Source: The Southern Company

The Southern Company (SO 0.28%) reported earnings this week, missing on the top line but beating on the bottom. This is the fourth straight quarter The Southern Company has exceeded earnings expectations – but is it time to buy this dividend stock? Here's what you need to know.

The numbers

On the top line, sales for The Southern Company's third quarter came in at $5.34 billion, just shy of its $5.4 billion estimate. Despite the slight miss, that still puts Southern's sales for this quarter above Q3 2013 ($5.0 billion) and Q3 2012 ($5.0 billion).

On the bottom line, Southern continued its earnings streak by pulling in $735 million, or $1.09 per share. That's a $0.02 beat over estimates, mimicking a recurring theme of exceeding earnings expectations. The company surprised by $0.04 to hit $0.50 EPS in Q4 2013, beat by $0.10 at $0.66 for Q1 2014, and squeaked past by $0.02 to $0.68 for Q2 2014. All of these quarters also reflect improvements over year-ago earnings.

From a longer-term perspective, The Southern Company's finances have been volatile, but steadily trending upwards over the past five years.

Beyond the numbers

Financial numbers alone are never enough for a smart investor. With over 37,000 MW of regulated electricity generation, 9,000 MW of competitive power, and 4.4 million customers, The Southern Company is a major energy player with many moving parts.

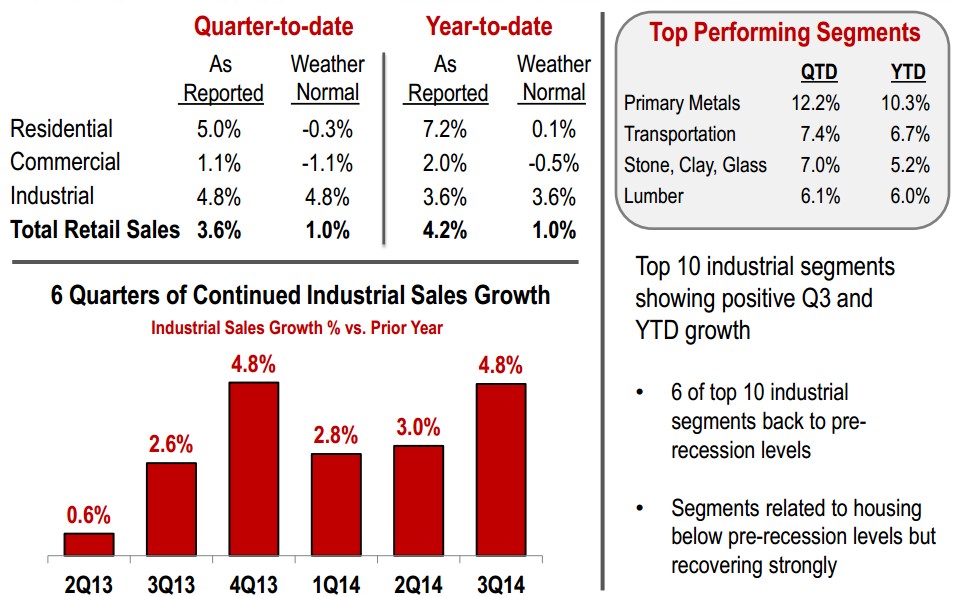

On the regulated front, the utility's guaranteed return on equity means that there's essentially only one simple way to increase profit: increase sales. So far for 2014, weather-normalized sales paint a mixed picture. While Southern's residential customers are essentially unmoved and commercial tapered off, the industrial sector continues to consume more energy.

Source: The Southern Company Q3 2014 Earnings Presentation

On the power generation front, The Southern Company hasn't made any major switches. While other energy utilities like Duke Power Corp (DUK +0.09%) have been moving away from coal, The Southern Company is relying on new technology to keep tapping this cheap, readily available fuel source.

The company's 582 MW Kemper County, Mississippi Integrated Gasification Combined Cycle (IGCC) is meant to turn coal into clean, affordable electricity. But increased costs and delays have turned this dream into a nightmare, and Southern Company stock has long been tarnished by this black mark.

From an initial $2.2 billion cost estimate and a 2013 construction end date, the price tag currently tops $6 billion (with $330 million added on this week) and is far from completion. The plant is currently powering itself off natural gas, and is expected to operate in its full "clean coal" capacity by the first half of 2016.

The Southern Company's second massive infrastructure project is managing to fare better. In response to rising natural gas prices, Southern is hard at work constructing a $14 billion 1,117 MW nuclear power plant in Georgia. If all goes as planned, the units will be in place by Q4 2018.

Time to buy Southern?

Since its earnings announcement, Southern Company stock has slid a couple percentage points as the S&P 500 has made a couple percentage points comeback. That's no reason to buy or sell, but it is indicative of what investors care about.

Despite Southern's solid earnings beat for the fourth consecutive quarter, Mr. Market isn't satisfied with it business operations. It's continually dropped the ball on estimations for its Kemper plant and, more to the point, isn't diversifying as quickly as its competitors.

As fluctuating fuel prices continue to pit coal against gas against nuclear, Southern is stuck with megaprojects that don't offer the dynamism of smaller plants, smart grids, energy efficiency initiatives, or decentralized power. For now, at least, there are simply better dividend stocks to stick your money behind.