Long-term investing is a better approach than stock trading for many reasons, including:

Higher probability of positive returns

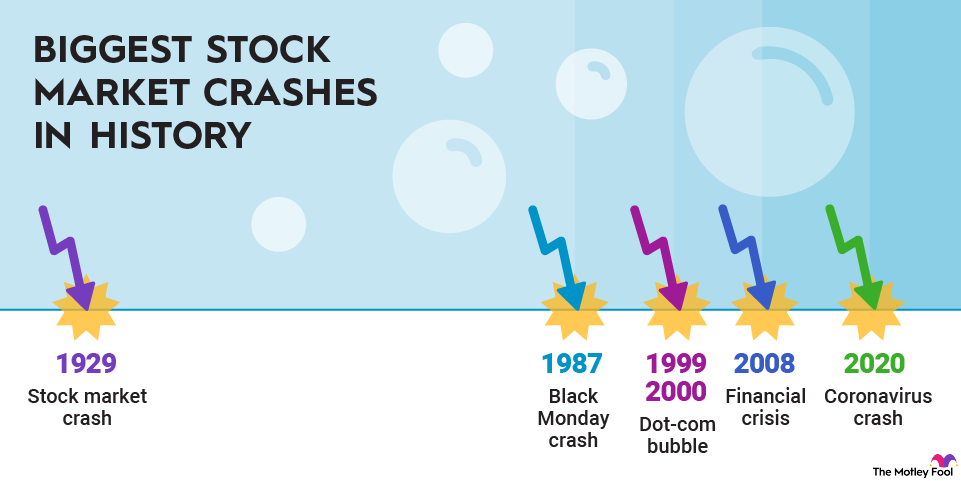

While the stock market has had down years, it has gone up in 70 of the past 96 years, or about 73% of the time. So, even if you start investing right at the end of a long bull market run and endure a stomach-churning crash, simply holding for a few years will likely still yield a positive result.

Contrast that with trading, which could see an investor risk the permanent loss of their capital if they buy at the top and then give up and sell at the bottom, locking in losses.

Not missing out on even bigger gains

One of the biggest mistakes many beginning investors make is selling too early, which can cause them to miss out on much greater returns over the long term. For example, while it might be tempting to cash in after a 10% or even 100% gain, great companies tend to continue producing winning returns.

Benefiting from compound interest

While stocks can correct and crash without warning, they generally move higher. As noted earlier, the S&P 500 has historically delivered a total annualized return of more than 10%. Despite all the volatility, that general upward trend adds up over time. For example, investing $550 a month in an S&P 500 index fund has historically grown into a $1 million nest egg in about 30 years.

Saving on taxes

Stock sales are taxable unless they're made in a tax-deferred retirement account, such as an individual retirement account (IRA). For stocks held long-term (more than a year), the capital gains tax rate is either 0%, 10%, or 20%, depending on your income and tax bracket.

However, short-term capital gains are taxed at a higher rate because they are treated as ordinary income, which is taxed at a rate of 10% to 37%. Taxes can eat a significant portion of an investor's gains if they're trading in and out of stocks, especially those in higher tax brackets.

While buying and holding over the long term generally yields the best returns, it's also essential to know when to sell stocks. Situations where selling is a smart move include when the reason you bought the stock no longer applies, the company is being acquired, you are rebalancing your portfolio, you need cash for a big purchase, or you see a better investment opportunity.