Investing in strong companies and holding them for a long time is a time-tested strategy for making money in the stock market. Following this philosophy can make the most of secular and disruptive growth opportunities that could shape the world, and shareholders could see their investments grow at a healthy pace thanks to compounding.

One such stock to consider buying right away and holding for the next decade is ASML Holding (ASML 3.16%). The Dutch semiconductor equipment giant is one of the best ways to capitalize on the secular growth of the chip industry. Let's look at the reasons this semiconductor stock can make investors richer in the next 10 years.

Image source: ASML

ASML is on track to deliver a decade of outstanding growth

The global semiconductor industry's revenue in 2024 stood at $627 billion, according to Deloitte and is expected to hit almost $700 billion this year. By 2035, the industry's revenue could more than triple to $2.4 trillion.

NASDAQ: ASML

Key Data Points

This remarkable growth is going to be driven by huge amounts of spending on artificial intelligence (AI) data centers equipped with powerful accelerators capable of tackling extensive workloads. AI chips alone are expected to account for a third of global semiconductor sales by 2035, growing at an annual pace of nearly 35% through the next decade.

Chipmakers and foundries will have to turn to ASML's machines to satisfy the booming chip demand over the next decade. Its lithography machines, along with its software and services, are crucial for printing various kinds of chips, especially the advanced kind that power AI data centers, smartphones, and computers.

The company is known for being the only manufacturer of extreme ultraviolet lithography (EUV) machines, and it reportedly has a 90% share of the deep ultraviolet lithography (DUV) market. Its EUV machines allow its customers to manufacture advanced chips, and that's precisely the reason the company witnessed a bump in its order book in the third quarter of 2025.

ASML received 5.4 billion euros ($6.3 billion) worth of orders in third quarter, slightly higher than analysts' expectations. The figure was more than double the bookings ASML saw in the same period last year. Management said in a news release that it sees "continued positive momentum around investments in AI."

That seems a bit conservative because recent developments in the AI space clearly indicate that a huge infrastructure spending boom is in the cards. OpenAI, for instance, struck deals with various chipmakers and cloud infrastructure providers for getting access to 26 gigawatts of AI data center capacity in the next decade. OpenAI, which shot into the limelight three years ago with ChatGPT, committed to spending more than $1 trillion over the next decade to build up this capacity.

Such massive spending by the likes of OpenAI and others will filter down to ASML, considering the latter's position in the advanced chipmaking market. Industry association Semi estimates that advanced chipmaking capacity of chips sized below 7-nanometer -- which are capable of handling larger workloads -- could expand at an annual rate of 14% through 2028.

So ASML could receive more orders for its equipment over the next 10 years as major cloud hyperscalers and AI companies such as OpenAI pour huge amounts of money into infrastructure development. That could eventually lead to an acceleration in growth.

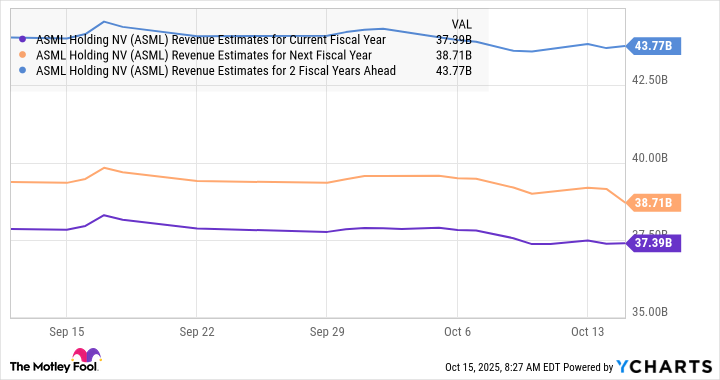

ASML is expecting 15% growth in its revenue for 2025 and improved its outlook for 2026, when it is now expected to record growth. Consensus estimates are projecting ASML's growth to step on the gas from 2027.

ASML Revenue Estimates for Current Fiscal Year; data by YCharts.

What's more, ASML can sustain its momentum beyond 2027 as the EUV lithography market, where it holds a monopoly-like position, could generate almost $175 billion in annual revenue in 2035. That would be a big increase over last year's EUV equipment spending of $19 billion.

Here's how much upside this stock could deliver in the next decade

ASML doesn't just sell EUV machines. Its product portfolio also includes DUV machines, refurbished equipment, metrology and inspection systems, and customer support. But even if we assume that ASML gets all of its revenue from EUV machines a decade from now, it could deliver tremendous upside.

We have seen that the EUV lithography market could hit $175 billion in revenue in 2035. Assuming that a challenger emerges in this market and reduces ASML's share to even 80%, its top line could hit $140 billion based on its EUV business alone. Multiplying that by ASML's price-to-sales ratio of 11 points toward a market cap of just over $1.5 trillion in 10 years. That would be a potential jump of 285% from current levels.

So ASML definitely looks like a top growth stock to buy and hold for the next decade considering the potential upside it could deliver.