If you're looking for dividend stocks to buy right now, Annaly Capital Management, Inc. (NLY 0.82%) and Newell Brands Inc. (NWL -4.79%) may be on your list. Annaly's fat 11.5% yield is incredibly attractive on its surface, while Newell Brands' above-average 3.5% payout and recent track record of dividend growth are appealing, too.

But at the same time, Annaly's dividend track record hasn't exactly been stellar, and a major interest rate trend is decidedly not in its favor going forward. Newell Brands also has its share of problems, including a looming boardroom fight for control of the company's future. The reality is, both companies have serious fundamental challenges that make for a lot of uncertainty. And if you're looking for a dependable dividend stock, uncertainty is your enemy.

Instead of hoping your timing is right, take a closer look at Retail Opportunity Investments Corp. (ROIC). This high-performing retail property owner pays a strong 4.4% dividend yield, has a solid track record of raising the payout, and is led by a top-notch management team with a long track record of success.

Image source: Getty Images.

The fight for Newell's future creates risk

Newell Brands may not ring many bells, but there's a good chance you own more than one -- potentially a lot more -- of its many products, including Rubbermaid, Graco, Oster, Papermate, Coleman, and dozens more. But since its late-2015 deal to buy fellow consumer-brands conglomerate Jarden for $13.2 billion, the company has faced a number of struggles to turn all that new revenue into outsize profit growth. Without a little history lesson, a look at a chart of the company's results might make you think it's an absolute bargain today.

Less than five times earnings? A huge jump in profits last year? Alas, all is not as it seems. A noncash benefit related to the new federal tax legislation signed into law in late 2017 gave the company a one-time bump. Newell's profits and revenue actually fell in the fourth quarter if we factor out this little wrinkle.

These recent struggles have led management to start the process of selling off what it considers noncore brands and assets in order to focus on the segments responsible for the majority of sales and EBITDA. This is probably the right move and should prove good for investors. Unfortunately, some big-name activist investors are facing off over the company's strategy. On one side you have Carl iCahn, who owns almost 7% of the company and recently reached an agreement to appoint four iCahn employees and allies to its board. On the other side is activist investor Starboard Value and its 3.8% stake and plans to nominate its own slate of directors.

Add it all up, and staying on the sidelines seems prudent. Newell needs to make changes and streamline its business, but with two big-time activist investors lining up to fight it out, investors would probably be best served to wait for the dust to settle. If it weren't for this risk, I think Newell Brands would be a potential value/turnaround play. But a looming proxy fight and uncertainty around who will end up holding the reins -- and setting the strategy -- create risk for dividend investors.

Correlation may not be causation, but...

Annaly Capital Management's big fat 11.5% yield is hard to ignore. But at the same time, investors need to understand how Annaly makes money and how that sets it up for a lot of pressure on its ability to grow earnings -- or even just sustain its dividend -- going forward. As a real estate investment trust -- or REIT -- Annaly is required to pay out the vast majority of its earnings to shareholders. But as a mortgage REIT, Annaly's assets are almost entirely made up of debt, not properties.

In short, the company owns real estate debt, using a substantial amount of debt to fund its investments, with its income essentially the difference between the interest it must pay on the debt it takes out and the interest it collects on the loans it owns. Historically speaking, that has translated to falling dividend payments after interest rates go up and rising dividends after rates decline.

NLY dividend data by YCharts.

Here's the bad news: We are in a rising-rate environment, and I think it would be a mistake to use "this time it's different" as an investing thesis for Annaly. History has been a solid indicator -- increasing rates make it harder for Annaly to sustain its dividend.

There are some potential positives for Annaly, particularly a relatively healthy housing market and what looks like the early stages of millennials starting to buy homes. That's great for homebuilders, but it's not enough to offset the risks that rising rates pose for Annaly Capital.

Great management and a solid strategy make this a dividend winner

While Retail Opportunity Investments Corp. is also a REIT, there is a substantial difference between its business of owning and leasing properties, and Annaly's business of owning the loans. This makes a difference in the impact of rising interest rates on its business, since its assets -- properties -- are long-lived in nature, and generally appreciate in value, and it often has access to debt at long-term fixed rates. This alone means a much higher level of predictability for the sustainability of dividend as compared to Annaly.

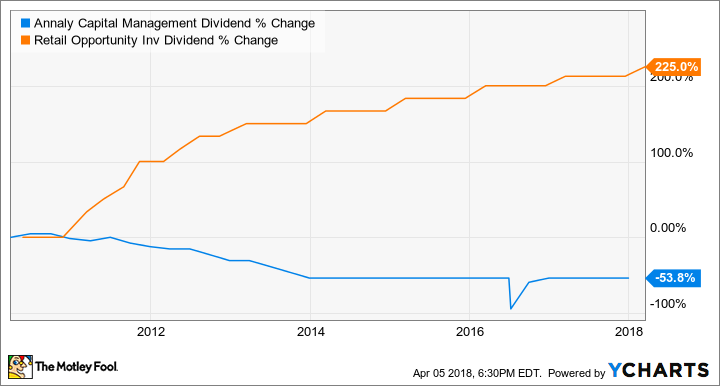

Here's how that has played out since ROIC went public in 2010.

NLY Dividend data by YCharts

ROIC's dividend has more than tripled over the period, while Annaly's has been cut in half. The company's management deserves a lot of credit, as they have identified a valuable niche in commercial real estate: high-value strip malls on the West Coast with an anchor grocery or pharmacy tenant to drive traffic and create value for other tenants.

Furthermore, ROIC isn't subject to Newell Brands' corporate shenanigans and the uncertainty of a proxy battle for its control.

A deeper look could pay off big

Just looking at yields and valuations on a chart could easily lead you down the path of buying shares of Newell or Annaly. And to be honest, there's a chance that such an investment could pay off. But a little closer look at the companies makes it clear that there are very real concerns that investors should -- at the very least -- consider before spending a dime on them.

ROIC, on the other hand, has a strong record of execution on its strategy under a very capable management team and a path forward that should be far less fraught with the difficulties Annaly and Newell Brands are facing. Based on that, it's not a difficult conclusion that investors would be better off buying ROIC and staying away from the other two, at least for the foreseeable future.