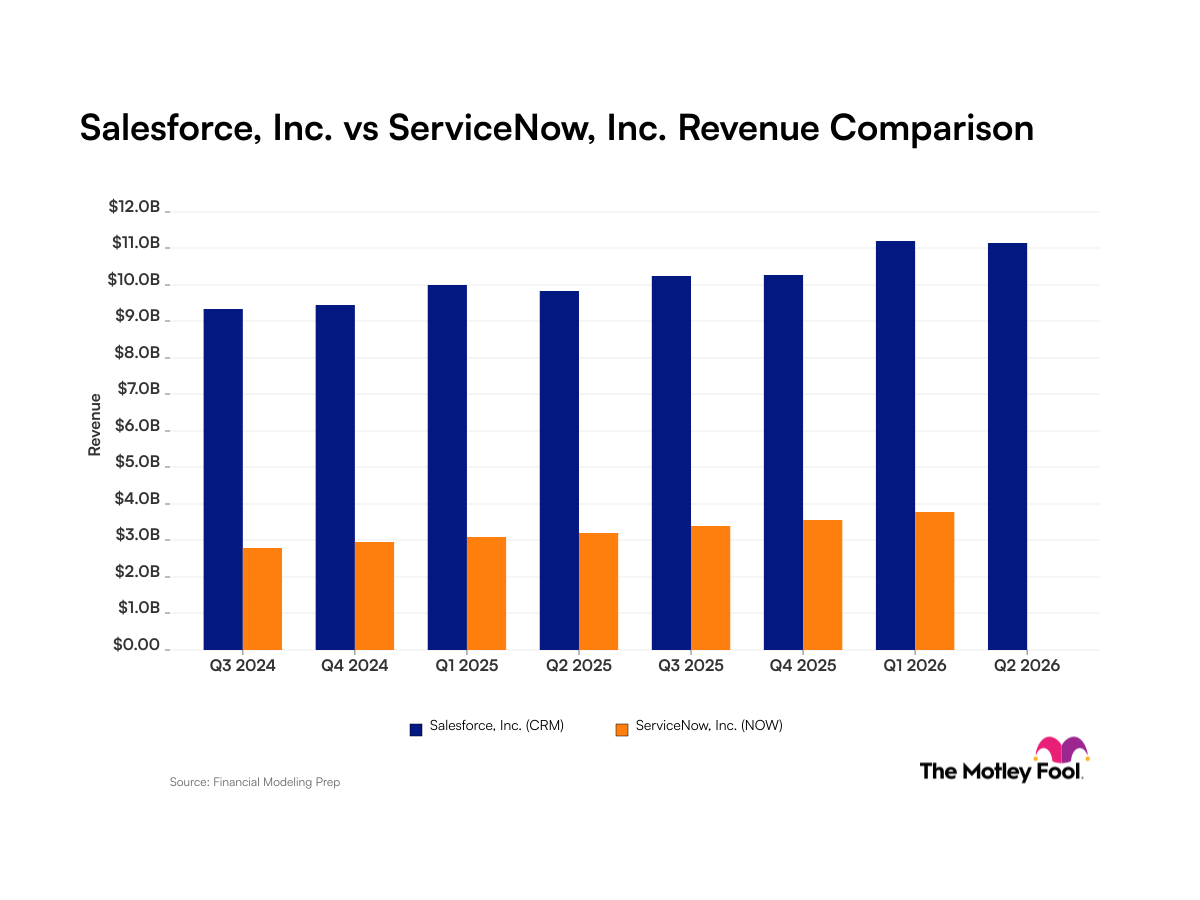

The news is out: salesforce.com (NYSE: CRM) reported earnings yesterday, and the stock has fallen by 5% already -- even though …

- There was 22% revenue growth in the fourth quarter.

- Customer acquisition is up by 31%.

- Per-share profits rose by 41% for the quarter and 82% for the year.

- Free cash flow climbed by 29% to $217 million.

Superb news. But if you're surprised at the market's reaction … well, you shouldn't be. Previewing what we wound up seeing yesterday, I gave investors the following advice last week:

I'm still not convinced that this valuation is cheap enough to justify buying [salesforce.com]. Analysts on average believe salesforce.com will grow at a nearly 36% clip over the next five years, which … seems priced into the stock at today's multiple. …

My advice: Keep your powder dry. Wait for a market correction or an investor overreaction to salesforce.com's earnings (due out next week, by the way.) Call it a hunch, but I suspect that if you are patient, you'll get a chance to own this superb stock at a significantly better price."

Hold your applause

Now, if you're worrying that this will be an "I told you so," column -- don't. I was right last week, yes. But honestly, salesforce.com's overvaluation was so obvious that it wasn't all that tough of a call. Our dilemma today is a bit more difficult: Now that salesforce.com has dropped in price, we need to ask whether it's dropped enough to justify your buying in.

I'd argue it has not -- and that you should not.

My thinking here basically mimics what I told you about Brocade (Nasdaq: BRCD) yesterday. You see, right now, post-selloff, salesforce.com sells for 38 times its 2009 free cash flow. If salesforce.com could achieve the long-term growth rate that Wall Street was expecting pre-earnings, that price might be appropriate. After all, 36% is faster than SAP (NYSE: SAP) , Microsoft (Nasdaq: MSFT), or Oracle (Nasdaq: ORCL) is expected to grow. Why, it's even faster than Google (Nasdaq: GOOG)!

Unfortunately, salesforce.com disappointed the Street yesterday, predicting sub-consensus 16% to 17% growth in 2010. That's a slowdown from yesteryear, and it's going to force Wall Street to walk back its growth assumptions going forward.

Foolish takeaway

How long of a walk Wall Street takes remains to be seen. But the farther they walk, the more overvalued salesforce.com will look. My advice: You've waited this long to own salesforce.com. Wait a little longer. We'll reach an attractive price eventually.

Is there such a thing as a growth stock selling for an attractive price? There is. They're here.