Surprisingly, 2021 has been a more challenging year on Walt Disney (DIS +1.73%) stock than 2020. I say surprisingly because this has been a year of economic reopening, where all its theme parks have reopened, blockbuster films are back on the big screen, and its hotels and resorts are welcoming guests. This is following 2020 when, because of the pandemic, many of those operations temporarily shut down.

The latest challenge came this week when Barclays analyst Kannan Venkateshwar downgraded Disney's stock to equal weight from overweight; and assigned it a price target of $175 down from $210.

Image source: Getty images.

Disney+ is facing headwinds

The main argument behind the stock price cut is the slowing growth at Disney+. Venkateshwar has a point. Disney's stock rallied in 2020 even while many of its operations were closed because of the success of Disney+. Hundreds of millions of people were cooped up indoors before vaccines became widely available, which led to a surge in demand for in-home entertainment. Launched in November of 2019, Disney+ benefited and has reached 116 million subscribers as of July 3.

With economies reopening and folks spending less time at home, the demand for streaming services is leveling off, leading to stagnating growth at Disney+. Disney CEO Bob Chapek even warned investors at a conference in late September that Disney+ is facing headwinds in the near term that will likely cause it to report its slowest subscriber growth since its launch.

Venkateshwar is concerned that the slower growth could lead Disney to lower its long-term outlook for Disney+ subscribers. As it stands, management expects the company to reach between 230 million and 260 million Disney+ subs by 2024. If the company indeed lowers that target, the stock is likely to fall in response.

A buying opportunity?

Investors should look at any such drawback in Disney's stock price as a buying opportunity. The stock is trading at a forward price-to-earnings ratio of 34, which is the lowest it has sold for dating back to January 2020. Its theme park segment returned to profitability last quarter, and Chapek said that results would be even better this quarter.

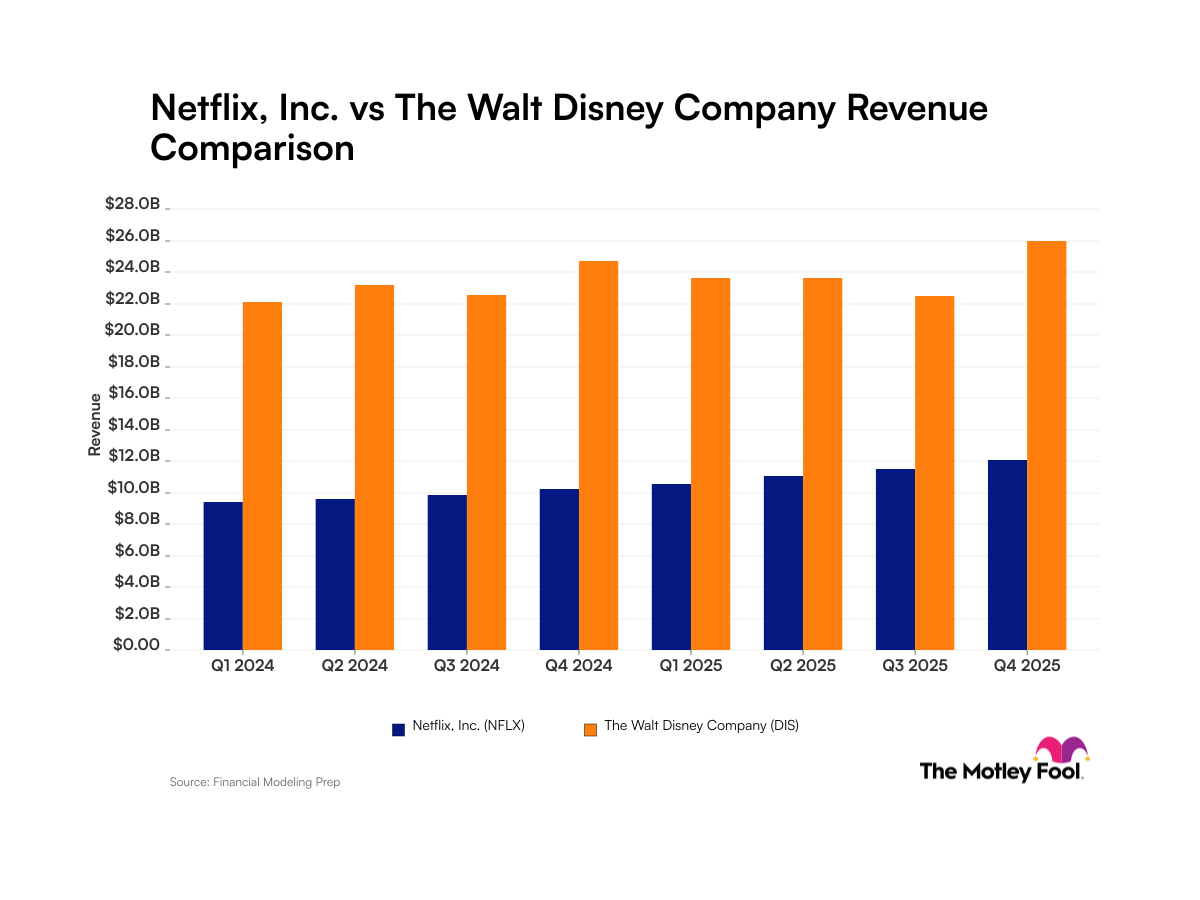

And despite the headwinds, its streaming services segment has generated $11.7 billion in revenue in the nine months ended July 3. To put that figure into context, Netflix's revenue in all of fiscal 2020 was $25 billion, and the streaming pioneer has been in the business for over a decade, whereas Disney is just getting started.

In the long run, Disney is likely to have several hundred million streaming subscribers worldwide, and the road to that target will be choppy and could take longer than expected. Long-term investors should be ready to buy Disney stock on a dip if the drop results from short-term fluctuations in streaming subscriber growth.