Analyzing Bank of the Ozarks (OZRK 1.18%) is a bit like peering through the looking glass in Alice in Wonderland.

If you read the comments from its executives, you'd think it was the most conservative bank in the industry. But if you step back and take an objective look at the facts, Bank of the Ozarks comes across as one of the riskiest banks in the country right now.

Banks are incredibly fragile institutions. Even the mere rumor about large loan losses can cause a bank to come tumbling down. Image source: Getty Images.

Tripling down on risky loans

Over the past five years, as Bank of the Ozarks' growth rate dramatically accelerated, it has flagrantly flouted numerous time-tested axioms of banking.

It has loaded up on commercial real estate (CRE) loans, which are among the riskiest loans banks make. And it has focused on the riskiest corner of the CRE market to boot: construction and development loans. If that isn't enough, moreover, it has focused on the riskiest type of construction and development loans: those that finance out-of-market commercial real estate projects.

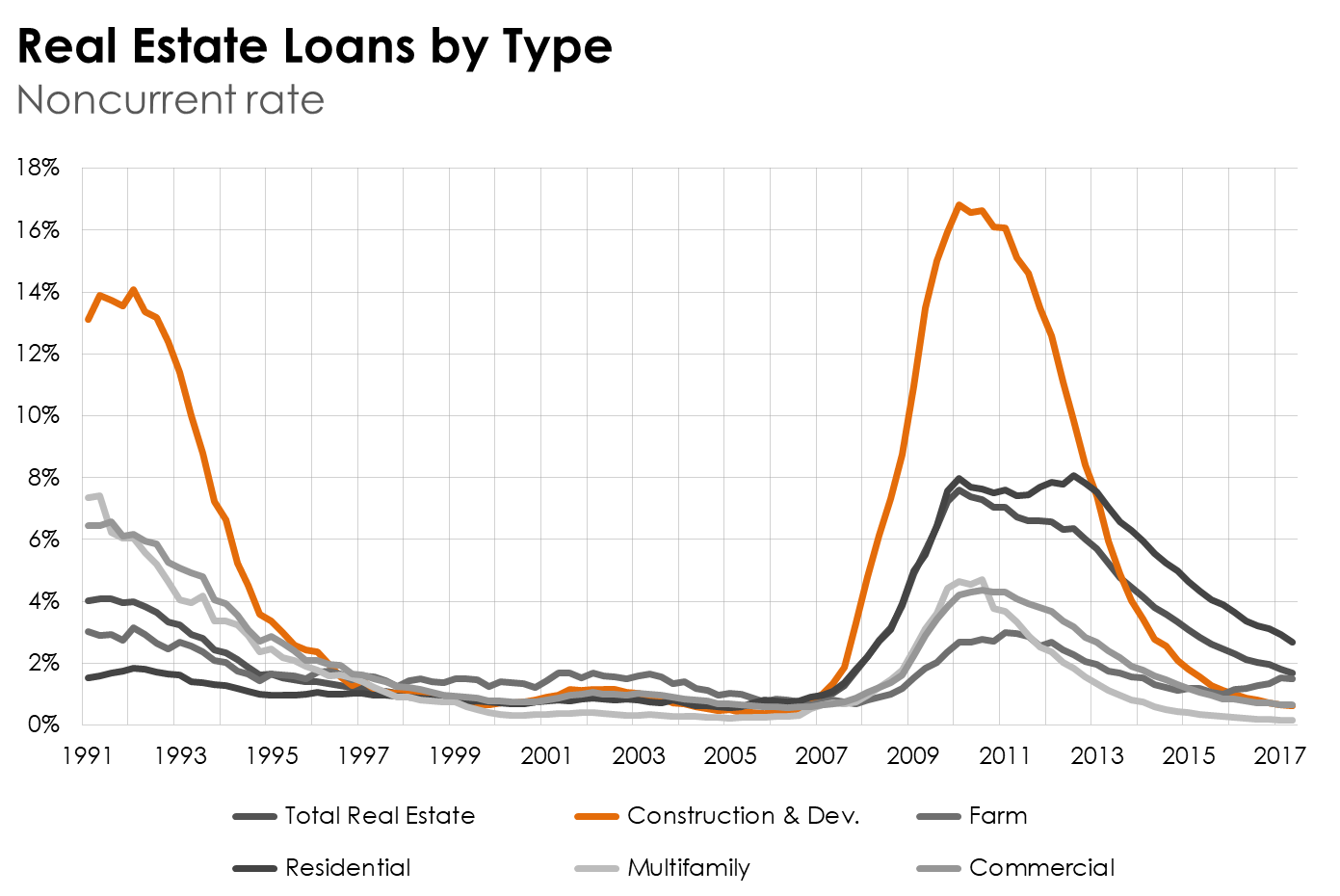

These types of loans default at a higher rate than other types of loans. See that orange line in the chart below that towers over the other lines in the recessions of the early 1990s and following the financial crisis of 2008? That represents the delinquency rate on construction and development loans.

Data source: FDIC. Chart by author.

The problem isn't just that construction and development loans default at a higher rate, which is also reflected in the annual stress tests administered by the Federal Reserve. When you couple it with out-of-market lending, the losses given default are also meaningfully higher.

A 2014 study found that loss given default rates on CRE loans were consistently higher for out-of-market loans. For construction and development loans, loss given default was between 3.7% and 7.7% higher than for in-market loans, depending on how a bank's territory is defined. The obvious conclusion, according to the study's authors: "Knowledge of local markets might be especially important for the servicing of C&D loans."

As an aside, this could explain why the Securities and Exchange Commission (SEC) wrote Bank of the Ozarks a letter last year asking, among other things, how it monitors real estate projects "throughout their lives to make sure the properties are moving along as planned to ensure appropriateness of continuing to capitalize interest." Relatedly, it also could explain why Bank of the Ozarks took the incredibly unusual step of suspending its duty to submit financial filings to the SEC.

A flawed defense

Bank of the Ozarks' executives offer a handful of explanations for the bank's bewildering growth strategy. However, they seem to perceive its strongest defense to be that its portfolio of out-of-market construction and development loans, which were originated by its real estate specialties group, or RESG, are ostensibly well-backed by collateral. Here's the bank's chief administrative officer Tim Hicks on the bank's latest conference call:

At quarter end, our average loan to cost for the RESG portfolio was a conservative 48.9% and our average loan to a price value was even lower at just 41.5%. The very low leverage of this portfolio exemplifies our conservative credit culture and is one of many reasons we have such confidence in the quality of our loan and lease portfolio.

If you read between the lines, Bank of the Ozarks' argument is basically that it doesn't matter if the loans from its RESG unit, which account for the majority of its on- and off-balance sheet CRE exposure, default at a high rate because they're purportedly so well collateralized.

But there are two fundamental flaws in this logic. First, if a recession were to strike, especially one that bears down on CRE values, there's no telling how far CRE prices will fall, especially for the projects Bank of the Ozarks finances. This may explain why other banks won't make these loans. Keep in mind that there isn't a huge market for half-developed commercial real estate projects in the middle of an economic downturn.

Even more importantly, a reliance on loan-to-value ratios like this misses the point about what causes banks to fail. It isn't insolvency. Most often, if not in the vast majority of cases, the problem is liquidity. As institutional investors and depositors catch wind of high default or delinquency rates at a bank, they withdraw their money en masse, causing a funding crisis. Look at major bank failures in the past, from Continental Illinois to Washington Mutual, and liquidity is the culprit.

In short, not only has Bank of the Ozarks thrown caution to the wind by doubling and tripling down over the last five years on the riskiest types of loans banks make, but it also seems to be justifying its inexplicable strategy with a defense that's fundamentally flawed.