Cloud storage and big data have been touted as the next technological boom, the next big thing for businesses. Dell does a good job explaining why in two simple sentences:

Cloud computing not only improves business processes and operational efficiency -- it reinvents the role of IT. And when aligned with organizational strategy, it can give you a competitive edge.

With that in mind, it is easy to see why big data and cloud storage is expected to grow exponentially over the next decade. However, due to exponential growth expectations, more cloud storage and big data businesses will continue popping up. This will lead to increased competition, which will likely lead to increased spending on marketing programs and lower price points for products and services, ultimately causing profit margins to decrease. . Therefore, in general, stock prices will not grow in tandem with the growth of the industry.

Something is wrong when the biggest players are disappointing

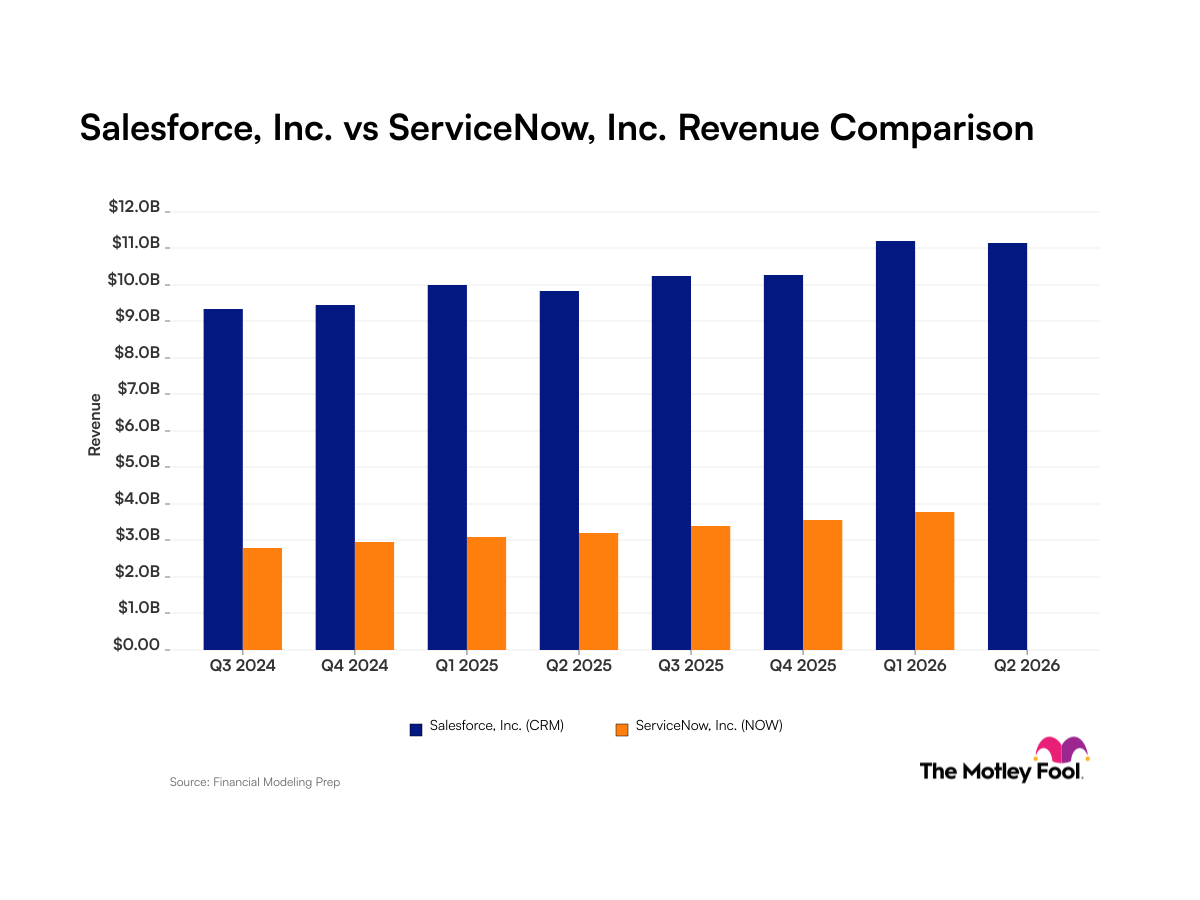

Two of the biggest companies in this industry are EMC (EMC +0.00%) and Salesforce.com (CRM 0.28%). Saleforce.com has been one of the best-performing cloud stocks, but the fundamentals behind this movement are close to nonexistent. Salesforce.com has not turned a profit on an annual basis in three years, yet over that same period, the share price has climbed 90%.

On the other hand, EMC's average net profit margin over that period was 12.4% and the share price slumped almost 7%. Similarly, NetApp (NTAP +6.08%) and F5 Networks (FFIV +2.67%) have consistently turned a profit and substantially under-performed the broader index.

The problem with Salesforce.com

Even though Salesforce.com's share price has performed well for investors in the past, there are two red flags. The first is Salesforce.com's accounts receivable. It is a red flag when a company's accounts receivable figure is greater than one-quarter of revenue. Currently, according to the March 5, 2014 10K, Salesforce.com has $1.36 billion in accounts receivable and $1.145 billion in revenue for the most recent quarter. This could be due to two reasons: Salesforce.com is too liberal with its billing, leading to a higher probabaility of getting burned, or there are some accounting games being played that allow Salesforce.com to legally add more accounts to the balance sheet.

The second red flag is the 38% increase in Salesforce.com's operating expenses in 2013. This trend will continue in 2014, and most likely into 2015 as well, according to Salesforce.com's most recent earnings press release. The company expects an EPS loss of $0.51-$0.53, which indicates that Salesforce.com is putting forth a concerted marketing effort and revenue is not keeping pace with expenses. If this trend does not reverse, investors will have no choice but to dump the stock.

Competition is great for customers, not so great for investors

The competition within the cloud computing space is many layers deep. Not only are tech giants like Microsoft, Dell, and Hewlett-Packard in the fray, but private cloud computing companies such as Artisan Infrastructure and SEN Technologies are providing a substantial supply glut.

This does not mean that every cloud computing business is destined to fail, but it does mean that companies will need to differentiate themselves from the competition. Two public companies that have done so are CommVault and Akamai. Both have kept their product as simple as possible. CommVault's Simpana is a single-platform service, and Akamai works solely with Cisco. Many other cloud computing and big data companies have dozens of partnerships that suck away revenue and increase expenditures.

What to expect moving forward

For long-term investors, Salesforce.com, Fusion-io, and December's hot IPO Nimble Storage should be avoided. All three are experiencing greater expense growth and widening net profit margin losses. EMC has been, and will continue to be, a stable option. Do not expect any surprises from EMC either way.

The two that will most likely outperform are Akamai and CommVault. Both have differentiated themselves and indicated that management has found a way to balance the cloud storage and big data supply glut.

The contrarian play is to pick up a smaller firm like Fusion-io or Nimble Storage with the hope that, during the inevitable consolidation phase, these two will be picked up quickly. The consolidation phase should begin within the next couple of years because the biggest players in the industry know that too many hats are in the ring, driving prices down.