Investors looking for solid income may wonder if there are big bank stocks with growing dividends. And it turns out, there are three with a lot to like, and they should certainly be put on investors' watchlists.

1. Wells Fargo (WFC +0.41%)

Much has been said about Wells Fargo through the years. There's the reality that it has delivered remarkable returns since 1990 -- as colleague John Maxfield noted, Wells Fargo's total return stands at 3,880% versus 880% for the S&P 500 -- and also that Buffett has continually upped his ownership to now stand above $25 billion, or nearly 9% of the company.

But what often goes undiscussed is the reality that the company is committed to increasing its dividend available to shareholders. Over the last year, it has seen its dividend per share rise by a remarkable 26%, according to S&P Capital IQ. And in just two years' time, it has been able to boost its quarterly dividend from $0.22 a share to $0.35, an increase of nearly 60%.

But there's more to like about Wells Fargo than just the growth in its dividend and its historical performance.

While it may trade at a slight premium with its price to tangible book value -- the comparison of its market value relative to the tangible value of a bank if every asset were sold and debt was paid back -- of 2.0 versus the industry average of 1.8, in many ways, this is warranted.

This is because it delivers both a very strong return on assets and equity, and also operates in a very efficient way relative to its peers:

|

Return on Assets |

Return on Equity |

Efficiency Ratio |

P/TBV |

Dividend Yield | |

|---|---|---|---|---|---|

|

Wells Fargo |

1.5% |

13.9% |

57.8% |

2.0 |

2.7% |

|

JPMorgan Chase |

0.9% |

11% |

63% |

1.4 |

2.7% |

|

Bank of America |

0.2% |

1.4% |

91.2% |

1.2 |

1.2% |

|

Citigroup |

0.4% |

4% |

70% |

0.9 |

0.1% |

First six months of 2014. Source: Company Investor Relations.

When you factor all this together, it's easy to understand why Buffett and investors everywhere think so highly of it.

2. JPMorgan Chase (JPM 1.90%)

While Wells Fargo topped the list, it would be a mistake to not mention JPMorgan Chase. It too has impressively upped its dividend, with its payout over the last 12 months standing 20% higher over the previous period.

And while it doesn't exactly match Wells Fargo in the performance metrics, it does have one that distinctly stands out: its current valuation.

With a P/TBV sitting at just 1.4, the market is demanding a significantly lower premium for the bank with Jaimie Dimon at the helm relative to Wells Fargo. While some of that may be justified thanks to the possibility of greater risk posed by it -- the London Whale loss of $6 billion plus the $920 million in settlements stands out -- the sizable discount it trades at is enticing.

Even JPMorgan itself noted at its latest investor day that it too felt its stock was undervalued, and this was in February, when its valuation was nearly identical to where it stands today.

All of this is to say, when you combine a growing dividend, solid performance and an attractive valuation, JPMorgan Chase must also be included on this list.

3. U.S. Bancorp (USB 0.44%)

Last, and certainly not least, we take a step down from the big four into the next "big bank" class and find U.S. Bancorp, which has upped its dividends per share by 15% over the last year.

And if JPMorgan Chase was a step down in relative valuation to Wells Fargo, then U.S. Bancorp is undeniably a step up, trading at 2.8 P/TBV. And it must be mentioned that its current dividend yield stands at 2.3%, which is below the other two.

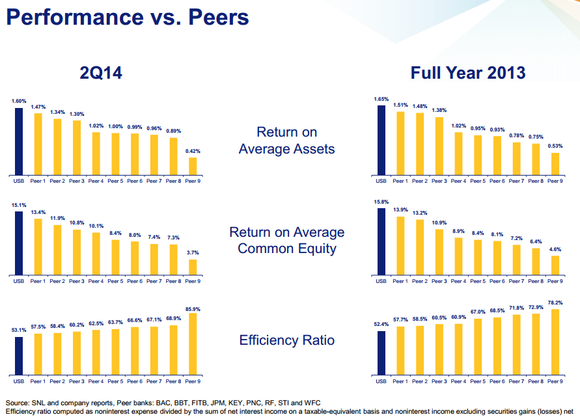

But as the company itself noted in a recent presentation to investors, it is clearly the top performer in the banking industry:

Source: U..S Bancorp CFA Society of Minnesota Conference Presentation.

And it must also be mentioned that while the return delivered by Wells Fargo since 1990 was impressive, it was actually topped by U.S. Bancorp, which stood at 4,140%.

Also consider that while it currently trades at a premium to the other two, since 2010, it has slowly but surely outpaced the other banks mentioned -- to say nothing of the bottom performers -- in its ability to grow the true value available to its shareholders:

While there is clearly a premium placed on U.S. Bancorp, in many ways, it is understandable.

The Foolish bottom line

These three banks are clearly committed to raising their dividends and delivering returns to shareholders, and they are certainly worthy candidates to place on your investment watchlist.