HSA distributions and taxes

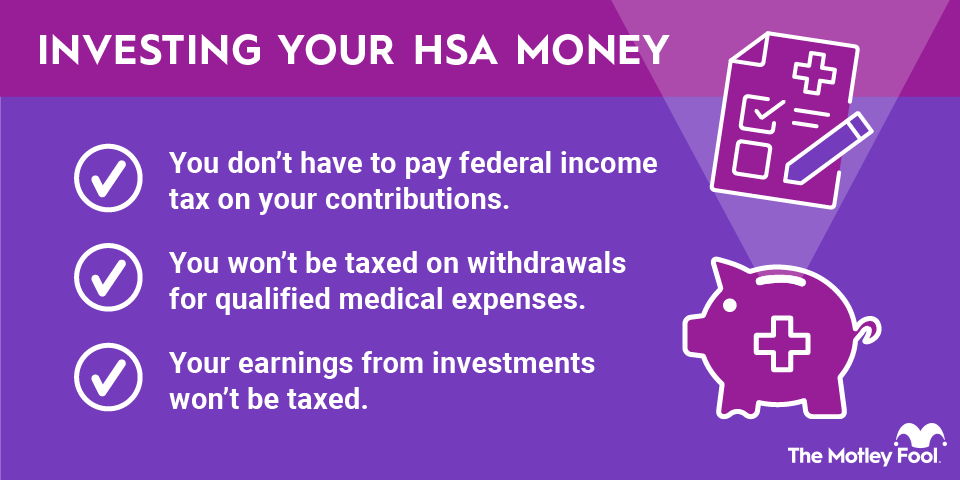

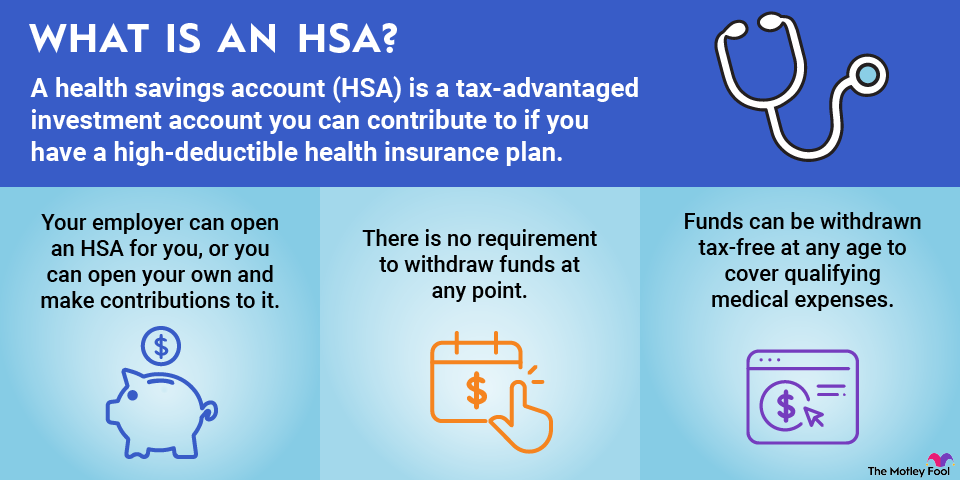

HSAs are a valuable type of investment account because you can make contributions with pre-tax funds, allow your money to grow tax-free, and make tax-free withdrawals for medical expenses. Most other tax-advantaged accounts, such as IRAs and 401(k)s, allow either pre-tax contributions or tax-free withdrawals -- but not both, as the HSA does.

Although a qualified HSA distribution is not taxable, you still must file IRS Form 8889 to report any distributions made during the year.

However, if you have made nonqualified distributions because you took money out of your HSA that you did not use to pay for eligible medical services, you will be taxed on the distribution at your ordinary income tax rate. If you have not yet reached age 65, you will also be subject to a 20% penalty on the withdrawn funds.

Those who are 65 or older may make nonqualified distributions without incurring the extra penalty and pay only ordinary income tax. In other words, HSA distributions made after age 65 are treated like those made from a 401(k) or traditional IRA. Because of this added flexibility, HSAs are often used as a retirement savings account.