When investors think of surging artificial intelligence (AI) stocks, Palantir Technologies and Nvidia are probably the first two that come to mind. Palantir is a leader in AI software and its stock is up by a whopping 530% over the last 12 months. Nvidia supplies the world's best AI data center chips and its stock has climbed by 74% over the same period.

But more and more companies are using AI to supercharge their legacy businesses. Duolingo (DUOL +4.80%), for instance, operates the world's largest digital language education platform, and it offers a growing portfolio of AI features designed to accelerate the learning experience. Its stock has more than doubled over the past year on the back of the company's stellar operating results, which have been boosted by AI.

Is there still time to buy Duolingo stock? Read on to find out.

Image source: Getty Images.

AI is creating new opportunities for Duolingo

Duolingo owes its success to its mobile-first, gamified approach to education. It takes learning out of the classroom and places it at the fingertips of anyone with a smartphone, enabling them to move at their own pace.

Duolingo had more than 128 million monthly active users during the second quarter of 2025 (ended June 30), which was a 24% increase from the year-ago period. The platform monetizes them in two ways: It shows ads to free users, and it sells subscriptions to those who want to unlock more features to accelerate their progress. A record 10.9 million users were subscribed in Q2, which was up 37% year over year.

Duolingo Max is the platform's most expensive subscription tier, and it offers a growing list of AI features as a selling point. There is Explain My Answer, which provides users with personalized feedback after each lesson, and Roleplay, which uses a chatbot-style interface to help users practice their conversational skills in a language of their choice. Duolingo also launched a new tool for Max subscribers last year called Video Call, which features a digital avatar named Lily who helps users practice their speaking skills.

Max subscribers represented a record 8% of the platform's total paying members during Q2, up from 7% in the first quarter just three months earlier. Its AI features are a step toward Duolingo's long-term goal to deliver a learning experience that rivals a human tutor, so expect penetration to continue to grow.

NASDAQ: DUOL

Key Data Points

Duolingo's revenue growth is accelerating

Duolingo generated a record $252.3 million in revenue during Q2, which crushed even the high end of management's forecast of $241.5 million. The figure represented a 41% increase compared to the year-ago period, which marked an acceleration from the 38% growth the company delivered during the first quarter. Simply put, the business is carrying a ton of momentum right now.

On the back of the strong Q2 result, management increased its full-year revenue forecast for 2025 to more than $1 billion. This would be the first year in the company's history that revenue crosses the billion-dollar milestone.

Duolingo also delivered a blistering second quarter at the bottom line. The business generated $44.8 million in net income, which was up by an eye-popping 84% from the year-ago period. Not many tech companies can deliver accelerating revenue growth without burning truckloads of cash at the bottom line, so Duolingo's consistent (and growing) profitability is an incredibly impressive achievement, and it's a key reason for its soaring stock price.

Duolingo stock presents an opportunity for long-term investors

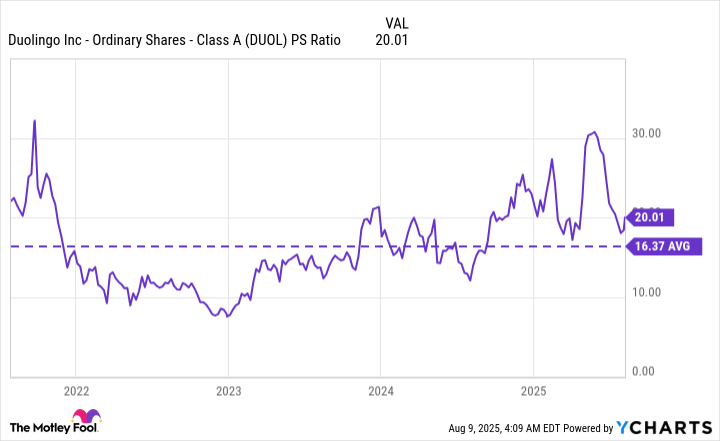

Duolingo's business is certainly firing on all cylinders right now, but investors will have to pay a premium if they want to own a slice. Its stock is trading at a price-to-sales (P/S) ratio of 20, which is a 22% premium to its long-term average of 16.4, dating back to when it went public in 2021:

DUOL PS Ratio data by YCharts

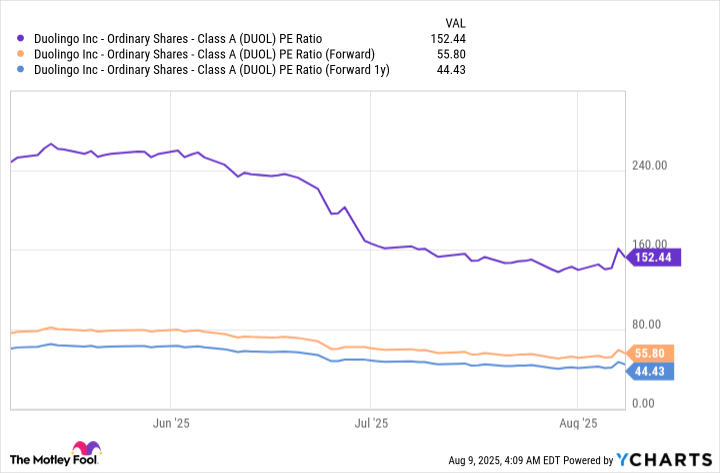

Since Duolingo is consistently profitable, investors can also value its stock using the price-to-earnings (P/E) ratio -- but it looks even more pricey by that metric. Based on the company's $2.40 in trailing-12-month earnings per share (EPS), its P/E ratio is currently an eye-popping 152.3. That makes the stock five times more expensive than the Nasdaq-100 technology index which trades at a P/E ratio of 32.9.

The stock looks a little more attractive if it is valued based on its future potential EPS. Wall Street's consensus estimate (provided by Yahoo! Finance) suggests Duolingo could generate $6.64 in EPS during 2025, placing its stock at a forward P/E ratio of 55.7. Analysts then expect $8.34 in EPS during 2026, which translates to a forward P/E ratio of 44.4:

DUOL PE Ratio data by YCharts

The stock still isn't cheap on a forward basis, but investors who are willing to hold on to it for five years or more could still do well if they buy it at the current price, purely because the company's earnings are growing so quickly.

Short-term investors who are looking for quick gains over the next 12 months or so should probably steer clear of Duolingo stock, but it could be an attractive buy for those with a longer-term outlook.