Image source: BHP Billiton.

Image source: BHP Billiton.

When BHP Billiton (BHP +2.86%) released its fiscal first-half earnings, CEO Andrew Mackenzie commented on the commodity downturn: "it's the speed and the quantum and the synchronized nature of those declines that have been more than we, or frankly anyone else in the industry, could have expected." That was the setup for some bad news, but also the backdrop for important improvements. Here are five things BHP Billiton's management wants you to know.

1. The dividend is different now

One of the big questions going into the semiannual update was the dividend. Would it survive as is, or would the downturn lead to a dividend cut, as it had at giant competitors Rio Tinto (RIO +1.46%) and Vale (VALE -0.07%)? Few were surprised by the answer. According to the CEO, "To match the economic conditions that we face today and expect to face in the future, the board has now adopted a dividend pay out policy equivalent to a minimum of 50% of underlying attributable profit." In other words, BHP is cutting the dividend.

That, however, is much better than the news at Vale, which eliminated its dividend earlier this year because of the commodity downturn. Rio Tinto, meanwhile, is still planning a dividend, but, like BHP, it's going to be lower than it has been. Although this might be a difficult pill for dividend-focused investors to swallow, all three companies are simply doing what's necessary to ensure they are positioned for the world that exists today.

2. Samarco is on our minds

Another big topic of interest for investors is the Samarco disaster, in which mine waste broke through a storage area and flooded several towns, taking human lives along the way. Samarco is a 50/50 joint venture with Vale. At the time of the call, Mackenzie said, that "discussions are also ongoing with the Brazilian government as well as the state government of Minas Gerais and Espirito Santo" about how to manage and fund the cleanup effort.

BHP and Vale have since come to an agreement with Brazil on cleanup costs, and how much each has to pay. The numbers are pretty big -- $1.1 billion each. But that's really just the starting point, because the miners still may face civil and criminal cases arising from the disaster. The takeaway here is that BHP has taken major steps in the right direction, but you'll want to keep listening for Samarco updates for a while.

3. We're doing OK

With the ugly stuff out of the way, CFO Peter Beaven highlighted some positives from the first six months of the year, including these:

- "We generated net operating cash flows of $5.3 billion, and free cash flow in every one of our businesses."

- "Our 40% EBITDA margin is significantly higher than our closest peer at only 29%."

- "We maintained our strong balance sheet holding net debt broadly stable over the last 12 months, despite substantially weaker prices and significant dividend payments."

That's a lot of information at once, but the point is that BHP is surviving the downturn fairly well -- in fact, better than many of its peers. So despite the bad news, BHP is still one of the cleanest shirts in the mining industry.

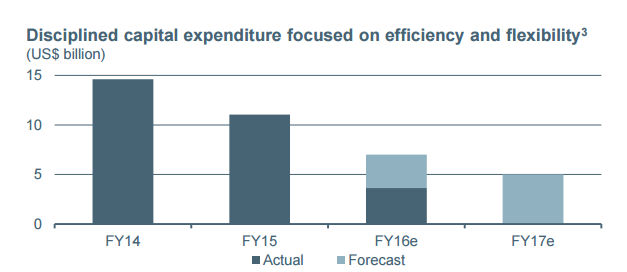

Capital spending heads down. Image source: BHP Billiton.

4. We're spending wisely

The dividend cut, however, is really part of a bigger issue, and that's how BHP plans on using cash. It wants to put cash to work where it will do the most good and, at the same time, preserve its financial strength. And on that score, the CFO noted that the miner plans "to invest $7 billion in the 2016 financial year and $5 billion in 2017."

That level of capital spending is down from nearly $15 billion in 2014, so BHP is tightening the belt pretty hard. But Beaven assured investors that "all projects that deserve to get capital are included in our funding plan." Put a different way, BHP is cutting back, but it isn't (and can't) stop spending. It's just making sure the money it spends is spent wisely.

So what kind of spending is going to take place at BHP? According to the CEO, "Capital efficient projects that leverage existing infrastructure and release latent capacity continue to present attractive near-term opportunities, even at current prices," and those are the first priority. Basically, these are projects that allow BHP to do more with less.

5. Here's a wild card to watch

That brings up another issue related to spending. When pushed on the topic of investing in current operations or buying assets, the CEO said, "This is an environment where, in many respects, buy, rather than build, is more attractive." Backing this claim up is the company's investment-grade debt rating and strong cash flow. In fact, unlike some miners that are simply looking to survive, BHP appears to have the capacity to do some deals.

Spending on internal projects simply increases the supply/demand imbalance that's hurting commodity prices. So even though BHP may be avoiding big internal projects, don't think it isn't looking to increase production in other ways. And if the commodity markets remain moribund, there could be some compelling opportunities that BHP is uniquely positioned to act upon.

Half full/half empty?

It would hard to say that BHP's earnings and conference call were filled with good news. BHP is suffering through a very difficult period. But if you look past the bad, there is a lot to like about this giant and globally diversified miner. And BHP really is surviving the downturn better than many of its peers, despite what the high-profile Samarco disaster might suggest. BHP, then, remains a good option for more conservative investors looking to step into the mining space. That's doubly true if you think consolidation is in the cards, since BHP, with a strong balance sheet, is likely to be on the buying side there.