Micron Technology's (MU +0.90%) meteoric rise over the last year marks more than just a generic bullish upgrade in the semiconductor industry. Micron's ascent is a symbolic rebuke to a long-held belief that memory chip demand is trapped in boom-and-bust cycles.

Let's dive into the structural changes shifting the memory market and understand how Micron is becoming a key enabler of the artificial intelligence (AI) infrastructure revolution.

Image source: The Motley Fool.

Why is the memory market volatile?

For years, the memory semiconductor industry has been vulnerable to sharp cyclical swings. Demand for DRAM and NAND flash storage is traditionally tied to patterns around consumer electronics upgrades.

During boom periods, chipmakers ramp up production to capture market share across PCs, smartphones, and data centers. Unfortunately, this strategy often leads to oversupply -- resulting in steep price declines that can erode profit margins for several quarters or even years.

Lead times for new fabrication plants further exacerbate mismatches between supply and demand, thereby creating a self-reinforcing loop of volatile business performance. As a result, investors historically applied low valuation multiples to memory stocks to reflect the unpredictable nature of these businesses.

NASDAQ: MU

Key Data Points

AI is turning memory into a structural narrative

Unlike past cycles plagued by lumpy discretionary spending, AI infrastructure requires continuous high-bandwidth memory (HBM) supply to power clusters of graphics processing units (GPUs) in massive training and inference workloads.

Major hyperscalers such as Amazon, Microsoft, Alphabet, and Meta Platforms are accelerating data center build-outs. Micron's specialties across DRAM and HBM have become critical enablers of next-generation AI factories as models and applications grow more complex.

Big tech faces competitive pressures to deploy and monetize new AI capabilities faster than its rivals. As such, hyperscalers are prioritizing securing memory supply over favorable price negotiations. This inherently creates a demand floor above the mechanics of prior boom-bust dynamics.

Micron has earnings growth stability through new contract structures

To meet hyperscale demand, Micron is using long-term agreements that provide clarity for both parties. Essentially, these contracts are designed to lock in committed chip volumes and partial price protections.

For customers, the trade-off is sacrificing some flexibility on price to ensure access to the memory needed to keep AI roadmaps on track. For Micron, the leverage is more lucrative. Long-term agreements provide predictable revenue streams, which help reduce the risk of inventory write-downs. This structure allows more deliberate capital expenditure (capex) planning across the company's fabs. In financial terms, this visibility translates into margin expansion and earnings durability.

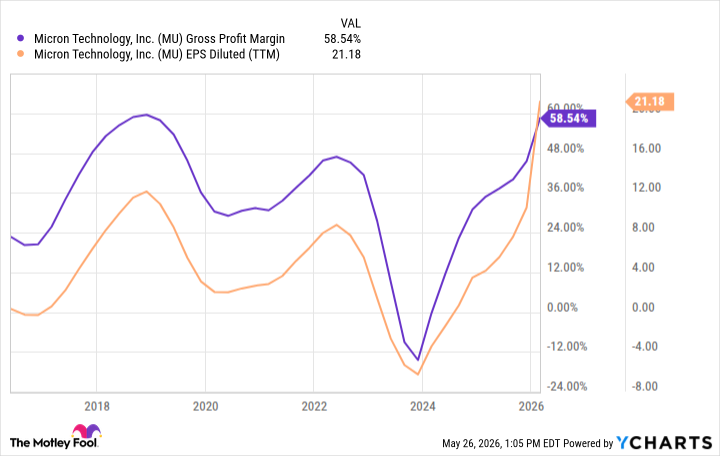

Data by YCharts.

As these deals compound, Micron's financial results should increasingly reflect compounding earnings supported by the multiyear build-out of AI infrastructure as opposed to fleeting cyclical tailwinds.

It's these dynamics that inspired UBS analyst Timothy Arcuri to lift his price target from $535 to $1,625 -- signaling that Micron's run is far from peaking. In this AI-driven memory paradigm, Micron is not enjoying a typical cycle wave. Rather, the company is emerging as a core pillar supporting the next major boom in the AI infrastructure era.