Investing doesn't have to be complicated. Long-term investing has been shown to outperform short-term investing and investing in simple business models has been a key theme for some of the world's best investors, including Warren Buffett and Peter Lynch. If investing in easy-to-understand businesses for the long haul appeals to you, then it could be a good time to consider Dunkin' Brands (DNKN +0.00%), WD-40 Company (WDFC -1.80%), and Apple (AAPL +1.02%).

A coffee drinker's delight

Todd Campbell (Dunkin' Brands): Like coffee? Me, too. And that's why Dunkin' Brands' simple business model makes it such a good investment idea.

IMAGE SOURCE: GETTY IMAGES.

You see, the company's leveraging its ability to deliver your daily caffeine fix for sales growth by offering increasingly more food items, including a new sausage sandwich using Beyond Meat. It's also expanding its footprint by opening more stores and testing delivery in major markets, including New York City.

In Q1, new products helped increase sales by 2.4% at existing stores and that, plus new stores, resulted in total sales rising 5.9% year over year to $319 million. Its adjusted operating margin was 33.3%, up from 31.8% last year, and its adjusted earnings per share improved 8.1% from one year ago to $0.67 in the quarter.

There's reason to think these strong results can continue. Dunkin's comparable-store sales increase was its best in four years and its earnings performance stemmed from increasing royalty income from its franchise owners and lower personnel costs -- two things that should continue offering tailwinds. Management expects its general and administrative expenses to drop at a mid-single-digit rate even as revenue climbs this year.

With more stores opening, new product offerings, and a tight lid on expenses, I think this is an easy-to-understand investment option that's poised to benefit long term from consumers seemingly unending love affair with coffee.

Sell one product and do it incredibly well

Tyler Crowe (WD-40 Company): If you are going to be a one-trick pony, then you better be able to do that trick better than anyone else. That statement is perhaps the most succinct way to describe The WD-40 Company because it does one thing and one thing only, and that is to sell WD-40. If you are looking for an easy-to-understand business that has done a great job of creating value for investors, then WD-40 is a stock to consider.

OK, so saying that all The WD-40 Company does is sell that iconic blue spray can overlooks some of the company's other cleaning and lubricant products. Based on the company's financials, though, WD-40 and the various ways the company sells it make up the vast majority of sales. In the most recent quarter, WD-40 multi-use and WD-40 specialty lubricants comprise more than 90% of sales.

It's easy to understand WD-40 as a business -- and to see how it creates value for its shareholders. It sells a ubiquitous branded product at a high margin. In fact, it doesn't even manufacture the products it sells. All WD-40 products are made by third-party manufacturers. That means WD-40 Company is very capital-light -- meaning it doesn't require lots of capital investments to keep the business going. All that cash the company generates can then be used to reward investors with ever-increasing dividends and share repurchases. This simple formula has translated into an incredible wealth generator for its investors.

WDFC total return price. Data by YCharts.

Sometimes the greatest investment ideas are the simplest ones. You can't get much simpler than WD-40, and it has worked out rather well so far for those who own the stock.

IMAGE SOURCE: GETTY IMAGES.

Size and simplicity

Travis Hoium (Apple): It may be one of the biggest companies in the world, but Apple is still one of the simplest businesses around. The company makes three core products: Macs, iPhones, and iPads and the operating system and software that supports those devices. Peripheral devices like the Apple Watch, Apple TV, AirPods, and the App Store are important to the product ecosystem, but they aren't fundamentally what drive the company.

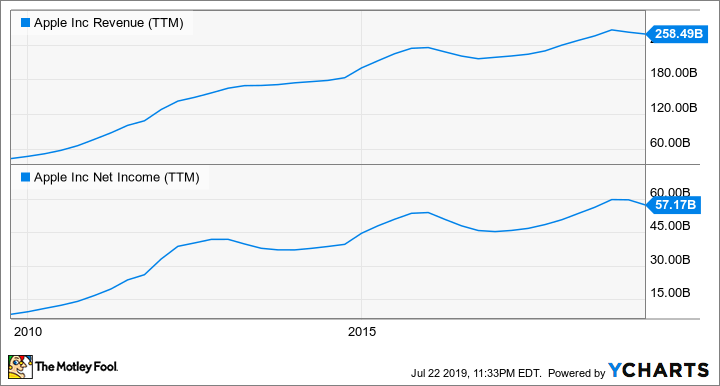

As a result, analyzing Apple is relatively straightforward for investors. If device sales are going up, it's good. And if they're going down, it's bad. Right now, you can see that revenue is going up, but that's despite iPhone unit sales peaking in 2015 at 231.2 million and bumping between 211.9 million and 217.7 million over the last three years.

AAPL revenue (TTM). Data by YCharts.

The biggest reason revenue is up is the increase in iPhone prices. An iPhone XS Max will set customers back a whopping $1,099, which is the same as an entry-level Mac computer. There's only so much more Apple can push on iPhone prices and not give up unit sales.

Questions around Apple's growth potential given very few products and a limited ability to raise prices are why the stock trades at 17.4 times trailing earnings, far below many large tech rivals. But given the simplicity of the business model, this is a stock that anyone starting out in investing can understand, both for its strengths and weaknesses.