Berkshire Hathaway (BRKA +2.16%) (BRKB +1.69%) is entering a new era. The conglomerate that Warren Buffett built over decades has a new CEO, Greg Abel, who took over from the Oracle of Omaha on Jan. 1. In his first full quarter as the head of Berkshire Hathaway, Abel oversaw some notable moves. For instance, the company exited its positions in several stocks, including Amazon (AMZN +1.07%).

Some may find that decision puzzling. Amazon is a leader in cloud computing, artificial intelligence (AI), and e-commerce, and arguably possesses a wide moat from several sources. And with the AI industry still in full swing, Amazon may be a great pick to capitalize on it. However, Abel and his team haven't given up on AI. There are at least two stocks in Berkshire Hathaway's portfolio that could be major winners from the AI revolution. Read on to find out more.

Image source: The Motley Fool.

1. Alphabet

Berkshire Hathaway first bought Alphabet's (GOOGL +0.16%) (GOOG -0.13%) Class A shares (which grant voting rights) in the third quarter of 2025. In the first quarter, the company increased its stake in this position by 204%, while also adding Alphabet's Class C shares (which come with no voting rights). The conglomerate is clearly excited about the future of Alphabet, and it is not surprising. Alphabet has many of the qualities of Buffett-style investing. For one, it is a fairly straightforward, easy-to-understand business.

Alphabet is the leading search engine company in the world through Google and also owns the largest video-sharing platform on the web, YouTube. The company generates significant revenue from advertising and various subscriptions. Then there is Alphabet's current fastest-growing segment, Google Cloud, which offers a range of cloud computing services, primarily via an attractive, flexible pay-as-you-go model. Alphabet has other businesses, but these make up its core.

NASDAQ: GOOGL

Key Data Points

Buffett also insists on investing in companies with durable competitive advantages. Alphabet fits the bill. The company's brand name alone, which has become a verb used in everyday language, makes its search engine empire nearly impenetrable. The company also benefits from network effects and switching costs. Then, there is the fact that Alphabet has excellent long-term prospects.

The company's AI business is helping power Google Cloud's amazing growth, and it plans to invest even more to capture the lucrative opportunities ahead. Alphabet's $460 billion cloud backlog as of the end of the first quarter, which almost doubled quarter-over-quarter, highlights the attractive growth runway at its disposal. And given the company's innovative culture and smaller -- but promising -- growth opportunities, like self-driving vehicles, the future looks bright. Investors should follow Abel's lead here and double down on Alphabet.

2. Apple

Apple (AAPL -2.10%) has been the largest holding in Berkshire Hathaway's portfolio for a while, and, so far, it has remained so under Abel's (short) tenure. The fact that Buffett once called Apple "the best business in the world" is all the confirmation we need that it fits the Oracle of Omaha's criteria. The business is fairly easy to understand: Apple makes money by selling hardware products, including smartphones, laptops, tablets, etc.

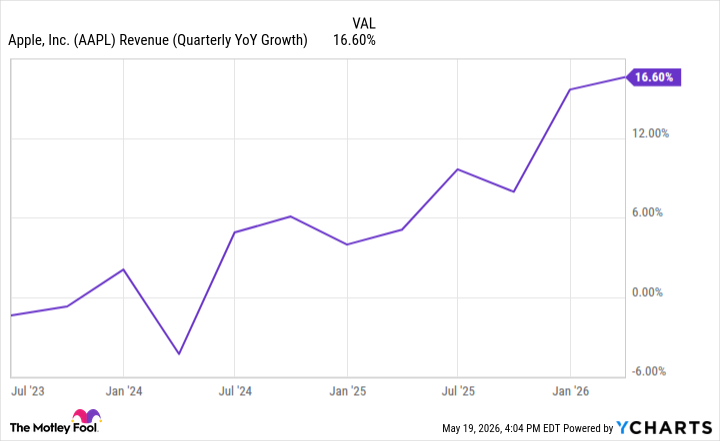

Its iPhone segment is its most important and functions almost like a subscription, as users tend to renew their phones every few years. Apple has improved its devices thanks to AI features. And over the past few quarters, sales growth has accelerated, reaching levels not seen in three years.

AAPL Revenue (Quarterly YoY Growth) data by YCharts

This shows that the iPhone can still drive solid sales growth, especially as Apple continues to improve it.

NASDAQ: AAPL

Key Data Points

Apple also has a high-margin services segment with over a billion paid subscriptions. This unit is important to Apple's future. As the company's installed base grows, it will expand subscription revenue, helping boost margins and profits. Let's not forget about Apple's competitive moat, which stems from its brand name. The company's brand routinely ranks as one of the most valuable in the world and grants it significant pricing power in an otherwise competitive market.

Apple also benefits from switching costs, since it can be difficult to transfer data from the company's ecosystem to one of its competitors'. Apple faces threats, including tariffs and regulatory risks, but the stock is still well positioned to outperform over the long run. It's no wonder that Abel remains bullish on the company.