When Apple reached a $1 trillion market cap, it was a momentous occasion. Almost 10 years later, it seems a new stock is reaching a $1 trillion valuation every week amid the artificial intelligence (AI) bull market. The latest is Micron Technology (MU -6.99%), a memory chip maker benefiting from increased on-device and cloud storage needs for AI software.

The question remains whether Micron has permanently elevated itself into the ranks of the "Magnificent Seven" stocks like Nvidia, or whether Micron is enjoying a temporary boost to the memory chip market before it falls back to Earth.

NASDAQ: MU

Key Data Points

Soaring profits due to insatiable demand

Nvidia has soared to become the largest company by market cap thanks to its innovation in AI chips. Training and running AI models like your ChatGPT chatbot require robust processing capabilities compared to legacy software programs, which is why Nvidia now generates $82 billion in quarterly revenue.

Now, it is increasingly the job of memory chips to help operate these AI software programs. Whether on your computing device (like an iPhone) or in the cloud, demand for storage is growing like an invasive species, creating a bottleneck for AI use worldwide. More memory chips will be needed to match supply and demand.

This may be a problem for the AI software providers, but it is a gold mine for Micron at the moment. A shortage of memory chip production has led to soaring prices, which in turn have boosted Micron's revenue and earnings. Revenue last quarter grew to $24 billion, up from $8 billion a year ago, and operating income was $16 billion. This quarter, management is guiding for $33.5 billion in revenue.

With analysts believing the shortage of memory chips won't end for years -- especially if both Anthropic and OpenAI raise tens of billions in capital for their initial public offerings (IPOs) -- estimates call for Micron to post $100 billion in net income in both 2027 and 2028.

Compared to these levels of net income, a market capitalization of $1 trillion does not look unreasonable for Micron.

Image source: Getty Images.

Revenue and earnings volatility

The big question is whether these earnings are durable. Some AI bulls claim that because of this new paradigm, memory chip demand will grow in perpetuity. You can understand the logic of this argument if AI is going to take over digital consumption worldwide, as it will need a gargantuan number of memory chips to operate smoothly.

Where the argument does not hold up is the historical cyclicality of the memory chip and semiconductor sector in general. Micron and the rest of the industry have experienced historical volatility in revenue due to undersupply or oversupply of memory chips. The bears would argue that, while AI is driving demand, this is just an overpriced memory chip cycle that will eventually turn the other way on investors.

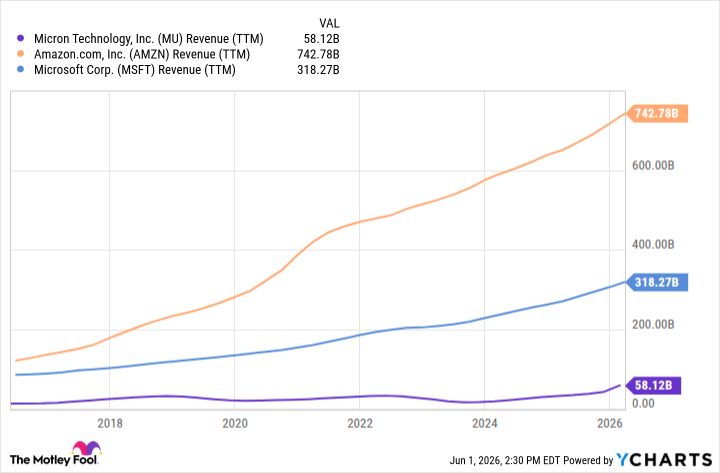

MU Revenue (TTM) data by YCharts

Why Micron is not a Magnificent Seven stock

Micron may generate the same level of net income as a Magnificent Seven stock like Amazon in 2027 and 2028 (Amazon's net income was $91 billion over the last 12 months). This does not put the business on the same competitive plane as the technology giants.

Outside of typical cycle worries, Micron could be seen as a commodity provider of computing storage alongside the rest of the memory chip industry. Large technology players like Amazon have diverse business models and competitive advantages that keep upstarts from accessing their profit pools. This is part of the reason why these stocks are valued so highly. Even fellow chipmaker Nvidia has a software development edge and product ecosystem that keeps customers from switching.

Micron does not have any of these competitive advantages, which is why I would not classify it as a Magnificent Seven stock even if it temporarily has a market value of $1 trillion and $100 billion in net income.