Micron (MU +0.90%) has recently ripped off the type of rally that few stocks will ever replicate. Since dipping to a three-month low around April 1, the stock has gained a jaw-dropping 116% in just a month and a half. After a quick return like that, investors are likely wondering if it's worth hanging around for more, if they should take their quick double and run to the bank, or if they should add to their Micron positions.

Image source: Getty Images.

Micron's growth is astounding

Micron makes memory chips, which are an integral part of every computing system, including the massive data centers powering artificial intelligence (AI). The demand for memory is easily at an all-time high, and because it takes several years to build new chip foundries, it will be awhile before supply can catch up with demand. As a result, memory chip prices are soaring. Micron told investors it would only be able to meet half to two-thirds of the market's demand for its wares over the medium term. That's a major supply constraint, and it's compounded by the fact that Micron believes the market opportunity for high-bandwidth memory (HBM), the type used in data centers, will increase from $35 billion in 2025 to $100 billion by 2028.

NASDAQ: MU

Key Data Points

That will allow the companies that make memory chips to keep their prices elevated for some time, so we can expect Micron's revenue to soar. Wall Street analysts are bullish on Micron's prospects, estimating 192% revenue growth this year and 56% growth next year. For 2027, they project it will have about $171 billion in revenue. For reference, over the past 12 months, chip foundry Taiwan Semiconductor Manufacturing (TSM +5.29%) generated $133 billion in revenue, and it's a $2 trillion company.

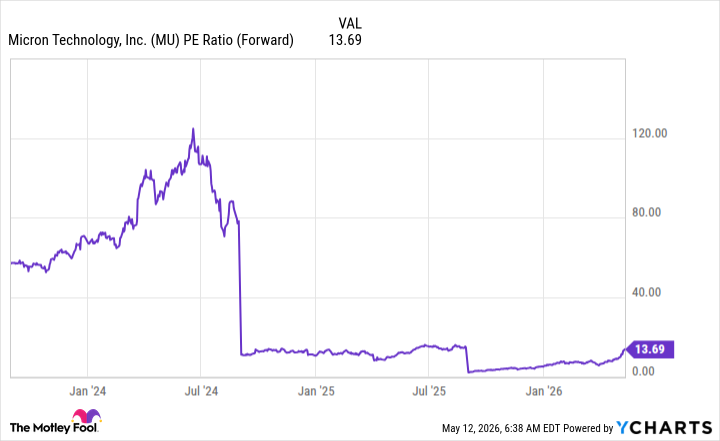

However, the memory chip market is far more cyclical than the logic chip market that Taiwan Semiconductor operates in. And Micron now trades for just 13.7 times forward earnings, while TSMC trades at a forward multiple of more than 25.

MU PE Ratio (Forward) data by YCharts

If the memory shortage lasts for several more years and Micron can continue increasing its production while it persists, it could be an incredible investment to own from here, even in the wake of its rally so far this year. However, if the shortage eases over the next year, the stock could be a flop. Investors will need to keep a close eye on this one, but if the company's growth rates keep up due to high memory demand, Micron could just be getting started.