Recently, I explained why I consider oil and gas MLP Linn Energy (LINE +0.00%) and its non-MLP equivalent LinnCo (NASDAQ: LNCO) to be high-yield investments ideally suited for retirees. The cornerstone of that opinion is the long-term sustainability of Linn's 13.4% yield. However, as my Motley Fool colleague Matt DiLallo just reported, Linn Energy's most recent earnings report included some disturbing news that could potentially invalidate that thesis.

Great news not as good as it seems

At first glance, Linn Energy seems to have had a great quarter. Production was up 51%, and it reported distributable cash flow (DCF) of $329 million, 8.2% above its earlier guidance. Its distribution coverage ratio, the leading indicator of distribution sustainability and safety, was an impressive 1.37.

However, 91% of that excess DCF figure comes from a onetime benefit of closing its recent deals with ExxonMobil (XOM -1.16%), Devon Energy (DVN -0.30%), and Pioneer Natural Resources (PXD +0.00%). When one excludes these onetime benefits, the actual coverage ratio for the quarter was just 1.03 -- still good, but lower than management was shooting for. In addition, management offered guidance that is concerning regarding the safety and growth prospects of the payout going forward.

How worried should you be about the guidance?

For the fourth quarter, Linn is expecting production to grow by 64% to 71% compared to the same quarter last year. While that's impressive growth, the partnership also announced it expects to fall short of covering its payout by $94 million. About half of this, $45 million worth, is due to pending sales of its Cleveland, Granite Wash, and Wolfberry assets. However, even accounting for this onetime charge, Linn Energy is expecting its coverage ratio to come in at just .83 next quarter.

For the second half of 2014, Linn Energy is now guiding for distribution coverage of .99, which represents a $6 million DCF shortfall. Previously, it had called for a $63 million surplus.

Are falling energy prices threatening the distribution?

In the second quarter conference call, management explained that the bevy of deals and acquisitions Linn Energy was making was designed to secure the long-term sustainability of the distribution by cutting capital expenditures by $550 million to $650 million per year since its Berry Petroleum acquisition. This would provide an excess of $103 million in DCF, and a coverage ratio of 1.1.

Yet, the recent guidance signifies a $69 million swing in expected DCF for the second half of 2014, and pretty much puts an end to any hopes of short-term distribution growth. What accounts for this unexpected cash flow decline?

WTI Crude Oil Spot Price data by YCharts.

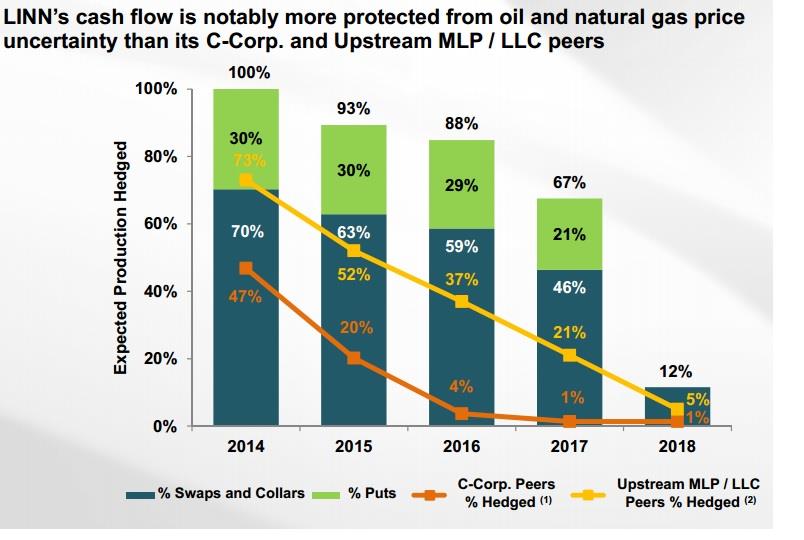

With energy prices plummeting recently, you might think that this explains Linn Energy's disappointing guidance. However, Linn Energy has hedged nearly 100% of its gas production through 2017, and 100% of its oil production for this year at favorable prices.

Source: Linn Energy September 2014 investor presentation.

In fact, as this slide shows, nearly all of Linn Energy's cash flows are secured via hedging through the end of 2016. Therefore, this should ensure that Linn Energy's cash flows are predictable through 2016 no matter what happens to energy prices.

The expected shortfall in DCF is thus not likely a result of a revenue shortfall, but of higher-than-expected capital expenditures. Unfortunately, given Linn's many recent acquisitions, management was unwilling to provide any 2015 capital expenditure or DCF guidance, stating that this would be provided during the next quarter's earnings release after the partnership had time to better study the capital requirements of its new assets.

What to watch going forward

Only 55% of oil production for 2015 and 2016 is hedged -- about 65% in 2015. Therefore, Linn Energy's exposure to dropping oil prices will only increase in the next two years. Given management's recent track record of falling short of DCF guidance, it's very important to keep a careful eye on capital expenditures in 2015 to make sure that DCF at least covers the distribution during the full year.

In terms of potential distribution growth, management has previously stated this would require further accretive acquisitions. Unfortunately, during the conference call, Executive Vice President and Chief Accounting Officer David Rottino said that he expects the volume of acquisitions in 2015 to "look a little slower."

Given that Linn Energy still owns 6,600 net acres of high cost/high decline, yet valuable, Midland basin assets, it will be important to see if management can accomplish its goal of selling/trading these assets by the end of the year -- as is its previously stated goal -- and on what terms. During the conference call, Mr. Rottino indicated that management would be focusing on trading the Midland basin assets for low-decline gas assets, which are not as profitable as oil, but are less volatile, and for which Linn Energy has more aggressive and favorable hedging in place.

Is the distribution safe?

There are three factors that make Linn Energy's distribution unlikely to face a cut during the next year or two. The first is the partnership's aggressive hedging, which should prevent any short-medium term energy price declines from effecting cash flow too severely.

Hopefully, Linn can secure additional oil hedges in 2015. However, at today's price, the company would likely be locking in suboptimal long-term prices. Thus, it would be a trade-off between cash flow security and potentially faster DCF growth should oil prices recover.

Second is the fast production growth. It should help greatly increase DCF if management can keep costs under control.

Finally, as Chief Financial Officer Kolja Rockov pointed out during the conference call, Linn Energy has $2.5 billion remaining on its short-term credit revolver. Although it's far from ideal and not a long-term solution, Linn Energy could cover any shortfall in distribution coverage with debt until oil prices recover enough to permanently secure the distribution.

Bottom line

Although its recent guidance is disappointing and means that investors shouldn't expect its distribution to grow anytime soon, Linn Energy's generous monthly payout is most likely safe for the next year or two. At today's undervalued price, I would still recommend income investors consider Linn Energy for a position as part of their diversified income portfolios.