Sandisk (SNDK 1.98%) has arguably been the stock of the year so far in 2026, soaring by over 600% in just five months. Normally, when I see a stock rising that much, that fast, I assume it's a meme stock or that the company in question is caught up in a bubble. However, I don't think that's the case here.

There are multiple reasons why Sandisk's stock has been a great performer so far, and there are three in particular that give me reason to think it can still go higher from here.

Image source: Getty Images.

Sandisk doesn't have an unreasonable valuation

When a stock rises more than 600% in five months, it's normally a safe bet that it has acquired a premium price tag along the way. But that doesn't appear to be the case with Sandisk.

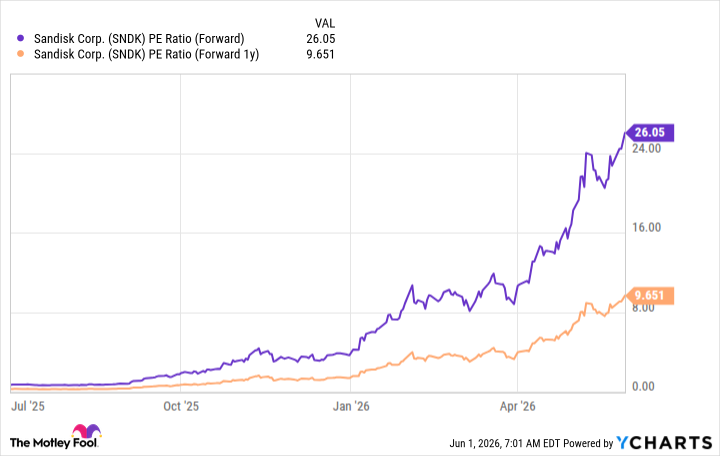

SNDK PE Ratio (Forward) data by YCharts.

It trades for 26 times its expected earnings for its fiscal 2026, which will end this month, so a better metric to use is the P/E for fiscal 2027 earnings, as that looks toward future growth. It's not often you can scoop up a fast-growing stock for less than 10 times earnings, but that's exactly the deal that Sandisk stock is giving investors.

Now, there are valid arguments against putting a high premium on a cyclical business like Sandisk. Still, if the current memory shortage lasts for several years, Sandisk could easily trade at a normal tech company valuation of around 25 times forward earnings (like it does now). Despite the stock's rapid rise, it isn't expensive, and a lot of that can be attributed to its growth.

Sandisk's growth is impressive

Sandisk makes NAND memory, which is primarily utilized in solid-state drives (SSDs). SSDs are heavily used in data centers, where they provide long-term storage for generative artificial intelligence (AI) interactions, as well as other data sets that need to be highly accessible. As demand grows and supply remains limited, prices will soar, which will cause Sandisk's revenue and earnings to grow at a rapid pace.

NASDAQ: SNDK

Key Data Points

During its most recently reported quarter, Sandisk's revenue rose 251% year over year. While it lost $0.30 per share overall last year, in fiscal 2026 Q3, its adjusted earnings per share (EPS) rose to $23.41. In its fiscal 2027, Wall Street analysts project Sandisk's adjusted EPS will come in at $175.62.

That would be monster growth, but what can investors expect after that?

The data center build-out is just getting started

Most investors can see that Sandisk has a great year ahead of it, but this could all come crashing down if the data center build-out doesn't continue. However, some well-connected companies believe that AI infrastructure spending will remain elevated through at least 2030. The most prominent is Nvidia, which provides computing units for data centers. It projects that AI hyperscaler data center capital expenditures will rise to $1 trillion in 2027, up from about $650 billion in 2026. However, that's only the beginning.

By 2030, Nvidia estimates there will be $3 trillion to $4 trillion in spending on data centers worldwide. If that forecast pans out, both Nvidia and Sandisk will have years of strong returns ahead due to soaring demand. Both companies likely have fairly good information pertaining to the level of demand they'll face over the next several years, so giving some credence to these projections may be smart.

Given the important role Sandisk is playing in the AI data center build-out, it will likely see strong returns over the next few years, making it a solid AI stock to consider buying now.