some vaccine makers are still buys

Moderna is one of those working on a hantavirus vaccine and has been doing so since before the recent outbreak on a cruise ship. While it may not be a buy for that specific reason, the company could have a bright future as it advances several of its current candidates through the pipeline. One of the most promising is mRNA-4157, an investigational personalized cancer vaccine. Moderna has plenty of other programs in the pipeline, and its mRNA platform, which enables it to develop vaccines faster than companies using traditional methods, is also a major strength.

Pfizer is another vaccine maker worth considering right now. The stock looks attractive on the dip, considering it has significantly replenished its pipeline and has a long list of pivotal trials it started over the past year or will kick off throughout 2026. Pfizer's shares could recover as its pipeline progresses through the end of the decade, making it a stock worth serious consideration.