Telecom giant AT&T's (T +1.20%) shareholders didn't enjoy 2014 very much. The stock missed a broad market rally, falling 4% instead.

AT&T owners hope for a smoother ride in 2015. Unfortunately, there are no guarantees of drastic improvements. Here are the three biggest reasons AT&T shares might underperform the market yet again this year.

This silver cloud has a dark lining, too. Image constructed from sources: AT&T and DirecTV.

The DirecTV buyout could fail

There's a huge buyout on the table, waiting for final approvals by American regulators. If the $48.5 billion merger with satellite TV broadcaster DirecTV (DTV +0.00%) passes regulatory muster, it's a clean ticket into new TV markets in North and South America, plus a healthy adrenaline shot for AT&T's free cash flows. Good things are bound to happen for AT&T, if this deal gets the final OK.

However, there are no guarantees that the approvals will come. And AT&T knows it.

In most big acquisitions, you'll find terms explaining what happens if the deal fails to close for various reasons. Four years ago, AT&T had to take that bitter pill when regulators and the Department of Justice combined to kill the company's proposed buyout of smaller rival T-Mobile USA (TMUS -1.60%). That cost $6 billion in cash and valuable radio spectrum licenses, and AT&T doesn't want another bill like that one.

In the DirecTV deal, DirecTV has agreed to pay $1.4 billion to its jilted suitor in case the company finds a better buyout offer from another company. But that's it. Any other deal cancellations, including those forced by the FCC or the DoJ, wouldn't trigger any breakup fees at all.

Taking clear steps to avoid another breakup-fee hangover is hardly a sign of ultimate confidence in the deal's approval. It's like a high-stakes gambler taking out an insurance policy before the big game, just to make sure the losses won't be too large.

I'll say that this merger stands a greater chance of passing regulatory reviews than the proposed combination of cable giants Comcast (CMCSA +2.27%) and Time Warner Cable (NYSE: TWC) does. The cable deal would combine the two largest players in that market, raising red flags about monopoly powers. Add DirecTV and AT&T, and you'd basically combine two different industries. AT&T's U-Verse TV service has just 6.1 million subscribers. Next to DirecTV's 37 million users, that's a drop in the ocean.

Still, it's the type of megamerger that the FCC has been throwing a jaundiced eye at lately. This deal could fail simply as collateral damage from the far wobblier Comcast/Time Warner affair.

And if that happens, AT&T is back to square one. Buying revenue growth is so much easier than building it organically in a mature telecom industry. And even though 2014 wasn't much of a banner year for AT&T's shares, the positive impact of a DirecTV merger has been baked into the stock's prices today.

I give this merger only about a 20% chance of failure. But it's a real risk, and the market backlash would be horrific.

Pricey valuation

Despite weak stock returns in 2014, AT&T actually looks expensive from some important angles.

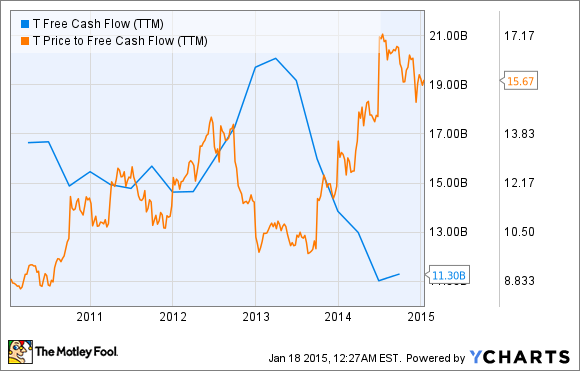

Chiefly, I'm thinking about AT&T's cash-based valuation. Cash is king, and Ma Bell isn't making as much of it as she used to. As free cash flows plunged in 2014, AT&T's price-to-cash flow valuation shot up to levels not seen since 2007. At 15.7 times trailing free cash flows versus archrival Verizon's (VZ +2.19%) price-to-free cash flows ratio of just 11.1, AT&T also compares poorly with its most important industry peer.

That's where the stock is hovering now, raising eyebrows and hackles on cash-focused value investors everywhere:

T Free Cash Flow (TTM) data by YCharts

T-Mobile CEO John Legere loves to throw spanners in the mobile industry's works. Source: T-Mobile.

Strong competition

T-Mobile and Sprint (S +0.00%) have caused constant headaches for both AT&T and Verizon lately. Sprint has the financial backing and industry expertise of Japanese telecom maverick Masayoshi Son and SoftBank on its side. Armed with a bold new CEO and a plethora of innovative marketing strategies, Sprint is poised to regain lost market share in 2015.

And T-Mobile is riding its "Uncarrier" strategy to strong market gains. If nothing else, the company is putting enough pressure on the mobile business model to force AT&T's hand into following suit in some cases. Meanwhile, the magenta telecom is growing faster than either AT&T or Verizon nowadays. The Uncarrier ideas are working.

This pressure will continue unabated in 2015. Strong competition is great for consumers, who reap the benefits of having carriers fighting for their attention and dollars. It's not so good for undisputed market leaders like Verizon and AT&T, who would much rather rest on their highly profitable laurels than adapt to a rapidly changing market.

Each one of these three risk factors may not amount to much, but put them all together and you'll see why I'd rather not own AT&T stock right now.