Marvell Technology (MRVL +3.98%) has been reaping the benefits of the artificial intelligence (AI) chip boom, as evident from the terrific growth in the company's revenue and earnings in recent quarters.

Not surprisingly, this semiconductor stock has shot up by a stunning 265% over the past year, outperforming the tech-focused Nasdaq Composite index's 42% jump by a big margin. Investors, however, may be wondering whether it makes sense to buy Marvell stock following its red-hot rally in anticipation of more upside.

That's why I will take a closer look at Marvell's latest quarterly report and check if this stock can soar higher.

Image source: The Motley Fool.

Marvell Technology's accelerating growth rate is great news for investors

Marvell released its fiscal 2027 first-quarter results (for the three months ended May 2) on May 27. Its revenue increased 28% year over year to $2.42 billion, while non-GAAP earnings increased by 29% to $0.80 per share.

NASDAQ: MRVL

Key Data Points

The guidance was the icing on the cake. Marvell is anticipating a stronger year-over-year growth of 35% in revenue in fiscal Q2. Even better, management notes that strong demand for its AI chips will accelerate revenue growth throughout the year. Moreover, Marvell has raised its fiscal 2027 revenue guidance by $500 million to $11.5 billion.

The company expects stronger revenue growth of 45% in fiscal 2028 to $16.5 billion. Marvell management noted on the latest earnings call that it is benefiting from strong demand for its data center networking solutions and custom AI processors. Specifically, Marvell estimates that its data center interconnect (DCI) business will double by fiscal 2028 compared to fiscal 2026 levels.

What's more, its custom AI chip revenue is anticipated to grow by 20% this fiscal year, followed by a jump of more than 100% in fiscal 2028. Marvell management noted that it has been securing more design wins for its data center products, while existing customers continue to award it more business. All this explains why analysts have become bullish about Marvell's prospects, and that's likely to pave the way for more upside in this AI stock.

The stock could easily jump higher

Marvell's valuation may prompt investors to question whether they should buy the stock right now. After all, it is trading at 70 times trailing earnings. However, the forward earnings multiple of 51 suggests that Marvell is on track to clock healthy bottom-line growth.

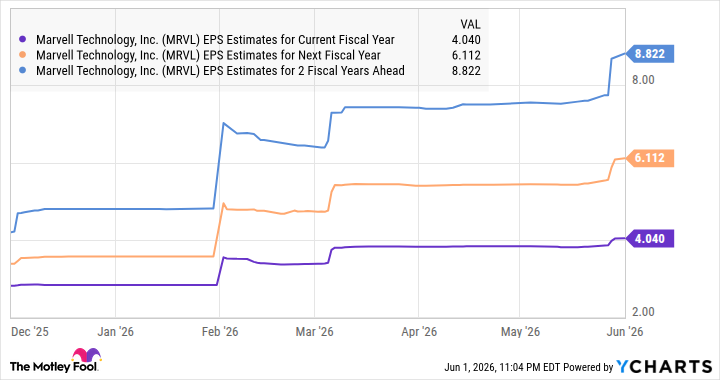

Consensus estimates indicate that Marvell's earnings could increase by 42% this year to $4.04 per share. Looking ahead, analysts are expecting its earnings to more than double by fiscal 2029.

Data by YCharts

Assuming Marvell's earnings indeed reach $8.82 per share in fiscal 2029 and it trades at 42 times earnings at that time, in line with the Nasdaq Composite's earnings multiple, its stock price could reach $370. That's a potential upside of 68% from current levels. However, Marvell's actual gains could be bigger than that, as the acceleration in its earnings growth should help it maintain a premium valuation.