The cannabis industry has been a disappointment. Although Wall Street had high hopes for marijuana stocks toward the end of the last decade, as legal and regulatory progress in the market made pot growers more attractive, almost every one of them has significantly underperformed broader equities in recent years. Tilray Brands (TLRY +8.10%), a leader in the industry, has been no exception: The company's shares have declined by more than 90% over the past five years. However, some investors hope that recent developments in the U.S. cannabis market could be a turning point for Tilray. Is now a good time to bet on the stock?

Image source: The Motley Fool.

A gift from the government

Following an executive order signed by President Trump, products approved by the U.S. Food and Drug Administration that contain marijuana -- as well as medical cannabis products that are legal in certain states -- have been moved from Schedule I to Schedule III. Here's what that means. Under federal law, Schedule I substances are deemed the most addictive while having no recognized medical benefits. Products in the Schedule III category are considered less prone to abuse. This change will make it easier to research potential health-related benefits of marijuana, something that could move the needle for pot growers that operate in the U.S. Tilray is ready to take on this opportunity through its footprints in the U.S. market, where it offers a variety of CBD and hemp-based products, as well as a craft-brewing business.

We have seen this movie before

It's worth noting that the recent rescheduling decision does not include recreational marijuana. However, there is a hearing on the books for next month to discuss whether other forms of cannabis should also be rescheduled. Even assuming the best-case scenario for Tilray, though, it is less than clear that this will be the major turning point many investors hope for. Rescheduling cannabis wouldn't make the substance legal at the federal level. So, significant barriers would remain.

NASDAQ: TLRY

Key Data Points

For instance, it would still be illegal to ship the substance across state lines. This restriction forces many cannabis companies to own and operate facilities to cultivate and process cannabis -- as well as to make various products derived from the substance -- in every state where they do business, instead of relying on one or a few such sites spread out in several states that ship products to every other one. This is an incredibly inefficient way to do business that pot growers are forced into, leading to significantly higher operating expenses than they would otherwise incur.

That's one of the reasons most cannabis companies in the U.S. are unprofitable. True, rescheduling will help medical cannabis companies in the country by allowing them to deduct normal business expenses (companies selling Schedule I or Schedule II drugs aren't allowed to do that), thereby lowering operating costs. But there are other problems. Just like it dealt with significant competition in Canada once recreational uses of cannabis were legalized in the country in 2018, Tilray might encounter the same issue here.

Even with the company's large portfolio of products and brands, it isn't clear that it has developed a competitive advantage that would allow it to emerge as one of the winners. And that would be the case even if federal legalization happens in the U.S. That might certainly open massive opportunities, but it would also attract far larger corporations with the financial means, brand recognition, and expertise in navigating industries with tough regulatory landscapes.

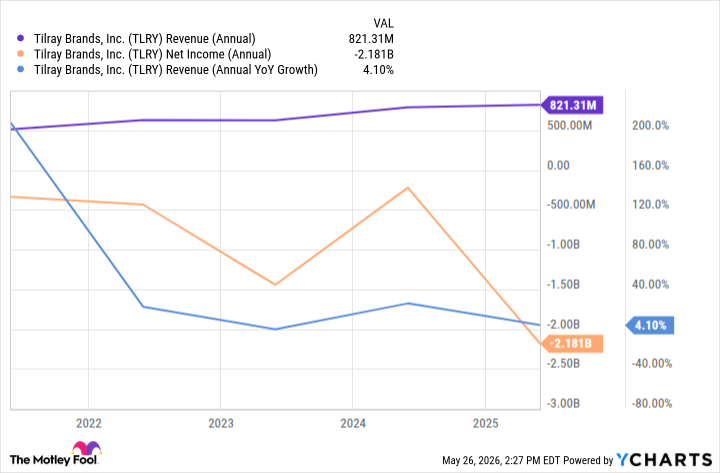

In fairness to Tilray, it has significantly diversified its lineup in recent years. It is now the fourth-largest craft brewer in the U.S. thanks to a series of acquisitions. That said, the company continues to generate inconsistent revenue growth. It also remains unprofitable.

TLRY Revenue (Annual) data by YCharts

Given Tilray's track record, its poor financial results, and the industry's uncertainty, it's hard to make a solid case that the company's long-term outlook is attractive. Investors shouldn't bother with this stock, even though it is trading just slightly above penny-stock territory.