Although Warren Buffett may be retired as CEO of Berkshire Hathaway (BRKA 0.22%) (BRKB 0.53%), he's still chairman of the board. That means his influence still reaches deeply within the company he built, and there is evidence of that in Berkshire's first-quarter investment activities.

One of Buffett's last moves as CEO was to initiate a position in Alphabet (GOOG +4.94%) (GOOGL +4.79%), a company he had been a longtime fan of, but that he didn't invest in until Q3 2025. While Berkshire didn't do anything with the stock in Q4, it more than tripled its position during Q1. That's a major vote of confidence and makes Alphabet one of Berkshire's largest holdings.

But this information is old. Is the stock still a buy today?

Image source: Getty Images.

Berkshire got a much better deal than you can get today

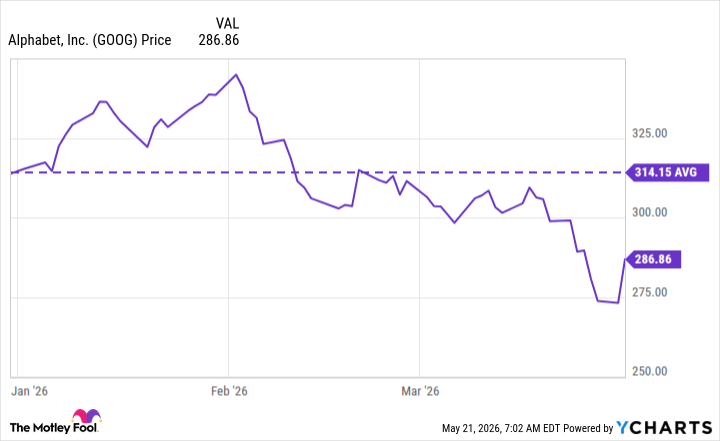

Although investors learned about Berkshire's Q1 buys on May 15, the information is as of March 31. That delay can be a big deal, as Alphabet's stock has risen significantly since March 31. During Q1, the average price for Alphabet's stock was $314, although it dipped a bit as the quarter ended.

Now, it trades for nearly $400 per share due to a major AI rally that kicked off in April. So, Berkshire got a better deal than you can get today, but is the stock still worth buying?

In Q1, Alphabet's revenue growth accelerated to 22% year over year, thanks to the strength of its Google Search and Google Cloud business units. In particular, Google Cloud revenue soared 63% year over year. Investors can expect similar growth for years to come, as Alphabet is making major investments in cloud infrastructure to support massive AI workloads coming online. It's also making a nice profit from its own AI chip that it's now selling to external clients.

NASDAQ: GOOGL

Key Data Points

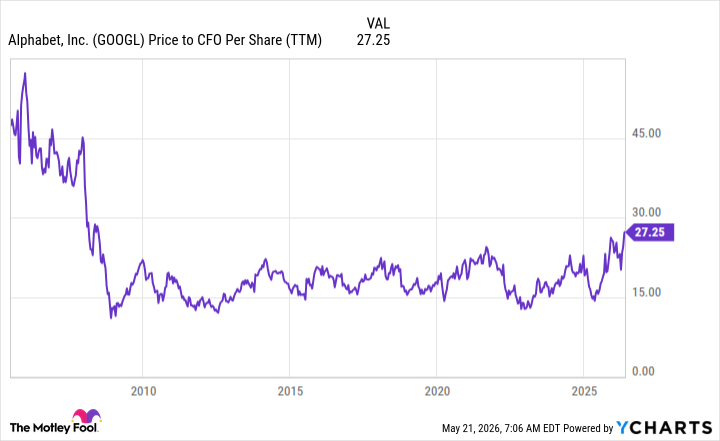

That bodes well for Alphabet's future, but it's now priced at a premium. I think the best way to value Alphabet's stock is via cash from operations. This measures how much cash the business is generating, and ignores the major capital investments Alphabet is making to drive growth. From this standpoint, Alphabet hasn't been this expensive since it was a fresh company on the public markets.

GOOGL Price to CFO Per Share (TTM) data by YCharts

That concerns me a bit, but 27 times operating cash flow isn't an out-of-line valuation for a successful big tech company; it just happens to be expensive for Alphabet. As a result, I'm a bit more cautious on Alphabet's stock. While I'm not selling, I am a bit hesitant to add until I see further proof of increased revenue growth from AI.