Poet Technologies (POET +4.34%) has emerged as one of the most volatile artificial intelligence (AI) stocks so far in 2026. The reason is simple: Growth investors are flocking to anything remotely related to AI infrastructure, and with "photonics" becoming one of the latest buzzwords in the sector, Poet has landed on the radar of speculative retail traders.

The question smart investors are asking is whether Poet stock is a sound buy at "just" $14 per share. A closer look at the company's valuation metrics reveals a clear answer.

NASDAQ: POET

Key Data Points

Taking a look at Poet stock's price movement

Poet entered 2026 with the appearance of strong tailwinds. Early gains were fueled by hefty enthusiasm around the company's manufacturing scale-up, alongside production orders that signaled a shift from R&D to commercial revenue traction.

Sentiment began to soar as the company's positioning in optical interconnects for hyperscale data centers gained momentum. However, a sharp reversal followed after news of a major order from Celestial AI was canceled. Celestial AI is a subsidiary of Marvell Technology, which cited confidentiality breaches as the basis for canceling the deal with Poet.

Like most momentum stocks, shares of Poet swiftly recovered -- exploding from the $7 to $9 range to the mid-teens on heavy volume as renewed buzz around photonics adoption and production readiness reignited interest.

Image source: Getty Images.

$14 might look cheap on the surface, but Poet stock is undoubtedly pricey

At first glance, a $14 stock price may appear inexpensive, but smart investors understand that share price alone reveals almost nothing about a company's true valuation.

Poet's trailing-12-month revenue is roughly $1.1 million -- hardly explosive, given the hundreds of billions of dollars big tech is pouring into AI data center build-outs. Meanwhile, the company's market capitalization hovers near $2 billion!

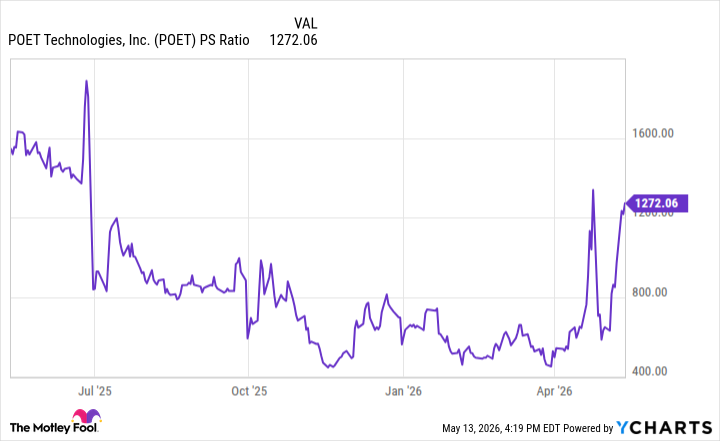

POET PS Ratio data by YCharts.

This translates to a price-to-sales (P/S) ratio above 1,200x -- an extraordinarily high multiple pricing Poet stock to perfection. Such a valuation multiple is unsustainable without rapid revenue acceleration and a clear path to sustained profitability. While high P/S multiples can persist under speculative growth assumptions, they often collapse once execution falters or stock dilution pressures mount due to liquidity concerns.

Whether the stock trades at $14 or $1,000 is irrelevant. What matters most is a company's enterprise value relative to actual sales growth, cash flow generation, and earnings trajectories. At current levels, investors are paying a premium that assumes Poet captures a meaningful slice of AI infrastructure budgets amid a budding photonics opportunity for years to come.

Investors should pass on Poet's hype

Traditional valuation methodologies paint a clear picture of overvaluation at $14. With negligible sales, no earnings, and a sky-high valuation, Poet does not meet the standard criteria for a no-brainer buy.

The risk-reward profile around Poet simply is not compelling: Substantial execution hurdles remain in scaling manufacturing and securing sustained hyperscaler orders. Any shortfall in revenue ramp-up will certainly trigger sharp selling pressure as sentiment reverses.

At today's price, Poet's upside is already baked in. Disciplined investors should demand either a materially lower entry or a concrete, measurable revenue inflection before taking a position. For now, Poet's stock priced at $14 remains a highly speculative bet rooted in hype rather than a value opportunity grounded in strong fundamentals.