Ever since arriving in the mid-1990s, Amazon.com (AMZN 0.73%) and eBay (EBAY 0.12%) have disrupted brick-and-mortar retailers across the world. Amazon evolved from an online bookstore to a massive superstore for physical and digital products, while eBay revolutionized online auctions and digital payments by acquiring PayPal.

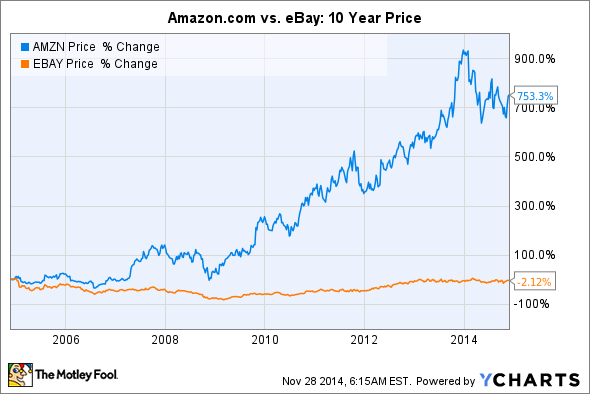

Source: Ycharts.

Both companies are now around 20 years old. Let's take a look at whether Amazon or eBay is the better e-commerce stock to hold for the next 20 years.

Top-line comparison

Amazon's revenue is split into three segments -- media (e-books, video, music), electronics and general merchandise, and "other" (Amazon Web Services, ad services, and co-branded credit cards), which respectively accounted for 26%, 67.5%, and 6.5% of its top line during the first nine months of 2014.

During that period, media sales rose 7.4% year-over-year, sales of electronics and general merchandise climbed 27.1%, and "other" revenue grew 42.8%. This indicates that people are buying more physical products from Amazon, while new initiatives like web services and ads are rising in popularity.

eBay's revenue comes from three segments -- Marketplace (its main site), Payments (PayPal), and Enterprise (Magneto content management, omnichannel operations, and marketing solutions), which respectively accounted for 50%, 44%, and 6% of its revenue during the first nine months of 2014. During that time, Marketplace revenue climbed 8.4% year-over-year, Payments grew by 19.8%, and Enterprise revenue rose 4.6%. However, investors should remember that eBay will spin off PayPal -- its fastest growing business -- in 2015.

Over the past 10 years, Amazon has crushed eBay in terms of pure revenue growth.

Source: Ycharts.

Bottom-line comparison

But when we compare Amazon's and eBay's margins and bottom lines, a different picture emerges. Over the past 12 months, Amazon only had an operating margin of 0.1% versus eBay's 20%. Amazon's and eBay's operating incomes have moved in dramatically opposite directions over the past decade.

Source: Ycharts.

Over the past eight quarters, Amazon posted a net loss four times, while eBay only posted a net loss once, in the first quarter of 2014. Amazon has trouble squeezing out a profit due to higher expenses from fulfilling orders (up 30% YOY in the first nine months of 2014) and higher expenditures on technology and content (up 41% during that period). Together, those two categories accounted for 23% of Amazon's operating expenses.

Yet one could also argue that Amazon uses its free cash flow (FCF) more efficiently than eBay. Amazon had FCF of $1.08 billion versus eBay's $4.57 billion over the past 12 months, although both companies had comparable operating cash flows ($5.71 billion for Amazon and $5.75 billion for eBay).

Amazon has a lower FCF because it reinvests so much of its operating cash flow back into its business. The media loves mentioning failures like the Fire Phone and wild cards like drones, but Amazon spends plenty of cash on practical uses like adding more fulfillment centers and upgrading them with cost-cutting robots. Last year, Amazon added eight new centers in North America and 20 overseas. It's also willing to make cross-industry purchases like Twitch, which it bought earlier this year for $970 million, to validate and complement its fledgling gaming business. Lastly, investing in gadgets like the Kindle and Fire TV tethers more users to its Prime ecosystem.

By comparison, eBay gobbled up smaller auction houses and classified advertising sites over the past decade, but it has no clear plans to straddle and disrupt other industries like Amazon does. eBay's biggest acquisitions were PayPal (2002), Skype (2005), StubHub (2007), Bill Me Later (2008), and GSI Commerce (2010). Since it sold Skype to Microsoft in 2011 and will spin off PayPal soon, eBay's inorganic growth has been fairly conservative. This means that eBay could put its cash to better use on more new products, services, and acquisitions.

Growth potential

Amazon's forward P/E of 375, compared to eBay's forward multiple of 17, indicates that the former is still in growth mode, while the latter is not. According to Alexa, Amazon is respectively the fourth and seventh most visited website in the U.S. and the world. eBay ranks eighth in the U.S. and 21st in the world.

Amazon has two key tools that eBay lacks -- Kindle devices and the $99-a-year Amazon Prime membership program. Amazon sells Kindle tablets and e-readers as well as Fire TV devices at paper-thin margins to generate more revenue from digital media and physical purchases.

The Kindle tablets will play a key role in Amazon's future. Source: Amazon.

With Prime membership, Amazon customers get free two-day shipping, free e-books, unlimited streaming of select media content, and discounts. Prime's user base has risen from at least 20 million confirmed members in January to an estimated 50 million in September. Consumer Intelligence Research Partners reported that the average Kindle owner spent 30% more on Amazon than non-Kindle owners, while Prime members spent twice as much as non-Prime members.

eBay doesn't have anything like the Kindle or Prime to lock in existing members while luring in new ones. That's why eBay's Marketplaces revenue only rose 6% YOY to $2.2 billion last quarter, while Amazon's total revenue soared 20% to $20.6 billion.

The verdict

It's obvious that Amazon is the superior e-commerce stock. Although its valuation is high and margins are nearly flat, it has a clear plan to grow its core business by expanding the Prime empire with consumer devices and digital content. By comparison, eBay will spin off its high-growth PayPal business soon, leaving its investors with the stagnant Marketplaces and Enterprise businesses.