Shares of Textainer Group Holdings Limited (TGH +0.00%), which leases out shipping containers, had an incredible run in 2017, advancing over 188% in the year. Meanwhile, oil tanker owner Nordic American Tankers Ltd. (NAT +0.47%) stock was down roughly 70%. So far this year, however, both have been flip-flopping, with Nordic American down around 6% and Textainer off by just over 20%. But despite the dramatic shift, here's why Textainer remains a better long-term option.

Solid at the core

Textainer's core business entails the use of debt to buy the standardized shipping containers used to transport goods around the globe. It then leases those containers to customers for multiyear periods. When a lease is up, it either tries to sign another lease or sells the container. Just about every part of that process has been doing well lately.

Image source: Getty Images.

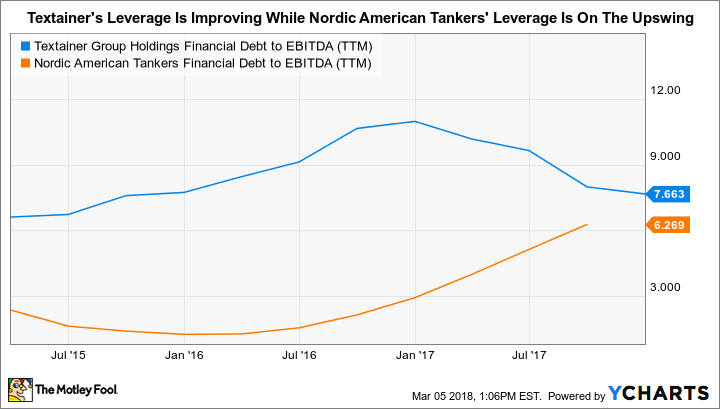

For example, the company's utilization rate has climbed from around 94% during the recent industry downturn to nearly 97.5%, helping to materially increase earnings as lease rates start to move higher due to a shortage of supply. The price of new containers, in the meantime, has jumped by around 80%, pushing out marginal players that were eroding industry pricing and making life hard at industry giants like Textainer (which has the second-largest container fleet in the world). At the back end, the price of used containers has doubled since hitting bottom in 2016, roughly the nadir of the downturn. Also, Textainer is one of the least leveraged companies in the container leasing business, giving it plenty of leeway to keep growing its container fleet.

Although shipping can be a volatile industry, Textainer's containers are largely leased out on multiyear contracts lasting five to seven years. So new contracts are being signed at higher rates as older ones roll off, essentially locking in stronger results in the years ahead. The company describes this as a lease expiration tailwind. Excited investors may have gotten ahead of themselves in 2017, pushing the shares up dramatically, but the changes taking shape at Textainer are at a fundamental level and should continue to support solid results at the business. The early 2018 pullback, then, isn't a sign of a reversal of fortunes.

The struggle continues

Nordic American Tankers, on the other hand, is still suffering under the weight of a heavy debt load. That was a key cause of investor fear in 2017, a period when the company was working to recapitalize its business, including issuing stock to help pay down debt. Complicating the issue were weak dayrates in the ship leasing industry. To give you an idea of just how weak the ship leasing market is, Nordic American reports that the average dayrate over the past quarter-century was around $30,000, but ended the year at just $13,800 (and hit a low of $10,600 in the third quarter).

To be fair, its financial position appears to be improving. Long-term debt fell roughly 12%, or about $54 million, between 2016 and 2017, largely thanks to the aforementioned share issuance, which took place late in the year and raised around $100 million. However, the company will be taking on another $130 million or so of debt in the second half of 2018 as three new ships are delivered. So the debt reduction in 2017 may be more of a bandaid than a resolution of the issue. In fact, the stock issuance was just one part of management's larger debt restructuring efforts, as it works to improve the strength of its balance sheet. It openly admits there's more to be done. .

It appears that the lingering issue for Nordic American are the relatively weak dayrates, which makes the leveraged financing approach used in the leasing sector problematic. If dayrates don't improve, debt payments will remain a big headwind. To put some numbers on that, interest expense ate up nearly 40% of the company's EBITDA in 2017. Although it had a similar number of roughly 30%, Textainer had positive earnings for the year while Nordic American was in the red.

TGH financial debt to EBITDA (TTM). Data by YCharts.

It's also worth highlighting a big difference between the two companies: Textainer's business is about frequent purchases of a large number of relatively cheap shipping containers with short useful lives. Nordic American Tankers buys a small number of very expensive ships that are used for a long time. It's simply easier for Textainer to adjust its business to prevailing market conditions. When industry trends go against Nordic American, it can be very hard to adapt.

Too much risk

After a huge stock price advance in 2017, Textainer's stock appears to be taking a breather as investors digest 2017 performance numbers and the prospects for 2018. However, Textainer appears to be in solid financial condition, in addition to operating in an industry that's already begun to turn around. Nordic American, on the other hand, continues to face a number of big question marks, not least of which are a still comparatively weak ship leasing market, high leverage, and a restructuring effort that's not yet complete. Most investors would be better off sticking with Textainer at this point or simply staying on the sidelines.